Question: Time Series Forecasting / Pfizer [9 points] We are interested in analyzing nd forecasting the Monthly Closing Price for Pfizer's Stock from January 1985-May 2022.

![Time Series Forecasting / Pfizer [9 points] We are interested in](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2024/09/66ee634b6b8bb_01866ee634ade9d9.jpg)

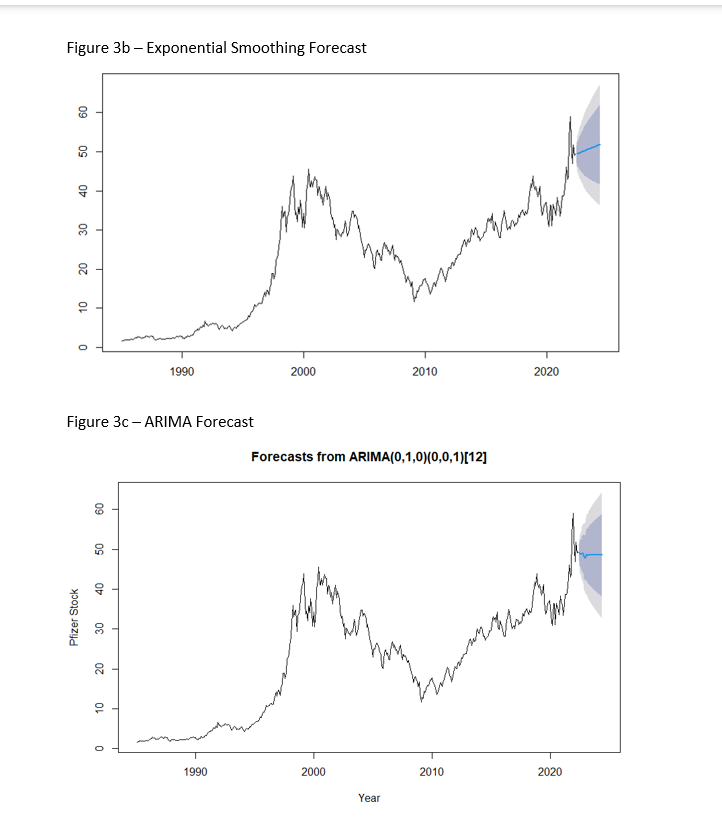

Time Series Forecasting / Pfizer [9 points] We are interested in analyzing nd forecasting the Monthly Closing Price for Pfizer's Stock from January 1985-May 2022. We ecide to implement Exponential Smoothing and ARIMA model(s). Please refer to Figures 3a3c elow. a. In time series models, we attempt to predict a given variable using only information contained in their past values. True or False? b. In Exponential Smoothing models, we expect recent observations to have less power in helping to forecast future values of a series. True or False? c. Refer to Figure 3b. What type of Exponential Smoothing model is this? d. An ARIMA model is slightly different than an ARMA. What is included in an ARIMA model that differentiates it from the ARMA process? e. Refer to Figure 3c. We can see that the non-seasonal portion is an ARIMA (0,1,0). Please describe what an ARIMA(0,1,0) represents (Use notation/equations if needed). f. Refer to Figure 3c. The (0,0,1) is the seasonal part of the model. True or False? g. Refer to Figure 3c. The [12] indicates this is a "12-month forecast." True or False? Figure 3b Exponential Smoothing Forecast Figure 3c-ARIMA Forecast Forecasts from ARIMA (0,1,0)(0,0,1)[12] Time Series Forecasting / Pfizer [9 points] We are interested in analyzing nd forecasting the Monthly Closing Price for Pfizer's Stock from January 1985-May 2022. We ecide to implement Exponential Smoothing and ARIMA model(s). Please refer to Figures 3a3c elow. a. In time series models, we attempt to predict a given variable using only information contained in their past values. True or False? b. In Exponential Smoothing models, we expect recent observations to have less power in helping to forecast future values of a series. True or False? c. Refer to Figure 3b. What type of Exponential Smoothing model is this? d. An ARIMA model is slightly different than an ARMA. What is included in an ARIMA model that differentiates it from the ARMA process? e. Refer to Figure 3c. We can see that the non-seasonal portion is an ARIMA (0,1,0). Please describe what an ARIMA(0,1,0) represents (Use notation/equations if needed). f. Refer to Figure 3c. The (0,0,1) is the seasonal part of the model. True or False? g. Refer to Figure 3c. The [12] indicates this is a "12-month forecast." True or False? Figure 3b Exponential Smoothing Forecast Figure 3c-ARIMA Forecast Forecasts from ARIMA (0,1,0)(0,0,1)[12]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts