Question: This question has three parts, a,b and c. Please fill in the blanks and show work: Derive Spot Rates using the method of Bootstrapping-starting with

This question has three parts, a,b and c. Please fill in the blanks and show work:

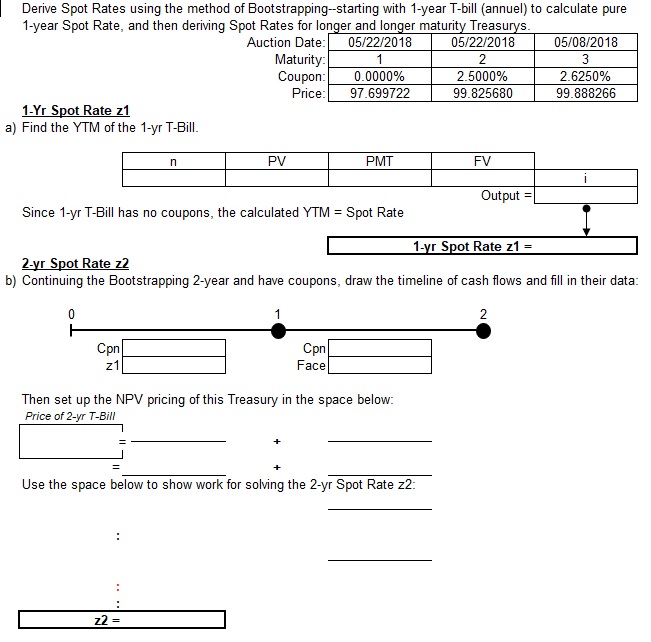

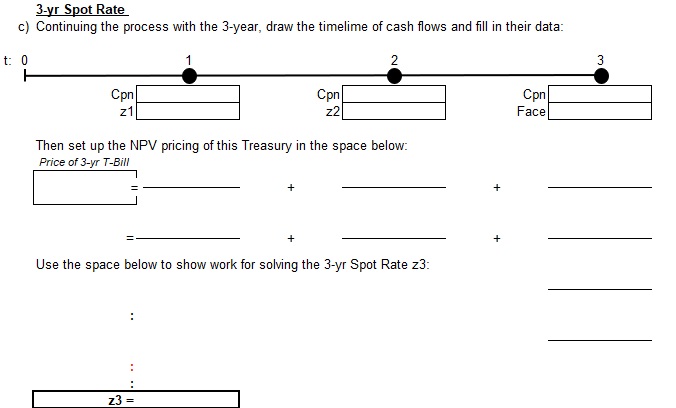

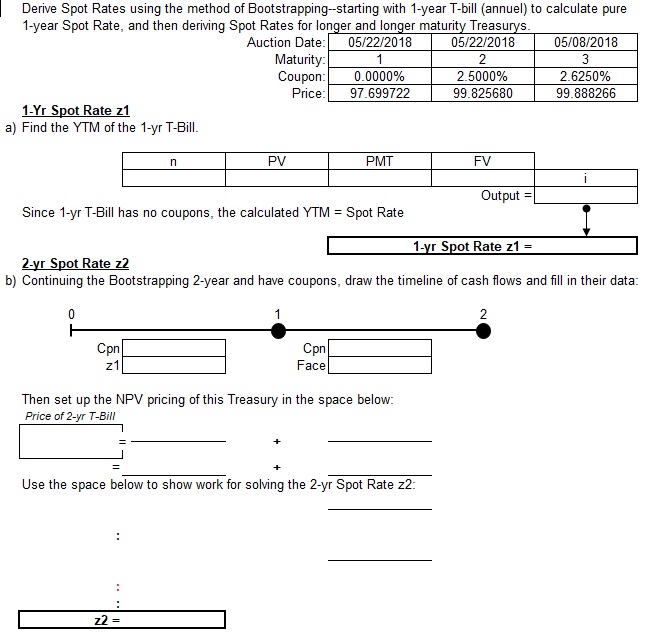

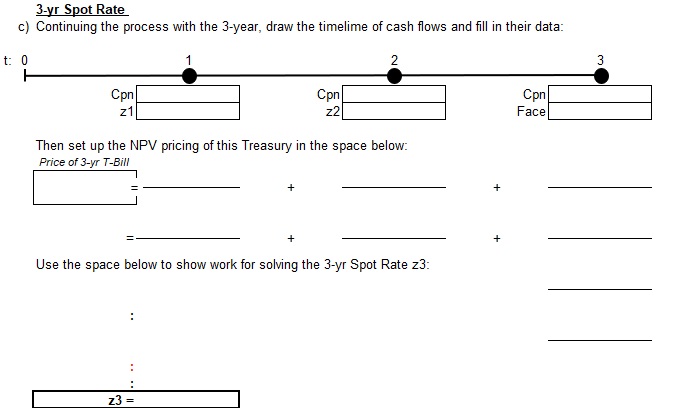

Derive Spot Rates using the method of Bootstrapping-starting with 1-year T-bill (annuel) to calculate pure 1-year Spot Rate, and then deriving Spot Rates for longer and longer maturity Treasurys Auction Date: 05/22/2018 05/22/2018 05/08/2018 Maturity: 2 3 Coupon: 0.0000% 2.5000% 2.6250% Price: 97.699722 99.825680 99.888266 1-Yr Spot Rate z1 a) Find the YTM of the 1-yr T-Bill. n PV PMT FV Output = Since 1-yr T-Bill has no coupons, the calculated YTM = Spot Rate 1-yr Spot Rate z1 = 2-yr Spot Rate z2 b) Continuing the Bootstrapping 2-year and have coupons, draw the timeline of cash flows and fill in their data: 0 Cpn Cpn z1 Face Then set up the NPV pricing of this Treasury in the space below: Price of 2-yr T-Bill Use the space below to show work for solving the 2-yr Spot Rate z2: . . 22 =3-yr Spot Rate c) Continuing the process with the 3-year, draw the timelime of cash flows and fill in their data: 0 Cpn Cpn Cpn z1 z2 Face Then set up the NPV pricing of this Treasury in the space below: Price of 3-yr T-Bill + + + + Use the space below to show work for solving the 3-yr Spot Rate z3: 73 =

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts