Question: This is a problem that has THREE questions. Therefore, please choose THREE answers (one choice for each question) to get full credit for this questions,

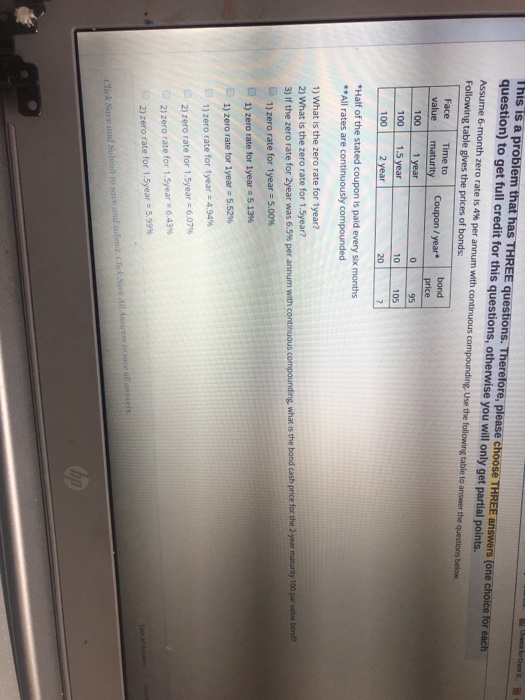

This is a problem that has THREE questions. Therefore, please choose THREE answers (one choice for each question) to get full credit for this questions, otherwise you will only get partial points. Assume 6-month zero rate is 4% per annum with continuous compounding. Use the following table to answer the questions below Following table gives the prices of bonds Face Time to bond value maturity Coupon / year* price 100 1 year 0 10 100 2 year 20 105 *Half of the stated coupon is paid every six months **All rates are continuously compounded 1) What is the zero rate for year? 2) What is the zero rate for 1.5year? 3) If the zero rate for 2year was 6.5% per annum with continuous compounding what is the bond cash price for the 2 year maturity 100 par value band 1) zero rate for 1 year = 5.00% 1) zero rate for lyear 5.13% 1) zero rate for lyear = 5.5296 1) zero rate for 1year = 4.94% 2) zero rate for 1.5year = 6,07% 2) zero rate for 1.5year 6.43% 2) zero rate for 1.5year = 5.999

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts