The value of the assets owned by Catfish Ltd follows a lognormal distribution. The current firm value

Question:

The value of the assets owned by Catfish Ltd follows a lognormal distribution. The current firm value is $100. The firm is about to issue a zero-coupon bond with a face value of $60. The volatility of the firm's assets is 30% annualized, and the continuously-compounded risk-free rate equals 10% per annum.

(a) If the bond has a maturity of 1 year, what are the current prices of the Catfish bond and of a default-free bond with the same characteristics?

(b) If the value of the assets of Catfish would increase by $0.5 over the next second, by how much would the value of the bond change approximately?

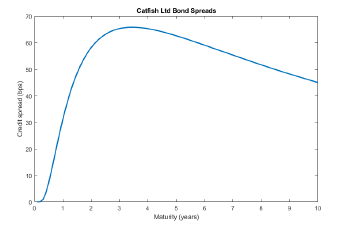

The treasurer of Catfish Ltd is considering his options (no pun intended) and examines a range of different maturities for the bond. His assistant has created the following graph showing the credit spread for a zero-coupon bond as a function of its maturity.

Expert Answer: