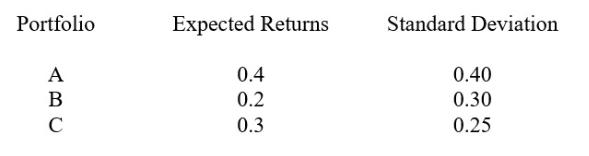

There are three distinct frontier portfolios, A, B and C. a) Compute, AB, the correlation between frontier

Fantastic news! We've Found the answer you've been seeking!

Question:

There are three distinct frontier portfolios, A, B and C.

a) Compute, ρAB, the correlation between frontier portfolios A and B.

b) Calculate the expected return on the global minimum variance portfolio.

c) Calculate the maximum possible Sharpe Ratio from these frontier portfolios, when the risk free rate is 2% per annum.

Expert Answer:

Related Book For

The Legal and Regulatory Environment of Business

ISBN: 978-0078023859

17th edition

Authors: Marisa Pagnattaro, Daniel Cahoy, Manning Magid, Lee Reed, Pe

Posted Date: