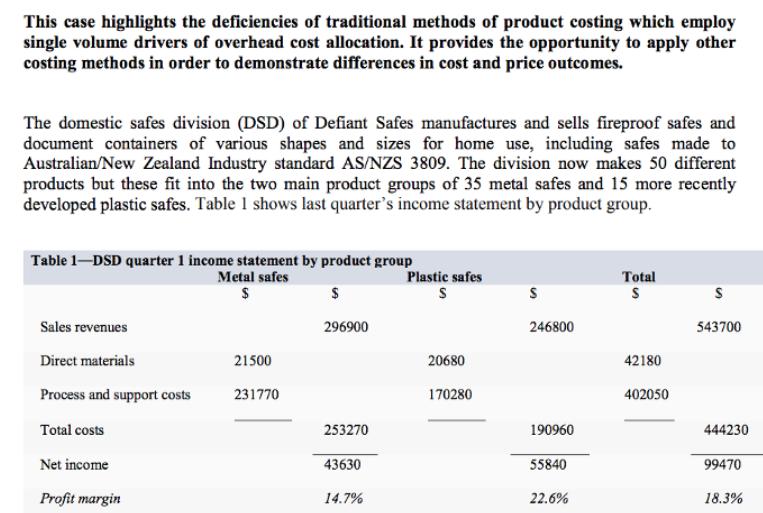

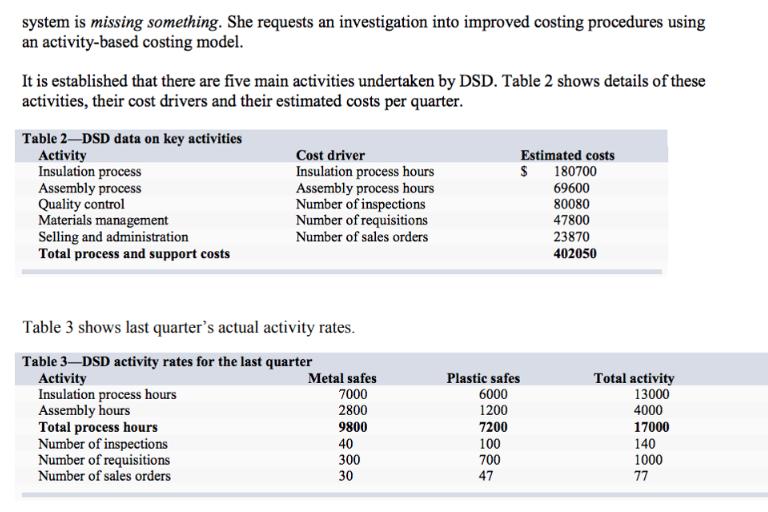

This case highlights the deficiencies of traditional methods of product costing which employ single volume drivers...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

This case highlights the deficiencies of traditional methods of product costing which employ single volume drivers of overhead cost allocation. It provides the opportunity to apply other costing methods in order to demonstrate differences in cost and price outcomes. The domestic safes division (DSD) of Defiant Safes manufactures and sells fireproof safes and document containers of various shapes and sizes for home use, including safes made to Australian/New Zealand Industry standard AS/NZS 3809. The division now makes 50 different products but these fit into the two main product groups of 35 metal safes and 15 more recently developed plastic safes. Table 1 shows last quarter's income statement by product group. Table 1-DSD quarter 1 income statement by product group Metal safes $ $ 296900 Sales revenues Direct materials Process and support costs Total costs Net income Profit margin 21500 231770 253270 43630 14.7% Plastic safes S 20680 170280 S 246800 190960 55840 22.6% Total S 42180 402050 S 543700 444230 99470 18.3% system is missing something. She requests an investigation into improved costing procedures using an activity-based costing model. It is established that there are five main activities undertaken by DSD. Table 2 shows details of these activities, their cost drivers and their estimated costs per quarter. Table 2-DSD data on key activities Activity Insulation process Assembly process Quality control Materials management Selling and administration Total process and support costs Cost driver Insulation process hours Assembly process hours Number of inspections Number of requisitions Number of sales orders Table 3 shows last quarter's actual activity rates. Table 3-DSD activity rates for the last quarter Activity Insulation process hours Assembly hours Total process hours Number of inspections Number of requisitions Number of sales orders Metal safes 7000 2800 9800 40 300 30 Estimated costs $ 180700 69600 80080 47800 23870 402050 Plastic safes 6000 1200 7200 100 700 47 Total activity 13000 4000 17000 140 1000 77 The assembly process for plastic safes is quite complex and there has recently been a high level of rejects. This has resulted in the need for increased quality control activities. Plastic safes generally comprise more components than metal safes, causing more material movements. The plastic safe product group is still new and DSD's customer base is characterised by a large number of customers each ordering small volumes. Required: 1. Explain the general problems associated with DSD's traditional costing system and highlight any indicators that the current costing system is outdated and flawed. 2. Calculate the activity rates to be used in the desired activity-based costing system and produce a revised income statement by product group tracing process and support costs to product groups using activity-based costing methodology. Explain the key differences in product costs and net profit margins between the two alternative costing systems. 3. 4. Provide advice to the managing director, stating key reasons, as to which costing system produces the most useful information for management. Also state your recommendations in respect of product strategy as a result of the information produced. You are required to present your answers in a group presentation with maximum duration of 10 minutes. No individual presentation is allowed. Each student within the group must participate and deliver the presentation. Each student should speak for a minimum of 2 minutes. This case highlights the deficiencies of traditional methods of product costing which employ single volume drivers of overhead cost allocation. It provides the opportunity to apply other costing methods in order to demonstrate differences in cost and price outcomes. The domestic safes division (DSD) of Defiant Safes manufactures and sells fireproof safes and document containers of various shapes and sizes for home use, including safes made to Australian/New Zealand Industry standard AS/NZS 3809. The division now makes 50 different products but these fit into the two main product groups of 35 metal safes and 15 more recently developed plastic safes. Table 1 shows last quarter's income statement by product group. Table 1-DSD quarter 1 income statement by product group Metal safes $ $ 296900 Sales revenues Direct materials Process and support costs Total costs Net income Profit margin 21500 231770 253270 43630 14.7% Plastic safes S 20680 170280 S 246800 190960 55840 22.6% Total S 42180 402050 S 543700 444230 99470 18.3% system is missing something. She requests an investigation into improved costing procedures using an activity-based costing model. It is established that there are five main activities undertaken by DSD. Table 2 shows details of these activities, their cost drivers and their estimated costs per quarter. Table 2-DSD data on key activities Activity Insulation process Assembly process Quality control Materials management Selling and administration Total process and support costs Cost driver Insulation process hours Assembly process hours Number of inspections Number of requisitions Number of sales orders Table 3 shows last quarter's actual activity rates. Table 3-DSD activity rates for the last quarter Activity Insulation process hours Assembly hours Total process hours Number of inspections Number of requisitions Number of sales orders Metal safes 7000 2800 9800 40 300 30 Estimated costs $ 180700 69600 80080 47800 23870 402050 Plastic safes 6000 1200 7200 100 700 47 Total activity 13000 4000 17000 140 1000 77 The assembly process for plastic safes is quite complex and there has recently been a high level of rejects. This has resulted in the need for increased quality control activities. Plastic safes generally comprise more components than metal safes, causing more material movements. The plastic safe product group is still new and DSD's customer base is characterised by a large number of customers each ordering small volumes. Required: 1. Explain the general problems associated with DSD's traditional costing system and highlight any indicators that the current costing system is outdated and flawed. 2. Calculate the activity rates to be used in the desired activity-based costing system and produce a revised income statement by product group tracing process and support costs to product groups using activity-based costing methodology. Explain the key differences in product costs and net profit margins between the two alternative costing systems. 3. 4. Provide advice to the managing director, stating key reasons, as to which costing system produces the most useful information for management. Also state your recommendations in respect of product strategy as a result of the information produced. You are required to present your answers in a group presentation with maximum duration of 10 minutes. No individual presentation is allowed. Each student within the group must participate and deliver the presentation. Each student should speak for a minimum of 2 minutes. This case highlights the deficiencies of traditional methods of product costing which employ single volume drivers of overhead cost allocation. It provides the opportunity to apply other costing methods in order to demonstrate differences in cost and price outcomes. The domestic safes division (DSD) of Defiant Safes manufactures and sells fireproof safes and document containers of various shapes and sizes for home use, including safes made to Australian/New Zealand Industry standard AS/NZS 3809. The division now makes 50 different products but these fit into the two main product groups of 35 metal safes and 15 more recently developed plastic safes. Table 1 shows last quarter's income statement by product group. Table 1-DSD quarter 1 income statement by product group Metal safes $ $ 296900 Sales revenues Direct materials Process and support costs Total costs Net income Profit margin 21500 231770 253270 43630 14.7% Plastic safes S 20680 170280 S 246800 190960 55840 22.6% Total S 42180 402050 S 543700 444230 99470 18.3% system is missing something. She requests an investigation into improved costing procedures using an activity-based costing model. It is established that there are five main activities undertaken by DSD. Table 2 shows details of these activities, their cost drivers and their estimated costs per quarter. Table 2-DSD data on key activities Activity Insulation process Assembly process Quality control Materials management Selling and administration Total process and support costs Cost driver Insulation process hours Assembly process hours Number of inspections Number of requisitions Number of sales orders Table 3 shows last quarter's actual activity rates. Table 3-DSD activity rates for the last quarter Activity Insulation process hours Assembly hours Total process hours Number of inspections Number of requisitions Number of sales orders Metal safes 7000 2800 9800 40 300 30 Estimated costs $ 180700 69600 80080 47800 23870 402050 Plastic safes 6000 1200 7200 100 700 47 Total activity 13000 4000 17000 140 1000 77 The assembly process for plastic safes is quite complex and there has recently been a high level of rejects. This has resulted in the need for increased quality control activities. Plastic safes generally comprise more components than metal safes, causing more material movements. The plastic safe product group is still new and DSD's customer base is characterised by a large number of customers each ordering small volumes. Required: 1. Explain the general problems associated with DSD's traditional costing system and highlight any indicators that the current costing system is outdated and flawed. 2. Calculate the activity rates to be used in the desired activity-based costing system and produce a revised income statement by product group tracing process and support costs to product groups using activity-based costing methodology. Explain the key differences in product costs and net profit margins between the two alternative costing systems. 3. 4. Provide advice to the managing director, stating key reasons, as to which costing system produces the most useful information for management. Also state your recommendations in respect of product strategy as a result of the information produced. You are required to present your answers in a group presentation with maximum duration of 10 minutes. No individual presentation is allowed. Each student within the group must participate and deliver the presentation. Each student should speak for a minimum of 2 minutes. This case highlights the deficiencies of traditional methods of product costing which employ single volume drivers of overhead cost allocation. It provides the opportunity to apply other costing methods in order to demonstrate differences in cost and price outcomes. The domestic safes division (DSD) of Defiant Safes manufactures and sells fireproof safes and document containers of various shapes and sizes for home use, including safes made to Australian/New Zealand Industry standard AS/NZS 3809. The division now makes 50 different products but these fit into the two main product groups of 35 metal safes and 15 more recently developed plastic safes. Table 1 shows last quarter's income statement by product group. Table 1-DSD quarter 1 income statement by product group Metal safes $ $ 296900 Sales revenues Direct materials Process and support costs Total costs Net income Profit margin 21500 231770 253270 43630 14.7% Plastic safes S 20680 170280 S 246800 190960 55840 22.6% Total S 42180 402050 S 543700 444230 99470 18.3% system is missing something. She requests an investigation into improved costing procedures using an activity-based costing model. It is established that there are five main activities undertaken by DSD. Table 2 shows details of these activities, their cost drivers and their estimated costs per quarter. Table 2-DSD data on key activities Activity Insulation process Assembly process Quality control Materials management Selling and administration Total process and support costs Cost driver Insulation process hours Assembly process hours Number of inspections Number of requisitions Number of sales orders Table 3 shows last quarter's actual activity rates. Table 3-DSD activity rates for the last quarter Activity Insulation process hours Assembly hours Total process hours Number of inspections Number of requisitions Number of sales orders Metal safes 7000 2800 9800 40 300 30 Estimated costs $ 180700 69600 80080 47800 23870 402050 Plastic safes 6000 1200 7200 100 700 47 Total activity 13000 4000 17000 140 1000 77 The assembly process for plastic safes is quite complex and there has recently been a high level of rejects. This has resulted in the need for increased quality control activities. Plastic safes generally comprise more components than metal safes, causing more material movements. The plastic safe product group is still new and DSD's customer base is characterised by a large number of customers each ordering small volumes. Required: 1. Explain the general problems associated with DSD's traditional costing system and highlight any indicators that the current costing system is outdated and flawed. 2. Calculate the activity rates to be used in the desired activity-based costing system and produce a revised income statement by product group tracing process and support costs to product groups using activity-based costing methodology. Explain the key differences in product costs and net profit margins between the two alternative costing systems. 3. 4. Provide advice to the managing director, stating key reasons, as to which costing system produces the most useful information for management. Also state your recommendations in respect of product strategy as a result of the information produced. You are required to present your answers in a group presentation with maximum duration of 10 minutes. No individual presentation is allowed. Each student within the group must participate and deliver the presentation. Each student should speak for a minimum of 2 minutes. This case highlights the deficiencies of traditional methods of product costing which employ single volume drivers of overhead cost allocation. It provides the opportunity to apply other costing methods in order to demonstrate differences in cost and price outcomes. The domestic safes division (DSD) of Defiant Safes manufactures and sells fireproof safes and document containers of various shapes and sizes for home use, including safes made to Australian/New Zealand Industry standard AS/NZS 3809. The division now makes 50 different products but these fit into the two main product groups of 35 metal safes and 15 more recently developed plastic safes. Table 1 shows last quarter's income statement by product group. Table 1-DSD quarter 1 income statement by product group Metal safes $ $ 296900 Sales revenues Direct materials Process and support costs Total costs Net income Profit margin 21500 231770 253270 43630 14.7% Plastic safes S 20680 170280 S 246800 190960 55840 22.6% Total S 42180 402050 S 543700 444230 99470 18.3% system is missing something. She requests an investigation into improved costing procedures using an activity-based costing model. It is established that there are five main activities undertaken by DSD. Table 2 shows details of these activities, their cost drivers and their estimated costs per quarter. Table 2-DSD data on key activities Activity Insulation process Assembly process Quality control Materials management Selling and administration Total process and support costs Cost driver Insulation process hours Assembly process hours Number of inspections Number of requisitions Number of sales orders Table 3 shows last quarter's actual activity rates. Table 3-DSD activity rates for the last quarter Activity Insulation process hours Assembly hours Total process hours Number of inspections Number of requisitions Number of sales orders Metal safes 7000 2800 9800 40 300 30 Estimated costs $ 180700 69600 80080 47800 23870 402050 Plastic safes 6000 1200 7200 100 700 47 Total activity 13000 4000 17000 140 1000 77 The assembly process for plastic safes is quite complex and there has recently been a high level of rejects. This has resulted in the need for increased quality control activities. Plastic safes generally comprise more components than metal safes, causing more material movements. The plastic safe product group is still new and DSD's customer base is characterised by a large number of customers each ordering small volumes. Required: 1. Explain the general problems associated with DSD's traditional costing system and highlight any indicators that the current costing system is outdated and flawed. 2. Calculate the activity rates to be used in the desired activity-based costing system and produce a revised income statement by product group tracing process and support costs to product groups using activity-based costing methodology. Explain the key differences in product costs and net profit margins between the two alternative costing systems. 3. 4. Provide advice to the managing director, stating key reasons, as to which costing system produces the most useful information for management. Also state your recommendations in respect of product strategy as a result of the information produced. You are required to present your answers in a group presentation with maximum duration of 10 minutes. No individual presentation is allowed. Each student within the group must participate and deliver the presentation. Each student should speak for a minimum of 2 minutes. This case highlights the deficiencies of traditional methods of product costing which employ single volume drivers of overhead cost allocation. It provides the opportunity to apply other costing methods in order to demonstrate differences in cost and price outcomes. The domestic safes division (DSD) of Defiant Safes manufactures and sells fireproof safes and document containers of various shapes and sizes for home use, including safes made to Australian/New Zealand Industry standard AS/NZS 3809. The division now makes 50 different products but these fit into the two main product groups of 35 metal safes and 15 more recently developed plastic safes. Table 1 shows last quarter's income statement by product group. Table 1-DSD quarter 1 income statement by product group Metal safes $ $ 296900 Sales revenues Direct materials Process and support costs Total costs Net income Profit margin 21500 231770 253270 43630 14.7% Plastic safes S 20680 170280 S 246800 190960 55840 22.6% Total S 42180 402050 S 543700 444230 99470 18.3% system is missing something. She requests an investigation into improved costing procedures using an activity-based costing model. It is established that there are five main activities undertaken by DSD. Table 2 shows details of these activities, their cost drivers and their estimated costs per quarter. Table 2-DSD data on key activities Activity Insulation process Assembly process Quality control Materials management Selling and administration Total process and support costs Cost driver Insulation process hours Assembly process hours Number of inspections Number of requisitions Number of sales orders Table 3 shows last quarter's actual activity rates. Table 3-DSD activity rates for the last quarter Activity Insulation process hours Assembly hours Total process hours Number of inspections Number of requisitions Number of sales orders Metal safes 7000 2800 9800 40 300 30 Estimated costs $ 180700 69600 80080 47800 23870 402050 Plastic safes 6000 1200 7200 100 700 47 Total activity 13000 4000 17000 140 1000 77 The assembly process for plastic safes is quite complex and there has recently been a high level of rejects. This has resulted in the need for increased quality control activities. Plastic safes generally comprise more components than metal safes, causing more material movements. The plastic safe product group is still new and DSD's customer base is characterised by a large number of customers each ordering small volumes. Required: 1. Explain the general problems associated with DSD's traditional costing system and highlight any indicators that the current costing system is outdated and flawed. 2. Calculate the activity rates to be used in the desired activity-based costing system and produce a revised income statement by product group tracing process and support costs to product groups using activity-based costing methodology. Explain the key differences in product costs and net profit margins between the two alternative costing systems. 3. 4. Provide advice to the managing director, stating key reasons, as to which costing system produces the most useful information for management. Also state your recommendations in respect of product strategy as a result of the information produced. You are required to present your answers in a group presentation with maximum duration of 10 minutes. No individual presentation is allowed. Each student within the group must participate and deliver the presentation. Each student should speak for a minimum of 2 minutes. This case highlights the deficiencies of traditional methods of product costing which employ single volume drivers of overhead cost allocation. It provides the opportunity to apply other costing methods in order to demonstrate differences in cost and price outcomes. The domestic safes division (DSD) of Defiant Safes manufactures and sells fireproof safes and document containers of various shapes and sizes for home use, including safes made to Australian/New Zealand Industry standard AS/NZS 3809. The division now makes 50 different products but these fit into the two main product groups of 35 metal safes and 15 more recently developed plastic safes. Table 1 shows last quarter's income statement by product group. Table 1-DSD quarter 1 income statement by product group Metal safes $ $ 296900 Sales revenues Direct materials Process and support costs Total costs Net income Profit margin 21500 231770 253270 43630 14.7% Plastic safes S 20680 170280 S 246800 190960 55840 22.6% Total S 42180 402050 S 543700 444230 99470 18.3% system is missing something. She requests an investigation into improved costing procedures using an activity-based costing model. It is established that there are five main activities undertaken by DSD. Table 2 shows details of these activities, their cost drivers and their estimated costs per quarter. Table 2-DSD data on key activities Activity Insulation process Assembly process Quality control Materials management Selling and administration Total process and support costs Cost driver Insulation process hours Assembly process hours Number of inspections Number of requisitions Number of sales orders Table 3 shows last quarter's actual activity rates. Table 3-DSD activity rates for the last quarter Activity Insulation process hours Assembly hours Total process hours Number of inspections Number of requisitions Number of sales orders Metal safes 7000 2800 9800 40 300 30 Estimated costs $ 180700 69600 80080 47800 23870 402050 Plastic safes 6000 1200 7200 100 700 47 Total activity 13000 4000 17000 140 1000 77 The assembly process for plastic safes is quite complex and there has recently been a high level of rejects. This has resulted in the need for increased quality control activities. Plastic safes generally comprise more components than metal safes, causing more material movements. The plastic safe product group is still new and DSD's customer base is characterised by a large number of customers each ordering small volumes. Required: 1. Explain the general problems associated with DSD's traditional costing system and highlight any indicators that the current costing system is outdated and flawed. 2. Calculate the activity rates to be used in the desired activity-based costing system and produce a revised income statement by product group tracing process and support costs to product groups using activity-based costing methodology. Explain the key differences in product costs and net profit margins between the two alternative costing systems. 3. 4. Provide advice to the managing director, stating key reasons, as to which costing system produces the most useful information for management. Also state your recommendations in respect of product strategy as a result of the information produced. You are required to present your answers in a group presentation with maximum duration of 10 minutes. No individual presentation is allowed. Each student within the group must participate and deliver the presentation. Each student should speak for a minimum of 2 minutes. This case highlights the deficiencies of traditional methods of product costing which employ single volume drivers of overhead cost allocation. It provides the opportunity to apply other costing methods in order to demonstrate differences in cost and price outcomes. The domestic safes division (DSD) of Defiant Safes manufactures and sells fireproof safes and document containers of various shapes and sizes for home use, including safes made to Australian/New Zealand Industry standard AS/NZS 3809. The division now makes 50 different products but these fit into the two main product groups of 35 metal safes and 15 more recently developed plastic safes. Table 1 shows last quarter's income statement by product group. Table 1-DSD quarter 1 income statement by product group Metal safes $ $ 296900 Sales revenues Direct materials Process and support costs Total costs Net income Profit margin 21500 231770 253270 43630 14.7% Plastic safes S 20680 170280 S 246800 190960 55840 22.6% Total S 42180 402050 S 543700 444230 99470 18.3% system is missing something. She requests an investigation into improved costing procedures using an activity-based costing model. It is established that there are five main activities undertaken by DSD. Table 2 shows details of these activities, their cost drivers and their estimated costs per quarter. Table 2-DSD data on key activities Activity Insulation process Assembly process Quality control Materials management Selling and administration Total process and support costs Cost driver Insulation process hours Assembly process hours Number of inspections Number of requisitions Number of sales orders Table 3 shows last quarter's actual activity rates. Table 3-DSD activity rates for the last quarter Activity Insulation process hours Assembly hours Total process hours Number of inspections Number of requisitions Number of sales orders Metal safes 7000 2800 9800 40 300 30 Estimated costs $ 180700 69600 80080 47800 23870 402050 Plastic safes 6000 1200 7200 100 700 47 Total activity 13000 4000 17000 140 1000 77 The assembly process for plastic safes is quite complex and there has recently been a high level of rejects. This has resulted in the need for increased quality control activities. Plastic safes generally comprise more components than metal safes, causing more material movements. The plastic safe product group is still new and DSD's customer base is characterised by a large number of customers each ordering small volumes. Required: 1. Explain the general problems associated with DSD's traditional costing system and highlight any indicators that the current costing system is outdated and flawed. 2. Calculate the activity rates to be used in the desired activity-based costing system and produce a revised income statement by product group tracing process and support costs to product groups using activity-based costing methodology. Explain the key differences in product costs and net profit margins between the two alternative costing systems. 3. 4. Provide advice to the managing director, stating key reasons, as to which costing system produces the most useful information for management. Also state your recommendations in respect of product strategy as a result of the information produced. You are required to present your answers in a group presentation with maximum duration of 10 minutes. No individual presentation is allowed. Each student within the group must participate and deliver the presentation. Each student should speak for a minimum of 2 minutes.

Expert Answer:

Answer rating: 100% (QA)

1 The company currently used traditional costing system of allocating process and support costs to t... View the full answer

Related Book For

Human Resource Management

ISBN: 978-1305500709

15th edition

Authors: Robert Mathis, John Jackson, Sean Valentine, Patricia Meglich

Posted Date:

Students also viewed these marketing questions

-

This case highlights the challenges of employee retention during stressful and unpredictable times when Xerox was undergoing a significant shift in its strategic focus. (For the case, go to...

-

You are an information technology (IT) intern working for Health Network, Inc. (Health Network), a fictitious health services organization headquartered in Minneapolis, Minnesota. Health Network has...

-

This case highlights the issues of recruitment outsourc- ing and methods used to recruit for scarce skills. Blueberry is a subsidiary of a multinational IT com- pany based in the US, Globalchip, and...

-

/* FILE: FLIX2YOU_data-load.txt */ /* Script to populate tables for FLIX2YOU .. current schema before revision */ /* Written by Gary Heberling on July 2, 2012 */ /* For IST210 world campus Penn State...

-

Zander Consulting, a real estate consulting firm, specializes in advising companies on potential new plant sites. The firm uses a job cost system with a predetermined indirect cost allocation rate...

-

Suppose that X and Y have the following joint probability function:(a) Find the expected value of g(X, Y) = XY2.(b) Find ?x and ?y. fix,v) 2 4 0.10 0.15 0.30 0.15 0.20 0.10 5

-

An income statement is a summary of a companys revenues and costs over a given period time. The data in the file bellevuebakery is an example of an income statement. It contains the revenues and...

-

Gila Corporation earned $2,650,000 during 2014. The company had an average of 520,000 shares of common stock outstanding. The average market price of common stock was $32 per share during the year....

-

1. While improper framing could affect the information we have on sark attacks, I think our decisions come down to "anchoring and adjustment". Because the information we received from the media was...

-

A small rock with mass 0.10 kg is released from rest at point. A, which is at the top edge of a large, hemispherical bowl with radius R=0.60 m (the figure (Figure 1)). Assume that the size of the...

-

1. Find the equation of the circle with radius 5 and center (-2, 4). 2. Find the equation of the circle with radius r and center (0, 1). 3. Find the equation of the circle with radius 4 7 and center...

-

If yield curves, on average, were flat, what would this say about the liquidity premiums in the term structure? Would you be more or less willing to accept the pure expectations theory? A. The...

-

Create a list of ten (10) questions to ask him or her that are related to discourse in your field. For instance, you might ask about what types of speaking events the person is involved in, how...

-

Consider an interest-only closed Canadian mortgage. It is offered over 15 years; has monthly payments; the contract mortgage rate is 3%; the mortgage amount is $800,000; the roll-over period is 3...

-

A Garment Company "You are on the management team of a private apparel company. The fundamental philosophy behind the company is that apparel manufacturing should be profitable without exploiting...

-

How to design an activity to use to develop Grade R learners literality skill. Name all of the resources that are required and explain step by step how to use the resources an the activity. Paste a...

-

There are two things that can make prices sticky. They are _________ and _________. A) Elmers glue and scotch tape B) rising input prices and output prices dropping C) menu costs and existing...

-

What is the role of business risk analysis in the audit planning process?

-

Unilever granted flexible work arrangements to 100,000 employees. Overall, the results have been positive. 1. Based on Unilever's Agile Working program, what else can human resource professionals do...

-

Discuss how globalization has changed jobs in an organization where you have worked. What are some HR responses to those changes?

-

This case provides information on the success of safety and health efforts in the workplace. (For the case, go to www.cengage.com/management/mathis or visit the instructor companion website.) 1....

-

Scores for the California Peace Officer Standards and Training test are normally distributed, with a mean of 50 and a standard deviation of 10. An agency will only hire applicants with scores in the...

-

1. Find the z-score that corresponds to a cumulative area of 0.3632. 2. Find the z-score that has 10.75% of the distributions area to its right.

-

Find the z-score that corresponds to each percentile. 1. P 5 2. P 50 3. P 90

Study smarter with the SolutionInn App