Question: To get the answer for part A you can simply say: 1.40752(1/1.1) = 1.279. My question is how to get the 1.40725 ? Can you

To get the answer for part A you can simply say: 1.40752(1/1.1) = 1.279.

My question is how to get the 1.40725 ? Can you find it by using: 1/ (1+(y^m)/m) ?

Please show how to solve it and don't skip steps.

Thank you

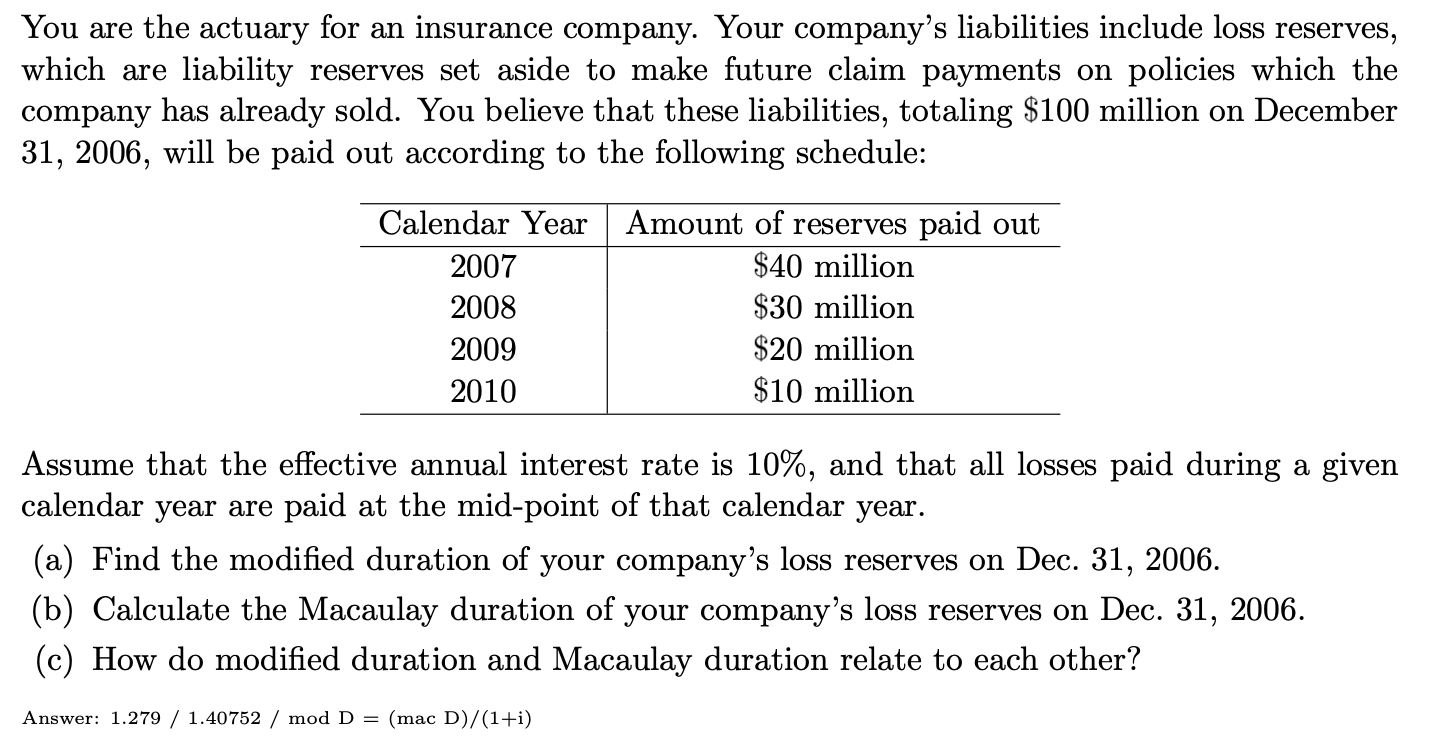

You are the actuary for an insurance company. Your company's liabilities include loss reserves, which are liability reserves set aside to make future claim payments on policies which the company has already sold. You believe that these liabilities, totaling $100 million on December 31, 2006, will be paid out according to the following schedule: Calendar Year Amount of reserves paid out 2007 $40 million 2008 $30 million 2009 $20 million 2010 $10 million Assume that the effective annual interest rate is 10%, and that all losses paid during a given calendar year are paid at the mid-point of that calendar year. (a) Find the modified duration of your company's loss reserves on Dec. 31, 2006. (b) Calculate the Macaulay duration of your company's loss reserves on Dec. 31, 2006. (c) How do modified duration and Macaulay duration relate to each other? Answer: 1.279 / 1.40752 / mod D = (mac D)/(1+i) You are the actuary for an insurance company. Your company's liabilities include loss reserves, which are liability reserves set aside to make future claim payments on policies which the company has already sold. You believe that these liabilities, totaling $100 million on December 31, 2006, will be paid out according to the following schedule: Calendar Year Amount of reserves paid out 2007 $40 million 2008 $30 million 2009 $20 million 2010 $10 million Assume that the effective annual interest rate is 10%, and that all losses paid during a given calendar year are paid at the mid-point of that calendar year. (a) Find the modified duration of your company's loss reserves on Dec. 31, 2006. (b) Calculate the Macaulay duration of your company's loss reserves on Dec. 31, 2006. (c) How do modified duration and Macaulay duration relate to each other? Answer: 1.279 / 1.40752 / mod D = (mac D)/(1+i)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts