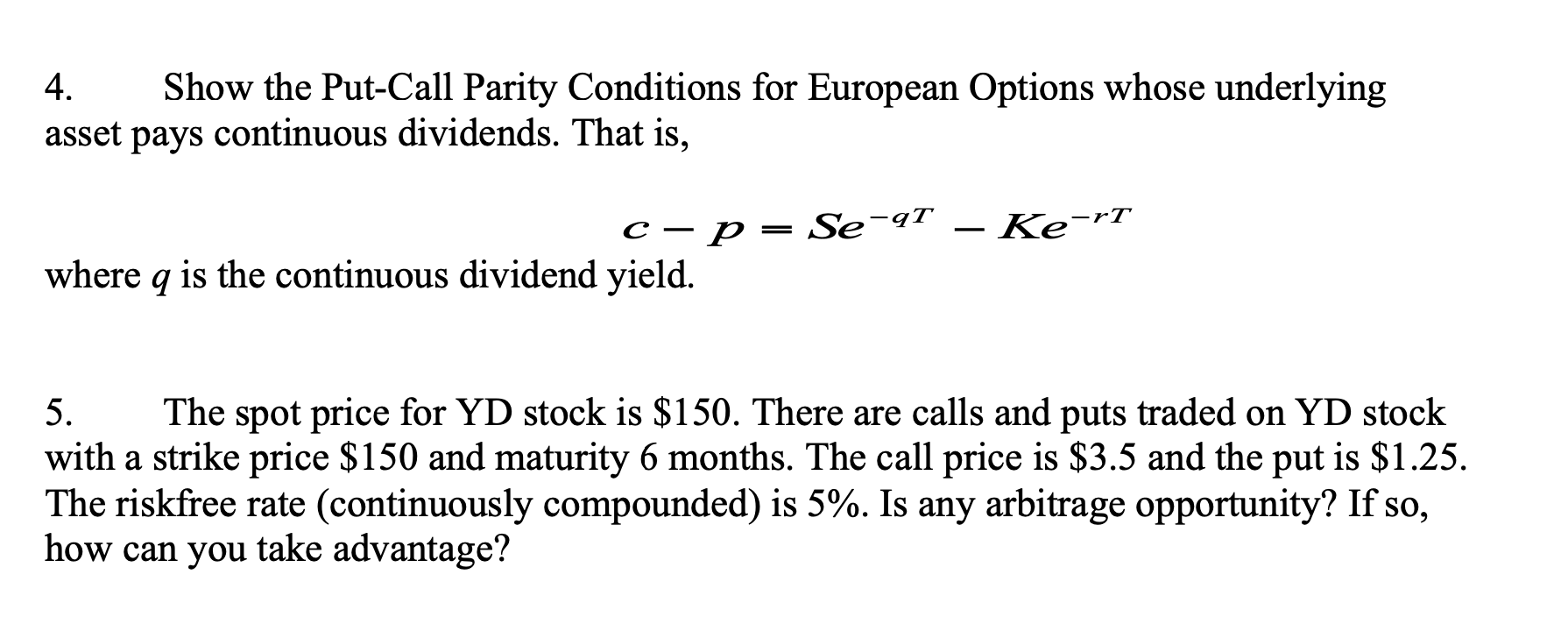

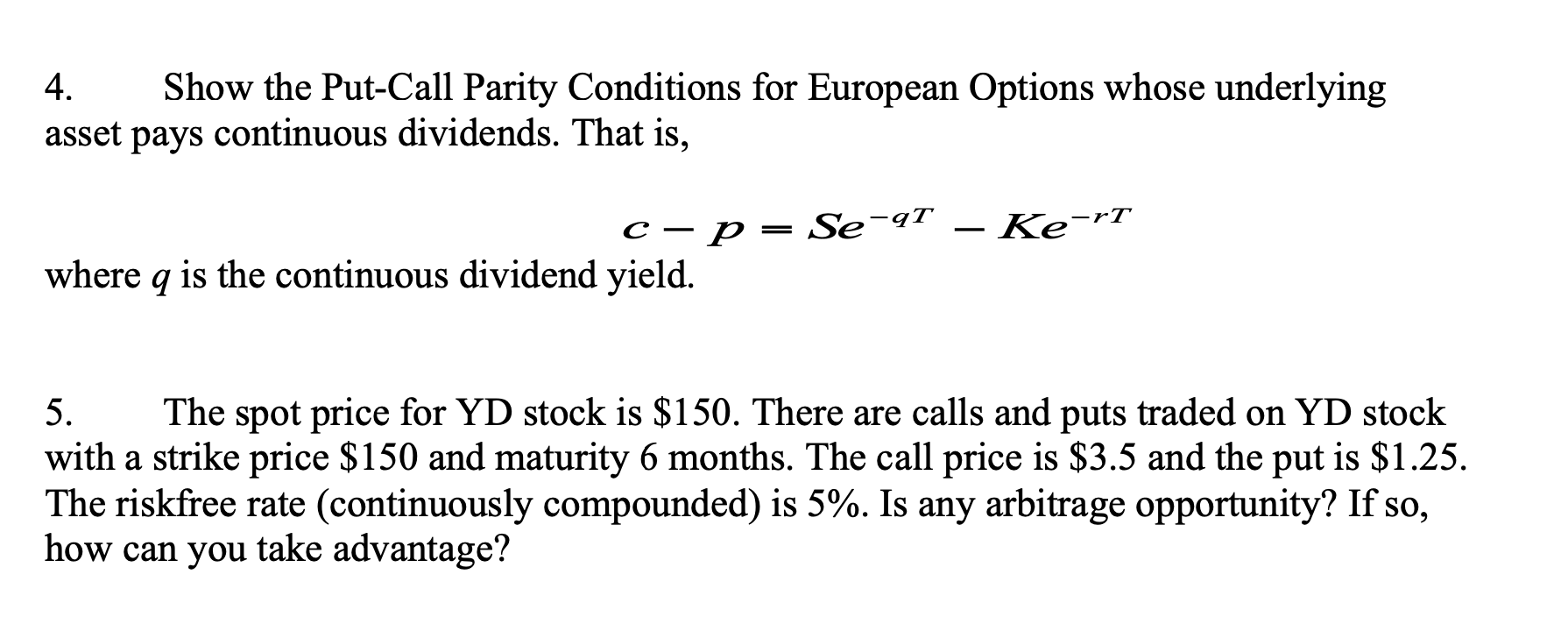

Question: This is all the information that I was given 4. Show the Put-Call Parity Conditions for European Options whose underlying asset pays continuous dividends. That

This is all the information that I was given

4. Show the Put-Call Parity Conditions for European Options whose underlying asset pays continuous dividends. That is, c p = Se'qT Ke'rT Where q is the continuous dividend yield. 5. The spot price for YD stock is $150. There are calls and puts traded on YD stock with a strike price $150 and maturity 6 months. The call price is $3.5 and the put is $1.25. The riskfree rate (continuously compounded) is 5%. Is any arbitrage opportunity? If so, how can you take advantage

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock