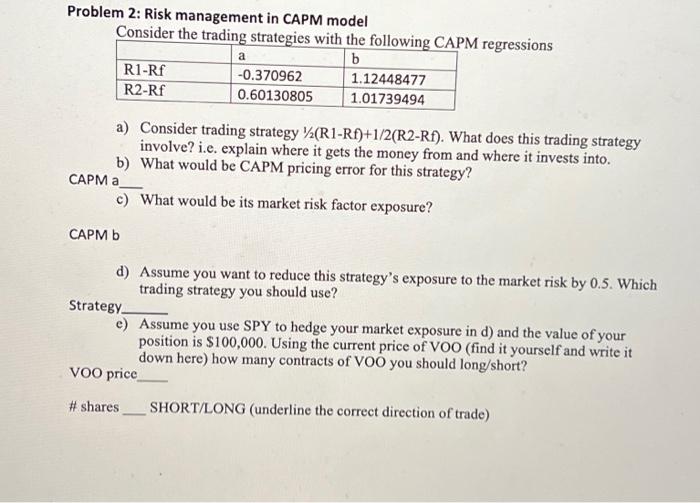

Question: There are 5 parts to this question Problem 2: Risk management in CAPM model Consider the trading strategies with the following CAPM regressions b R1-Rf

Problem 2: Risk management in CAPM model Consider the trading strategies with the following CAPM regressions b R1-Rf -0.370962 1.12448477 R2-Rf 0.60130805 1.01739494 a a) Consider trading strategy (R1-Rf)+1/2(R2-Rf). What does this trading strategy involve? i.e. explain where it gets the money from and where it invests into. b) What would be CAPM pricing error for this strategy? c) What would be its market risk factor exposure? d) Assume you want to reduce this strategy's exposure to the market risk by 0.5. Which trading strategy you should use? Strategy e) Assume you use SPY to hedge your market exposure in d) and the value of your position is $100,000. Using the current price of VOO (find it yourself and write it down here) how many contracts of VOO you should long/short? VOO price #shares SHORT/LONG (underline the correct direction of trade) Problem 2: Risk management in CAPM model Consider the trading strategies with the following CAPM regressions b R1-Rf -0.370962 1.12448477 R2-Rf 0.60130805 1.01739494 a a) Consider trading strategy (R1-Rf)+1/2(R2-Rf). What does this trading strategy involve? i.e. explain where it gets the money from and where it invests into. b) What would be CAPM pricing error for this strategy? c) What would be its market risk factor exposure? d) Assume you want to reduce this strategy's exposure to the market risk by 0.5. Which trading strategy you should use? Strategy e) Assume you use SPY to hedge your market exposure in d) and the value of your position is $100,000. Using the current price of VOO (find it yourself and write it down here) how many contracts of VOO you should long/short? VOO price #shares SHORT/LONG (underline the correct direction of trade)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts