The Toliza Museum of Art In early 2009, Juan Antonio Jimenez has just begun his new...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

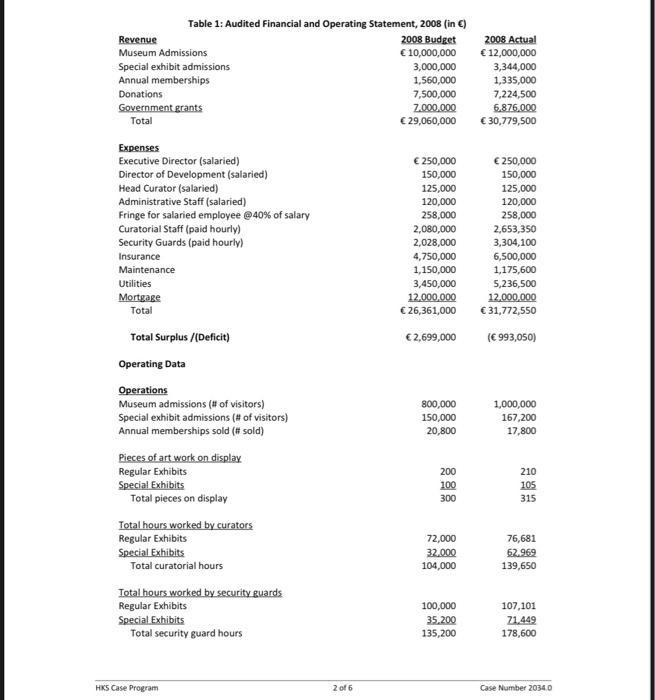

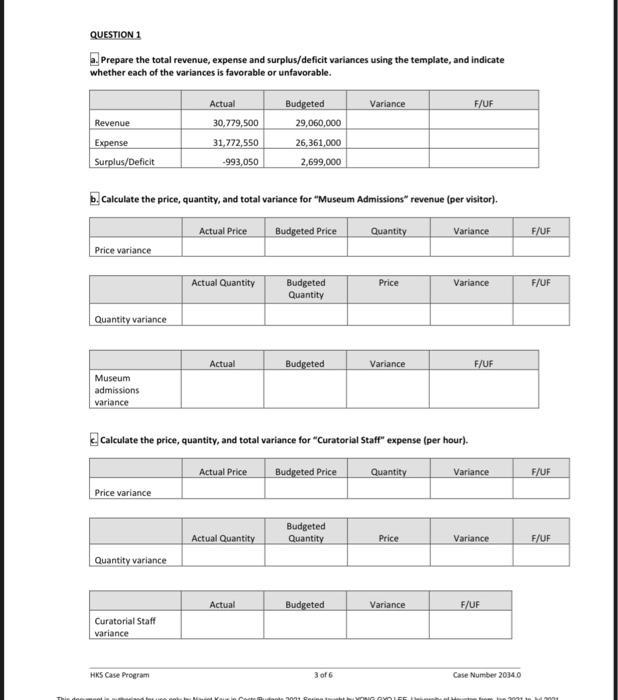

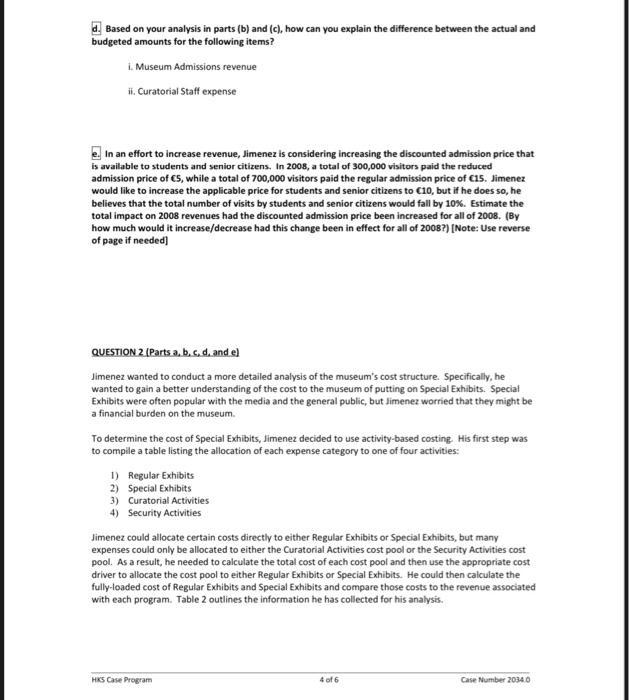

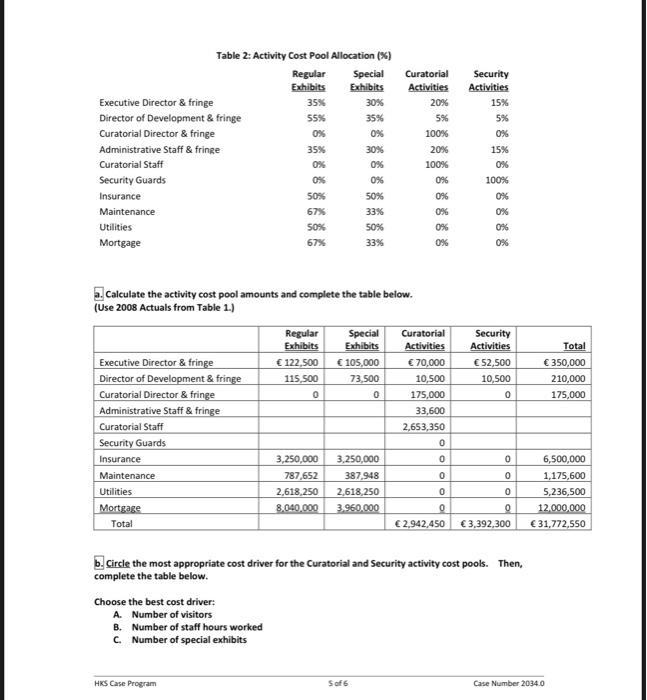

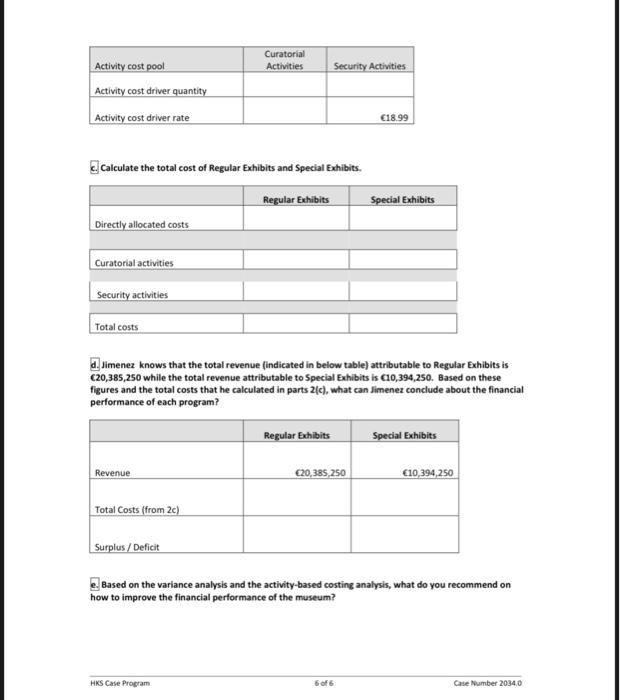

The Toliza Museum of Art In early 2009, Juan Antonio Jimenez has just begun his new position as Executive Director of the Toliza Museum of Art ("Toliza"). Toliza is a beautiful art museum located in the city of Toliza, Spain. Toliza's art collection includes a wide variety of classic and contemporary art, all housed in a forty-room museum and sculpture garden in the heart of the city. Toliza displays its art to the public in two ways: Regular Exhibits and Special Exhibits. Regular Exhibits are displayed throughout the year and feature pieces from the museum's permanent collection, which focuses on art from the Toliza area. Special Exhibits are limited-time only displays (often four to six weeks in duration) featuring pieces by renowned artists that are on loan from other museums. When Jimenez was hired as Executive Director, the Board of Directors made it clear to him that his first priority should be to analyze the museum's finances. The Board was concerned about the museum's financial performance in 2008, when Toliza operated at a deficit despite putting on three well-received Special Exhibits. Toliza's revenues came from: admissions fees, exhibits, annual memberships, donations and government grants. The expenses are primarily labor costs. In addition to Jimenez, Toliza's senior management team includes one Director of Development and one Head Curator. Other employees include four administrative staff members, seventy professional curating staff and numerous security and maintenance staff who are paid on an hourly basis. There are currently eighty-nine individuals who work part-time on security. As Jimenez strolled through one of the museum's special exhibition halls-currently featuring the early works of Pablo Picasso-he began to wonder what had caused the museum's deficit in 2008 and what financial results could be expected in 2009. Upon reaching his office, he set about to answer these questions, beginning with a review of the financial and operating data presented in Table 1. Table 1: Audited Financial and Operating Statement, 2008 (in €) 2008 Budget € 10,000,000 2008 Actual € 12,000,000 3,344,000 1,335,000 7,224,500 6.876.000 Revenue Museum Admissions Special exhibit admissions Annual memberships 3,000,000 1,560,000 Donations 7,500,000 Government grants Total Z.00.000 € 29,060,000 € 30,779,500 Expenses € 250,000 € 250,000 Executive Director (salaried) Director of Development (salaried) Head Curator (salaried) 150,000 150,000 125,000 125,000 Administrative Staff (salaried) Fringe for salaried employee @40% of salary 120,000 120,000 258,000 258,000 Curatorial Staff (paid hourly) 2,080,000 2,028,000 2,653,350 3,304,100 6,500,000 1,175,600 Security Guards (paid hourly) Insurance 4,750,000 Maintenance 1,150,000 Utilities 3,450,000 5,236,500 Mortgage Total 12.000,000 12,000,000 € 26,361,000 € 31,772,550 Total Surplus /(Deficit) €2,699,000 (€ 993,050) Operating Data Operations Museum admissions (# of visitors) 800,000 150,000 1,000,000 Special exhibit admissions (# of visitors) Annual memberships sold (# sold) 167,200 20,800 17,800 Pieces of art work on display Regular Exhibits Special Exhibits 200 210 100 105 Total pieces on display 300 315 Total hours worked by curators Regular Exhibits Special Exhibits 72,000 76,681 62.969 32.000 104,000 Total curatorial hours 139,650 Total hours worked by security guards Regular Exhibits 100,000 107,101 Special Exhibits Total security guard hours 35.200 135,200 21.449 178,600 HKS Case Program 2 of 6 Case Number 2034.0 QUESTION 1 a Prepare the total revenue, expense and surplus/deficit variances using the template, and indicate whether each of the variances is favorable or unfavorable. Actual Budgeted Variance F/UF Revenue 30,779,500 29,060,000 Expense 31,772,550 26,361,000 Surplus/Deficit -993,050 2,699,000 b. Calculate the price, quantity, and total variance for "Museum Admissions" revenue (per visitor). Actual Price Budgeted Price Quantity Variance F/UF Price variance Actual Quantity F/UF Budgeted Quantity Price Variance Quantity variance Actual Budgeted Variance F/UF Museum admissions variance Calculate the price, quantity, and total variance for "Curatorial Staff" expense (per hour). Actual Price Budgeted Price Quantity Variance F/UF Price variance Budgeted Quantity Actual Quantity Price Variance F/UF Quantity variance Actual Budgeted Variance F/UF Curatorial Staff variance HKS Case Program 3 of 6 Case Number 2034.0 Tom n 01 e m d. Based on your analysis in parts (b) and (c), how can you explain the difference between the actual and budgeted amounts for the following items? i. Museum Admissions revenue i. Curatorial Staff expense In an effort to increase revenue, Jimenez is considering increasing the discounted admission price that is available to students and senior citizens. In 2008, a total of 300,000 visitors paid the reduced admission price of CS, while a total of 700,000 visitors paid the regular admission price of C15. Jimenez would like to increase the applicable price for students and senior citizens to C10, but if he does so, he believes that the total number of visits by students and senior citizens would fall by 10%. Estimate the total impact on 2008 revenues had the discounted admission price been increased for all of 2008. (By how much would it increase/decrease had this change been in effect for all of 2008?) (Note: Use reverse of page if needed) QUESTION 2 (Parts.a, b. s.d.and e) Jimenez wanted to conduct a more detailed analysis of the museum's cost structure. Specifically, he wanted to gain a better understanding of the cost to the museum of putting on Special Exhibits. Special Exhibits were often popular with the media and the general public, but Jimenez worried that they might be a financial burden on the museum. To determine the cost of Special Exhibits, Jimenez decided to use activity-based costing. His first step was to compile a table listing the allocation of each expense category to one of four activities: 1) Regular Exhibits 2) Special Exhibits 3) Curatorial Activities 4) Security Activities Jimenez could allocate certain costs directly to either Regular Exhibits or Special Exhibits, but many expenses could only be allocated to either the Curatorial Activities cost pool or the Security Activities cost pool. As a result, he needed to calculate the total cost of each cost pool and then use the appropriate cost driver to allocate the cost pool to either Regular Exhibits or Special Exhibits. He could then calculate the fully-loaded cost of Regular Exhibits and Special Exhibits and compare those costs to the revenue associated with each program. Table 2 outlines the information he has collected for his analysis. HKS Case Program 4 of 6 Case Number 2034.0 Table 2: Activity Cost Pool Allocation (%) Regular Exhibits Special Exhibits Curatorial Security Activities Activities Executive Director & fringe 35% 30% 20% 15% Director of Development & fringe 55% 35% 5% 5% Curatorial Director & fringe Administrative Staff & fringe 0% 0% 100% 0% 35% 30% 20% 15% Curatorial Staff 0% 0% 100% O% Security Guards 0% 0% 0% 100% Insurance 50% 50% 0% 0% Maintenance 67% 33% 0% 0% Utilities S0% 50% 0% 0% Mortgage 67% 33% 0% 0% Calculate the activity cost pool amounts and complete the table below. (Use 2008 Actuals from Table 1.) Regular Exhibits € 122,500 Curatorial Special Exhibits Security Activities € 70,000 Activities Total Executive Director & fringe Director of Development & fringe Curatorial Director & fringe € 105,000 €52,500 € 350,000 115,500 73,500 10,500 10,500 210,000 175,000 175,000 Administrative Staff & fringe 33,600 Curatorial Staff 2,653,350 Security Guards Insurance 3,250,000 3,250,000 6,500,000 Maintenance 787,652 387,948 1,175,600 2,618,250 3.960,000 Utilities 2,618,250 5,236,500 Mortgage Total 8.040.000 12.000,000 €2,942,450 €3,392,300 € 31,772,550 b. Circle the most appropriate cost driver for the Curatorial and Security activity cost pools. Then, complete the table below. Choose the best cost driver: A. Number of visitors B. Number of staff hours worked C. Number of special exhibits HKS Case Program Sof 6 Case Number 2034.0 Curatorial Activity cost pool Activities Security Activities Activity cost driver quantity Activity cost driver rate €18.99 Calculate the total cost of Regular Exhibits and Special Exhibits. Regular Exhibits Special Exhibits Directly allocated costs Curatorial activities Security activities Total costs d. Jimenez knows that the total revenue (indicated in below table) attributable to Regular Exhibits is C20,385,250 while the total revenue attributable to Special Exhibits is C10,394,250. Based on these figures and the total costs that he calculated in parts 2(c), what can Jimenez conclude about the financial performance of each program? Regular Exhibits Special Exhibits Revenue C20,385,250 C10,394,250 Total Costs (from 2c) Surplus / Deficit Based on the variance analysis and the activity-based costing analysis, what do you recommend on how to improve the financial performance of the museum? HKS Case Program 6of6 Case Number 2034.0 The Toliza Museum of Art In early 2009, Juan Antonio Jimenez has just begun his new position as Executive Director of the Toliza Museum of Art ("Toliza"). Toliza is a beautiful art museum located in the city of Toliza, Spain. Toliza's art collection includes a wide variety of classic and contemporary art, all housed in a forty-room museum and sculpture garden in the heart of the city. Toliza displays its art to the public in two ways: Regular Exhibits and Special Exhibits. Regular Exhibits are displayed throughout the year and feature pieces from the museum's permanent collection, which focuses on art from the Toliza area. Special Exhibits are limited-time only displays (often four to six weeks in duration) featuring pieces by renowned artists that are on loan from other museums. When Jimenez was hired as Executive Director, the Board of Directors made it clear to him that his first priority should be to analyze the museum's finances. The Board was concerned about the museum's financial performance in 2008, when Toliza operated at a deficit despite putting on three well-received Special Exhibits. Toliza's revenues came from: admissions fees, exhibits, annual memberships, donations and government grants. The expenses are primarily labor costs. In addition to Jimenez, Toliza's senior management team includes one Director of Development and one Head Curator. Other employees include four administrative staff members, seventy professional curating staff and numerous security and maintenance staff who are paid on an hourly basis. There are currently eighty-nine individuals who work part-time on security. As Jimenez strolled through one of the museum's special exhibition halls-currently featuring the early works of Pablo Picasso-he began to wonder what had caused the museum's deficit in 2008 and what financial results could be expected in 2009. Upon reaching his office, he set about to answer these questions, beginning with a review of the financial and operating data presented in Table 1. Table 1: Audited Financial and Operating Statement, 2008 (in €) 2008 Budget € 10,000,000 2008 Actual € 12,000,000 3,344,000 1,335,000 7,224,500 6.876.000 Revenue Museum Admissions Special exhibit admissions Annual memberships 3,000,000 1,560,000 Donations 7,500,000 Government grants Total Z.00.000 € 29,060,000 € 30,779,500 Expenses € 250,000 € 250,000 Executive Director (salaried) Director of Development (salaried) Head Curator (salaried) 150,000 150,000 125,000 125,000 Administrative Staff (salaried) Fringe for salaried employee @40% of salary 120,000 120,000 258,000 258,000 Curatorial Staff (paid hourly) 2,080,000 2,028,000 2,653,350 3,304,100 6,500,000 1,175,600 Security Guards (paid hourly) Insurance 4,750,000 Maintenance 1,150,000 Utilities 3,450,000 5,236,500 Mortgage Total 12.000,000 12,000,000 € 26,361,000 € 31,772,550 Total Surplus /(Deficit) €2,699,000 (€ 993,050) Operating Data Operations Museum admissions (# of visitors) 800,000 150,000 1,000,000 Special exhibit admissions (# of visitors) Annual memberships sold (# sold) 167,200 20,800 17,800 Pieces of art work on display Regular Exhibits Special Exhibits 200 210 100 105 Total pieces on display 300 315 Total hours worked by curators Regular Exhibits Special Exhibits 72,000 76,681 62.969 32.000 104,000 Total curatorial hours 139,650 Total hours worked by security guards Regular Exhibits 100,000 107,101 Special Exhibits Total security guard hours 35.200 135,200 21.449 178,600 HKS Case Program 2 of 6 Case Number 2034.0 QUESTION 1 a Prepare the total revenue, expense and surplus/deficit variances using the template, and indicate whether each of the variances is favorable or unfavorable. Actual Budgeted Variance F/UF Revenue 30,779,500 29,060,000 Expense 31,772,550 26,361,000 Surplus/Deficit -993,050 2,699,000 b. Calculate the price, quantity, and total variance for "Museum Admissions" revenue (per visitor). Actual Price Budgeted Price Quantity Variance F/UF Price variance Actual Quantity F/UF Budgeted Quantity Price Variance Quantity variance Actual Budgeted Variance F/UF Museum admissions variance Calculate the price, quantity, and total variance for "Curatorial Staff" expense (per hour). Actual Price Budgeted Price Quantity Variance F/UF Price variance Budgeted Quantity Actual Quantity Price Variance F/UF Quantity variance Actual Budgeted Variance F/UF Curatorial Staff variance HKS Case Program 3 of 6 Case Number 2034.0 Tom n 01 e m d. Based on your analysis in parts (b) and (c), how can you explain the difference between the actual and budgeted amounts for the following items? i. Museum Admissions revenue i. Curatorial Staff expense In an effort to increase revenue, Jimenez is considering increasing the discounted admission price that is available to students and senior citizens. In 2008, a total of 300,000 visitors paid the reduced admission price of CS, while a total of 700,000 visitors paid the regular admission price of C15. Jimenez would like to increase the applicable price for students and senior citizens to C10, but if he does so, he believes that the total number of visits by students and senior citizens would fall by 10%. Estimate the total impact on 2008 revenues had the discounted admission price been increased for all of 2008. (By how much would it increase/decrease had this change been in effect for all of 2008?) (Note: Use reverse of page if needed) QUESTION 2 (Parts.a, b. s.d.and e) Jimenez wanted to conduct a more detailed analysis of the museum's cost structure. Specifically, he wanted to gain a better understanding of the cost to the museum of putting on Special Exhibits. Special Exhibits were often popular with the media and the general public, but Jimenez worried that they might be a financial burden on the museum. To determine the cost of Special Exhibits, Jimenez decided to use activity-based costing. His first step was to compile a table listing the allocation of each expense category to one of four activities: 1) Regular Exhibits 2) Special Exhibits 3) Curatorial Activities 4) Security Activities Jimenez could allocate certain costs directly to either Regular Exhibits or Special Exhibits, but many expenses could only be allocated to either the Curatorial Activities cost pool or the Security Activities cost pool. As a result, he needed to calculate the total cost of each cost pool and then use the appropriate cost driver to allocate the cost pool to either Regular Exhibits or Special Exhibits. He could then calculate the fully-loaded cost of Regular Exhibits and Special Exhibits and compare those costs to the revenue associated with each program. Table 2 outlines the information he has collected for his analysis. HKS Case Program 4 of 6 Case Number 2034.0 Table 2: Activity Cost Pool Allocation (%) Regular Exhibits Special Exhibits Curatorial Security Activities Activities Executive Director & fringe 35% 30% 20% 15% Director of Development & fringe 55% 35% 5% 5% Curatorial Director & fringe Administrative Staff & fringe 0% 0% 100% 0% 35% 30% 20% 15% Curatorial Staff 0% 0% 100% O% Security Guards 0% 0% 0% 100% Insurance 50% 50% 0% 0% Maintenance 67% 33% 0% 0% Utilities S0% 50% 0% 0% Mortgage 67% 33% 0% 0% Calculate the activity cost pool amounts and complete the table below. (Use 2008 Actuals from Table 1.) Regular Exhibits € 122,500 Curatorial Special Exhibits Security Activities € 70,000 Activities Total Executive Director & fringe Director of Development & fringe Curatorial Director & fringe € 105,000 €52,500 € 350,000 115,500 73,500 10,500 10,500 210,000 175,000 175,000 Administrative Staff & fringe 33,600 Curatorial Staff 2,653,350 Security Guards Insurance 3,250,000 3,250,000 6,500,000 Maintenance 787,652 387,948 1,175,600 2,618,250 3.960,000 Utilities 2,618,250 5,236,500 Mortgage Total 8.040.000 12.000,000 €2,942,450 €3,392,300 € 31,772,550 b. Circle the most appropriate cost driver for the Curatorial and Security activity cost pools. Then, complete the table below. Choose the best cost driver: A. Number of visitors B. Number of staff hours worked C. Number of special exhibits HKS Case Program Sof 6 Case Number 2034.0 Curatorial Activity cost pool Activities Security Activities Activity cost driver quantity Activity cost driver rate €18.99 Calculate the total cost of Regular Exhibits and Special Exhibits. Regular Exhibits Special Exhibits Directly allocated costs Curatorial activities Security activities Total costs d. Jimenez knows that the total revenue (indicated in below table) attributable to Regular Exhibits is C20,385,250 while the total revenue attributable to Special Exhibits is C10,394,250. Based on these figures and the total costs that he calculated in parts 2(c), what can Jimenez conclude about the financial performance of each program? Regular Exhibits Special Exhibits Revenue C20,385,250 C10,394,250 Total Costs (from 2c) Surplus / Deficit Based on the variance analysis and the activity-based costing analysis, what do you recommend on how to improve the financial performance of the museum? HKS Case Program 6of6 Case Number 2034.0

Expert Answer:

Related Book For

Essentials of Corporate Finance

ISBN: 978-1259277214

9th edition

Authors: Stephen Ross, Randolph Westerfield, Bradford Jordan

Posted Date:

Students also viewed these accounting questions

-

Joey Moss, a recent finance graduate, has just begun his job with the investment firm of Covili and Wyatt. Paul Covili, one of the firm's founders, has been talking to Joey about the firm's...

-

The Metropolitan Museum of Art in New York City is one of the best in the world. Under an 1893 law, it must admit the public free of charge five days and two evenings a week. The Met has a long...

-

The new administrator for the art museum was concerned that the museums collection of rare 17th-century American porcelain was not recognized on the financial statements. Explain to the administrator...

-

Create a 3-panel informational brochure on threats to government computer systems and the potentials effects of these threats. To create your brochure, you can use brochure builder or another program...

-

Two processes, P 1 and P 2 , have been designed so that P 2 prints a byre stream produced by P 1 . Write a skeleton for the procedures executed by P 1 and P 2 to illustrate how they synchronize with...

-

1. Susan and Gray probably will need more information about the proposed system. Make a list of people whom they might want to interview. Also, suggest other fact finding techniques they should...

-

Your Social Security number (SSN) is unique, and with it you can construct your own personal Social Security polynomial. Let the polynomial function be defined as follows, where ai represents the ith...

-

Bishop Company has provided the estimated data that appear in rows 4 to 8 of the following spreadsheet: Required Using the spreadsheet tips that follow, construct a spreadsheet that allows you to...

-

During the year, Worldly Company issued $30,000 of common stock for cash. The company recorded revenues of $205,000, expenses of $150,000, and paid dividends of $20,000. What was Worldly's net income...

-

HealthFull Nurse-Run Clinic: Table 6.2 analyzes appointments that are lost (cannot be scheduled) because of limits to capacity. However, another problem at HealthFull Clinic is cancelled...

-

QUESTION 6 What is the proper adjusting entry at June 30, the end of the fiscal year, based on a prepaid insurance account balance before adjustment, $15,400, and unexpired amounts per analysis of...

-

REQUIRED: Cost of production report under the following assumptions: Lost units - normal, discovered at the beginning Lost units - normal, discovered at the end Lost units - abnormal, discovered when...

-

ABC, Inc., manufactures only two products: Gadget A and Gadget B. The firm uses a single, plant wide overhead rate based on direct-labor hours. Production and product-costing data are as follows:...

-

.Jean Saburit has gone over the financial statements for Saburit Parts, Inc. The income statement has been prepared on an absorption costing basis and Saburit would like to have the statement revised...

-

When a constant force is applied to an object, the acceleration of the object varies inversely with its mass. When a certain constant force acts upon an object with mass 2 kg, the acceleration of the...

-

Use the following for all 3 circuits. V1 = 9.0 V, V = 12.0 V R = 2.0 ohms, R = 4.0 ohms, R3 = 6.0 ohms, R4 = 8.0 ohms C1 = 3.0 C = 3.0 (a) Find I in circuit A (b) Find I1 in circuit B R w R3 V R R4...

-

Financial Accounting 2b (Semester 2 2021 During periods of falling prices and stable or increasing inventory levels: a. weighted average COGS > LIFO COGS > FIFO COGS b. LIFO COGS weighted average COGS

-

How has the too-big-to-fail policy been limited in the FDICIA legislation? How might limiting the too-big-to-fail policy help reduce the risk of a future banking crisis?

-

In 2014, an Action Comics No. 1, featuring the first appearance of Superman, was sold at auction for $3,207,852. The comic book was originally sold in 1938 for $.10. What was the annual increase in...

-

Consider the following abbreviated financial statements for Cabo Wabo, Inc.: What is owners' equity for 2015 and 2016? CABO WABO, INC Partial Balance Sheets as of December 31, 2015 and 2016 2015 2016...

-

Imprudential, Inc.. has an unfunded pension liability of $730 million that must be paid in 25 years. To assess the value of the firm's stock, financial analysts want to discount this liability back...

-

Assume that you must make future value estimates using the future value of 1 table (Table B.2). Which interest rate column do you use when working with the following rates? 1 8% compounded quarterly...

-

Ken Francis is offered the possibility of investing $2,745 today and in return to receive $10,000 after 15 years. What is the annual rate of interest for this investment? (Use Table B.1.) AppendixLO1

-

Ed Summers expects to invest $10,000 for 25 years, after which he wants to receive $108,347. What rate of interest must Summers earn? (Use Table B.2.) AppendixLO1

Study smarter with the SolutionInn App