Question: The table below shows the projected cash flow statements for Apex Corporation, which is being considered as a target for Hightech, a large conglomerate. The

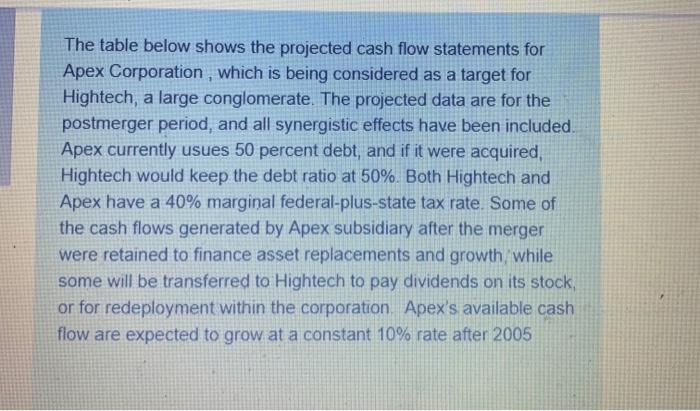

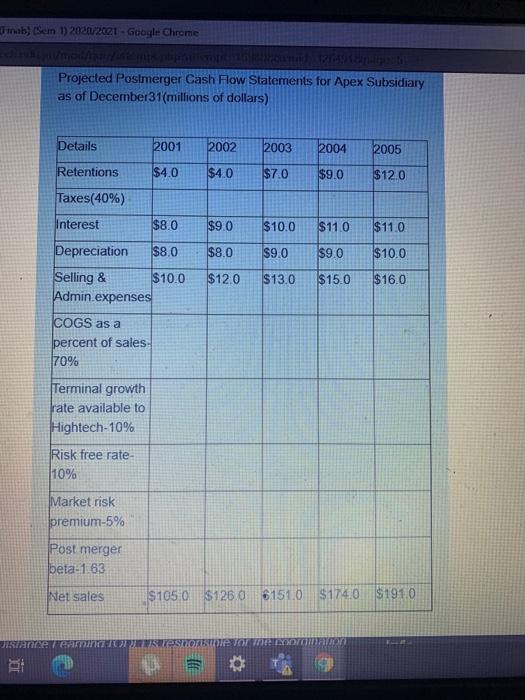

The table below shows the projected cash flow statements for Apex Corporation, which is being considered as a target for Hightech, a large conglomerate. The projected data are for the postmerger period, and all synergistic effects have been included Apex currently usues 50 percent debt, and if it were acquired, Hightech would keep the debt ratio at 50%. Both Hightech and Apex have a 40% marginal federal-plus-state tax rate. Some of the cash flows generated by Apex subsidiary after the merger were retained to finance asset replacements and growth, while some will be transferred to Hightech to pay dividends on its stock, or for redeployment within the corporation Apex's available cash flow are expected to grow at a constant 10% rate after 2005 Pinab) (Sem 1) 2020/202.1- Google Chrome Projected Postmerger Cash Flow Statements for Apex Subsidiary as of December 31(millions of dollars) Details 2001 2002 2003 2004 2005 Retentions $4.0 $4.0 $7.0 $9.0 $120 Taxes(40%) Interest $8.0 $9.0 $10.0 $11.0 $11.0 $8.0 $9.0 $90 $10.0 Depreciation $8.0 Selling & $10.0 Admin.expenses $12.0 $13.0 $15.0 $16.0 COGS as a percent of sales 70% Terminal growth rate available to Hightech-10% Risk free rate- 10% Market risk premium-5% Post merger beta-1.63 Net sales $1050 $1260 61510 $174.0 $191,0 DISTA TIETOITOTUOMET The table below shows the projected cash flow statements for Apex Corporation, which is being considered as a target for Hightech, a large conglomerate. The projected data are for the postmerger period, and all synergistic effects have been included Apex currently usues 50 percent debt, and if it were acquired, Hightech would keep the debt ratio at 50%. Both Hightech and Apex have a 40% marginal federal-plus-state tax rate. Some of the cash flows generated by Apex subsidiary after the merger were retained to finance asset replacements and growth, while some will be transferred to Hightech to pay dividends on its stock, or for redeployment within the corporation Apex's available cash flow are expected to grow at a constant 10% rate after 2005 Pinab) (Sem 1) 2020/202.1- Google Chrome Projected Postmerger Cash Flow Statements for Apex Subsidiary as of December 31(millions of dollars) Details 2001 2002 2003 2004 2005 Retentions $4.0 $4.0 $7.0 $9.0 $120 Taxes(40%) Interest $8.0 $9.0 $10.0 $11.0 $11.0 $8.0 $9.0 $90 $10.0 Depreciation $8.0 Selling & $10.0 Admin.expenses $12.0 $13.0 $15.0 $16.0 COGS as a percent of sales 70% Terminal growth rate available to Hightech-10% Risk free rate- 10% Market risk premium-5% Post merger beta-1.63 Net sales $1050 $1260 61510 $174.0 $191,0 DISTA TIETOITOTUOMET

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts