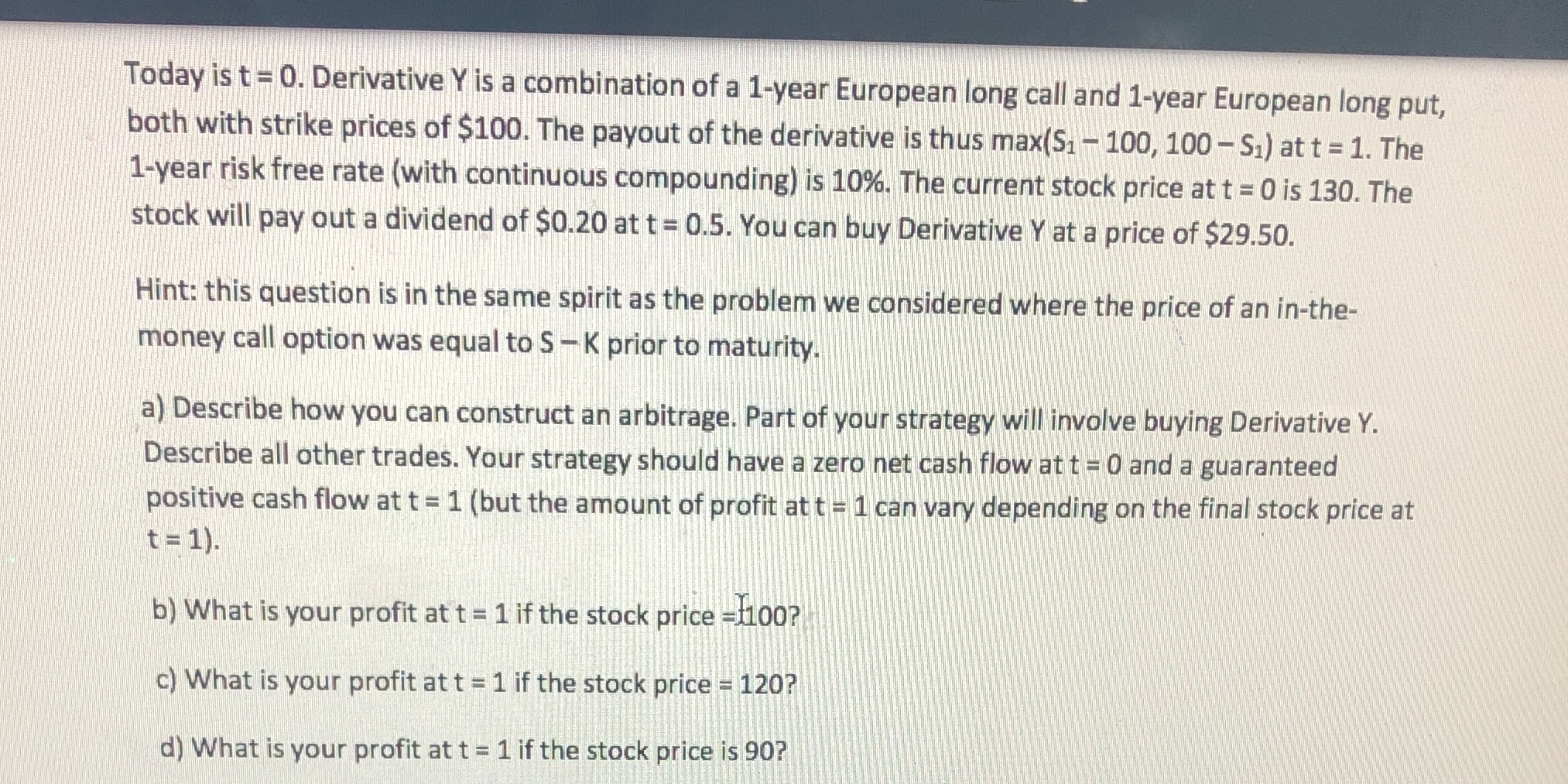

Today is t= 0. Derivative Y is a combination of a 1-year European long call and...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a To construct an arbitrage we need to ensure a zero net cash flow at time t0 and a guaranteed posit... View the full answer

Related Book For

Posted Date: