Question: There is a article named,Differences in Auditors' Materiality Assessments When Auditing Financial Statements and Sustainability Reports. I wonder that the fifth paragraph that is supplementary

There is a article named,"Differences in Auditors' Materiality Assessments When Auditing Financial Statements and Sustainability Reports".

I wonder that the fifth paragraph that is supplementary analysis, can u summarise it and explain it as clear as possible

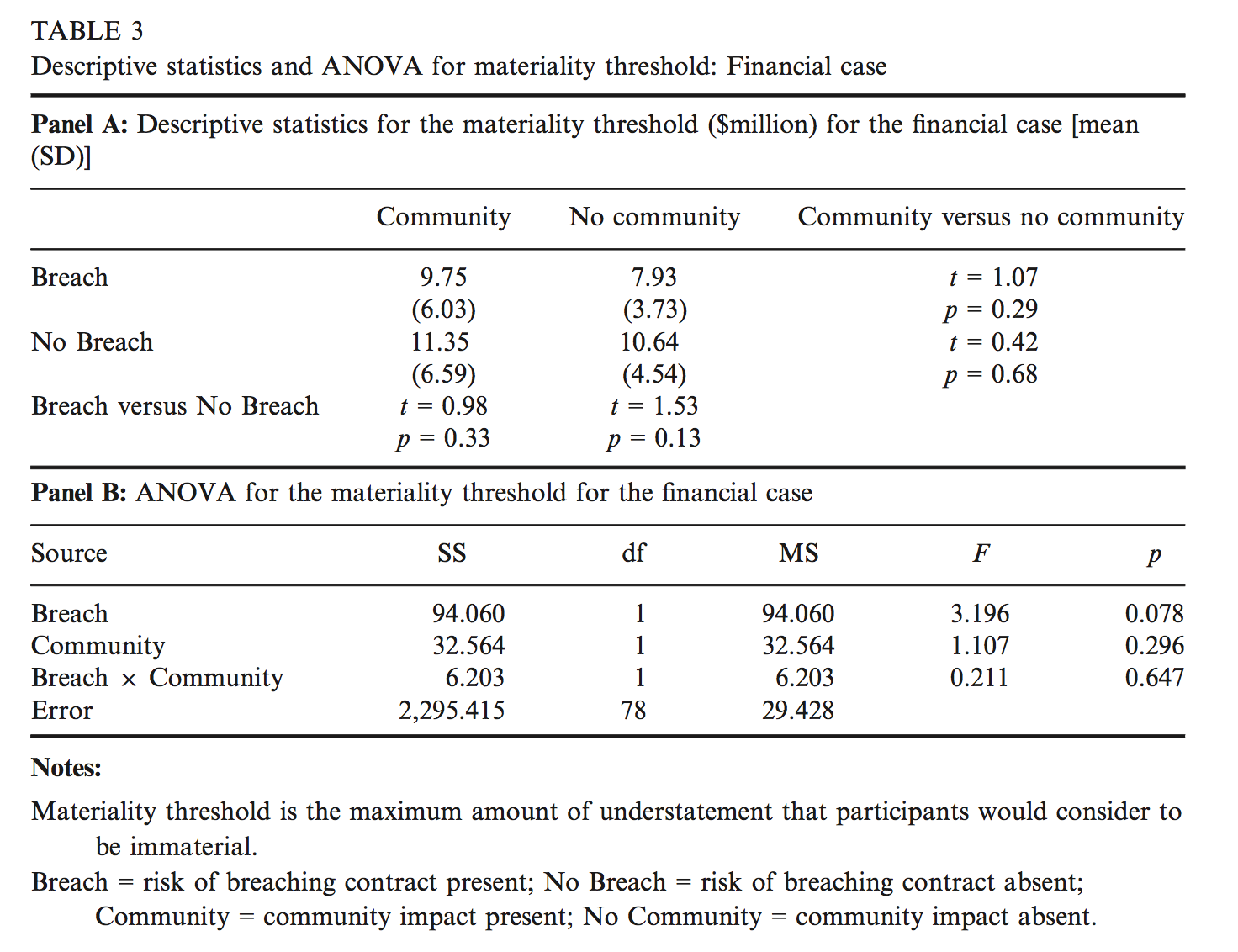

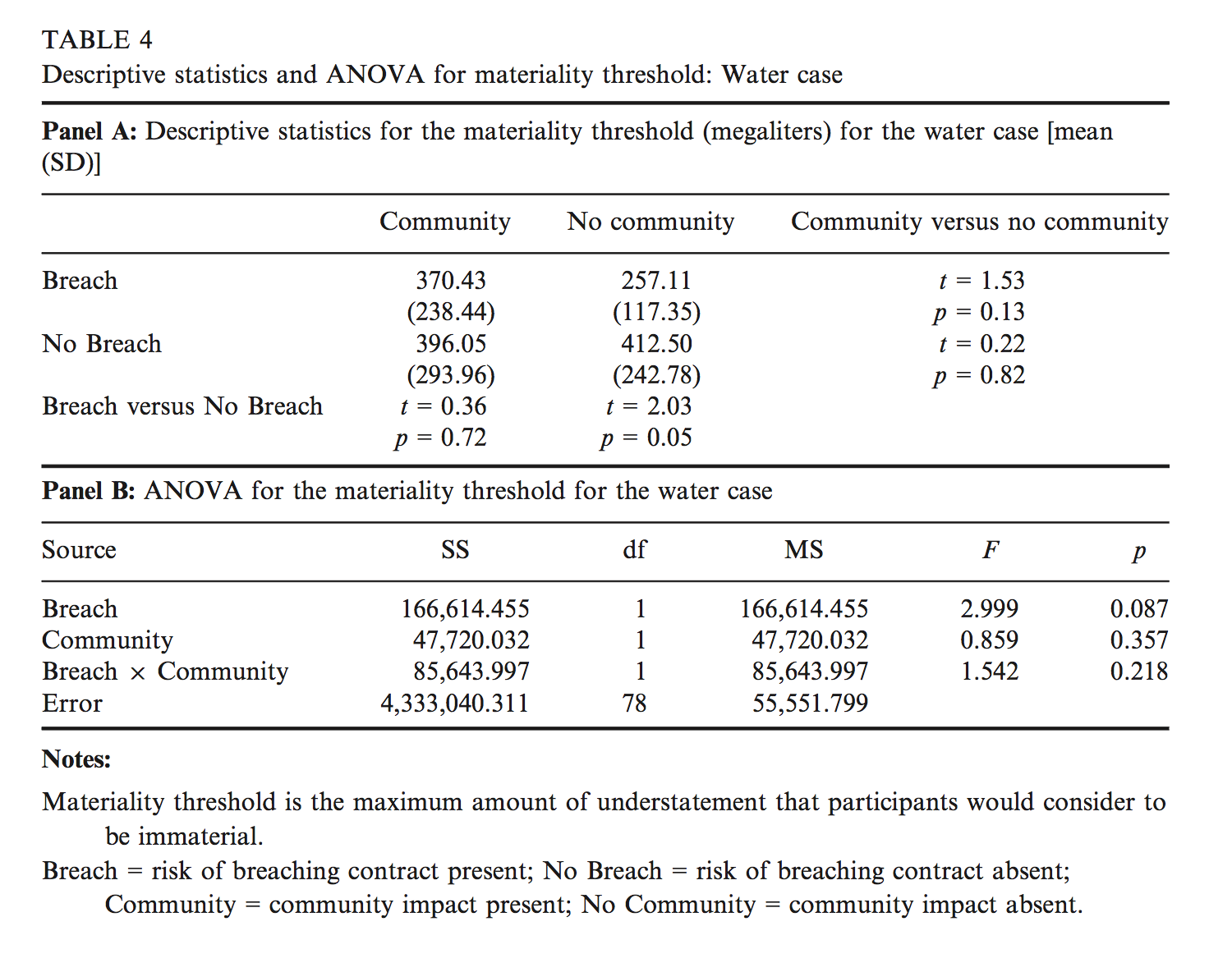

After assessing the materiality of each audit difference, participants were asked to indicate the maximum amount of understatement that they would consider to be immaterial for each of the two cases which represents the participant's materiality thresholds. Because the materiality thresholds for nancial and water are on different scales (dollars and W) and there is potentially some disagreement on what base should be used to determine a water materiality threshold,14 we examine the nancial and water materiality thresholds separately and compare the results using the dollar and Wamounts indicated as the basis for analysis. Table 3 contains the analysis for the nancial case and Table 4 contains the analysis for the water case. In interpreting the means in Tables 3 and 4, it should be noted that ahigh score in Table 1 (whether \"materially missta \") will likely be associated with a low score in Tables 3 and 4; that is, a higher materiality assessment would be consistent with a lower materiality threshold, and vice versa.15 Table 3, panel A provides the mean materiality thresholds set by participants for the nancial case. Panel B shows the 292 between-subjects AN OVA with the breacho breach and communityo community treatments. There is a marginally signicant main effect for breach (E = 3.196, p = 0.078, two-tailed) with participants setting a lower materiality threshold when there is a risk of breaching a contract than when there is no risk, but no signicant community effect (p = 0.296) or interaction (p = 0.647). This margin- ally signicant main effect for breach is inconsistent with the main analysis where there was an insignicant breach effect for the nancial case (see Table 2, panel B). This inconsistency can be explained by differences in the task. When assessing the materiality of an audit difference of 6.6 percent of net prot, auditors are less likely to respond to the risk of breaching a contract because it is already over the 5 percent benchmark suggested in audit standards. However, when setting a materiality threshold, it would likely be considered as a qualitative factor. The contrast examined earlier [2, 2, 1, 3], which tests both the main effect and the interaction, is not signicant (t = 1.538, p = 0.13, two tailed, not tabulated). None of the simple effects included in panel A are signicant (p 2 0.1, two- tailed). Table 4 provides details of the analysis conducted for the water case. The AN OVA in Table 4, panel B shows a marginally signicant main effect for breach (E = 2.999, p = 0.087, two-tailed) with participants setting a lower materiality threshold when there is a risk of breaching a contract than when there is no risk. The contrast [ 2, 2, 1, 3] as described above, is marginally signicant (t = 1.699, p = 0.09, two-tailed not tabulated) and the only signicant simple effect is for breach in the absence of community (t = 2.03, p = 0.05, two- tailed) (Table 4, panel A). Overall this indicates that participants set a lower threshold when there is a risk of breaching a contract than when there is no risk of breaching a contract and this breach effect is only signicant in the no community treatment.16 The pattern of results presented in Table 1 and Table 4 are somewhat different for the water case. In both instances, the only signicant simple effect is for breach in the absence of community. However, in Table 1, this result is driven by the no breacho community cell while' in Table 4 this result' is driven by the breachlno community cell. To better understand this difference, we arranged W interviews with two of the partners (from two different Big 4 rms) who had provided input to designing the cases. One of the authors held a face-to-face meeting with each of them and explained the results of our study both verbally and diagrammatically. Partners were not surprised that auditors assessed materiality higher for the nancial case than for the water case as liability risk is greater for a nancial statement audit. Explanations referred to the consequences of get ting it wrong as being much greater and more visible for a nancial audit. They referred to scientic uncertainty when assuring water reports and the greater precision in audit standards compared to sustainability assurance standards with respect to materiality would result in greater variation between materiality judgments for the water report engagement compared to the nancial engagement. The partners indicated that the nding that the lowest materiality assessment was for the no breacho community treatment was consistent with their expectations. However, when asked to speculate on why the materiality threshold was lowest in the absence of a community rather than in the presence of a community for the water case, they suggested that when setting a materiality threshold in the absence of a community, the focus is only on shareholders. With the effects on share- holders becoming more salient, it may encourage greater conservatism where there is a risk of breaching a contract, resulting in the lowest threshold in the breacho community treatment. Nevertheless, it is not clear why these effects would differ between the two tasks. Further inspection of the data for the water case showed that the breacho com- munity treatment had the lowest variance (117.35) of the four cells (see Table 4, panel A) (F = 4.698; p = 0.033, not tabulated). One reason for this is that the proportion of individuals indicating a threshold consistent with the breach limit (i .e., setting a materiality threshold at the amount where the breach would cut in) was higher for the breacho community treatment than the breach/community treatment (11 of 18 in cell 2 compared toSoi'ZfiinceLg2 =2.815;p=0 .09). Libby and Brown (2013) in a study that examines materiality judgments for a nancial statement case nd differences in their results between Likert scale materiality assessments and an allowable error measure. They note that their study plus previous research and discussions with representatives of the major audit rms suggest the prominence of a thresh- old of 5 percent of pre-tax income as the nominal quantitative benchmark and that smaller errors require the consideration of qualitative factors. No such guidelines appear for water reports. The fact that these task effects exist in both nancial statement materiality judgments where the differences are below 5 percent of a base (Libby and Brown 2013) and in our study for sustainability reports, where the differences are above 5 percent of a base, suggests the need for future research to examine these task differences. In fact, this call for further research on task effects follows a long line of similar calls (e.g., Ashton 1990; Bonner 1994; Nelson and Tan 2005; Trotman 2005). TABLE 3 Descriptive statistics and ANOVA for materiality threshold: Financial case Panel A: Descriptive statistics for the materiality threshold ($million) for the nancial case [mean (SD)] Community No community Community versus no community Breach 9.75 7.93 t = 1.07 (6.03) (3.73) p = 0.29 No Breach 11.35 10.64 t = 0.42 (6.59) (4.54) p = 0.68 Breach versus No Breach t = 0.98 I = 1.53 p = 0.33 p = 0.13 Panel B: ANOVA for the materiality threshold for the nancial case Source SS df MS F p Breach 94.060 1 94.060 3.196 0.078 Community 32.564 1 32.564 1.107 0.296 Breach X Community 6.203 1 6.203 0.211 0.647 Error 2,295.415 78 29.428 Notes: Materiality threshold is the maximum amount of understatement that participants would consider to be immaterial. Breach = risk of breaching contract present; No Breach = risk of breaching contract absent; Community = community impact present; No Community = community impact absent. TABLE 4 Descriptive statistics and ANOVA for materiality threshold: Water case Panel A: Descriptive statistics for the materiality threshold (megaliters) for the water case [mean (SD)] Community No community Community versus no community Breach 370.43 257.11 at = 1.53 (238.44) (117.35) p = 0.13 No Breach 396.05 412.50 t = 0.22 (293.96) (242.78) p = 0.82 Breach versus No Breach t = 0.36 t = 2.03 p = 0.72 p = 0.05 Panel B: ANOVA for the materiality threshold for the water case Source SS df MS F p Breach 166,614.455 1 166,614.455 2.999 0.087 Community 47,720.032 1 47,720.032 0.859 0.357 Breach x Community 85,643.997 1 85,643.997 1.542 0.218 Error 4,333,040.311 78 55,551.799 Notes: Materiality threshold is the maximum amount of understatement that participants would consider to be immaterial. Breach = risk of breaching contract present; No Breach = risk of breaching contract absent; Community = community impact present; No Community = community impact absent

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts