Question: The table below shows the closing prices (represented by letters) on a particular day for a series of European call options with different strike prices

The table below shows the closing prices (represented by letters) on a particular day for a series of European call options with different strike prices and expiry dates on a particular risky non-dividend-paying security.

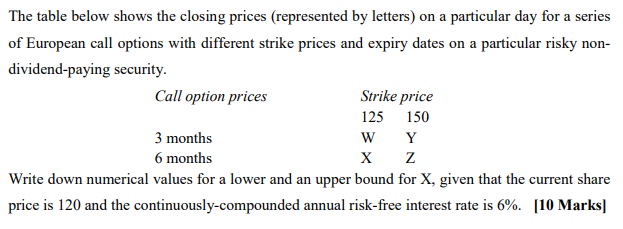

The table below shows the closing prices (represented by letters) on a particular day for a series of European call options with different strike prices and expiry dates on a particular risky non- dividend-paying security. Call option prices Strike price 125 150 3 months w Y 6 months X z Write down numerical values for a lower and an upper bound for X, given that the current share price is 120 and the continuously-compounded annual risk-free interest rate is 6%. [10 Marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts