Question: This is all I have Problem4 You are analyzing yield spreads between corporate and government bonds. The following two corporate bonds X and Y are

This is all I have

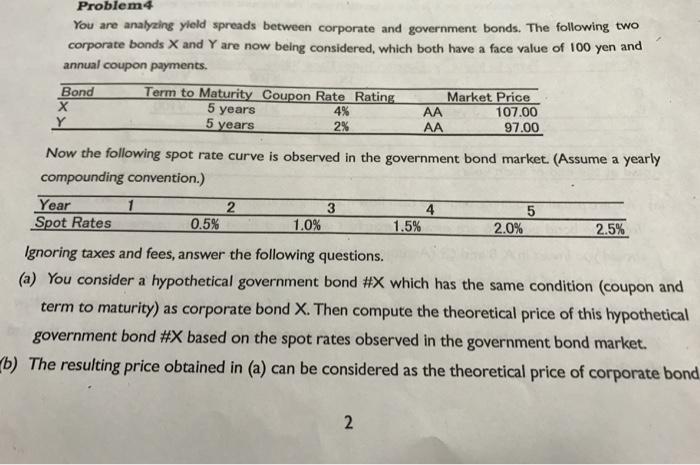

Problem4 You are analyzing yield spreads between corporate and government bonds. The following two corporate bonds X and Y are now being considered, which both have a face value of 100 yen and annual coupon payments. Bond Term to Maturity Coupon Rate Rating 5 years 5 vears 4% 2% 107.00 97.00 Now the following spot rate curve is observed in the government bond market. (Assume a yearly compounding convention.) Year Spot Rates 2 3 4 5 0.5% 1.0% 1.5% 2.0% 2.5% Ignoring taxes and fees, answer the following questions. (a) You consider a hypothetical government bond #x which has the same condition (coupon and term to maturity) as corporate bond X. Then compute the theoretical price of this hypothetical government bond #x based on the spot rates observed in the government bond market. (b) The resulting price obtained in (a) can be considered as the theoretical price of corporate bond

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts