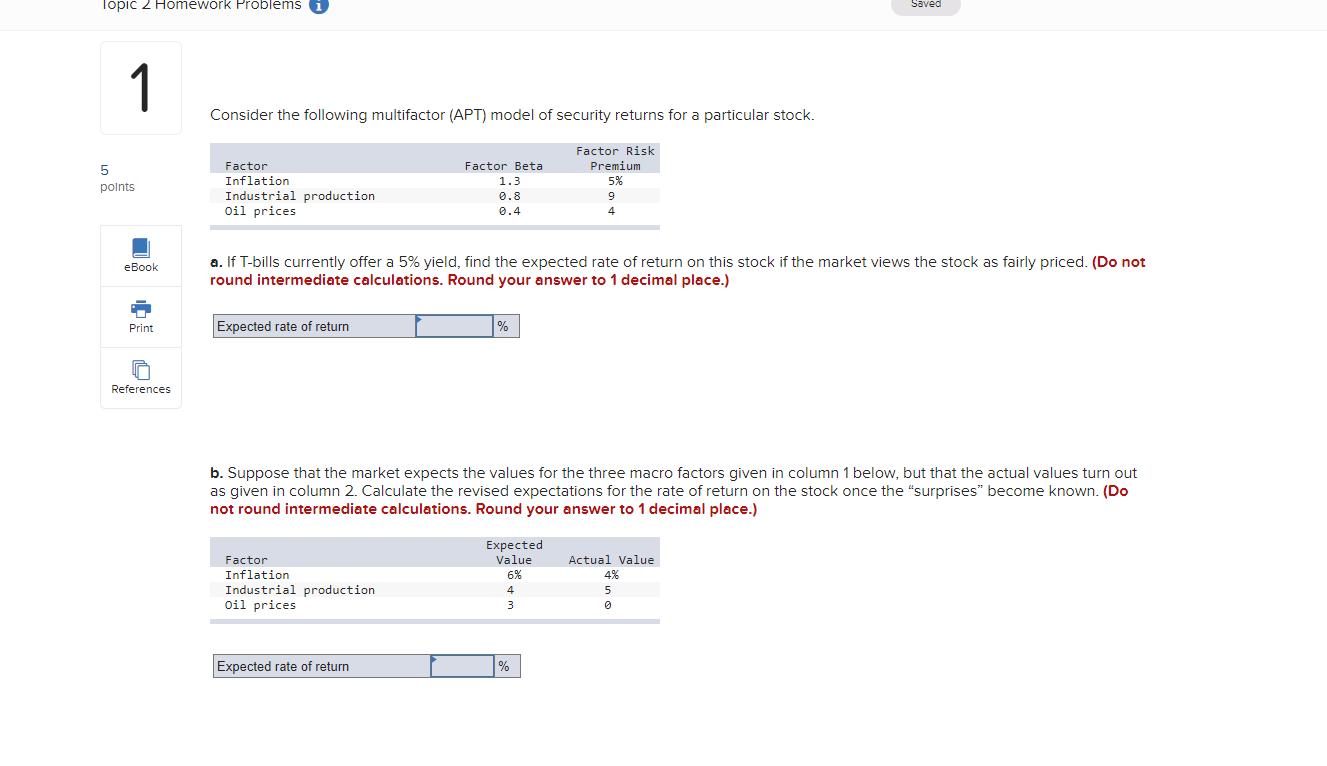

Question: Topic 2 Homework Problems Consider the following multifactor (APT) model of security returns for a particular stock. Factor Risk 5 Factor Factor Beta Premium points

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts