Question: (16 pts) Let 2 = {wi, W2, W3, wa} and T = 2 (time to maturity). Suppose that the risk-free asset has prices A(0) =

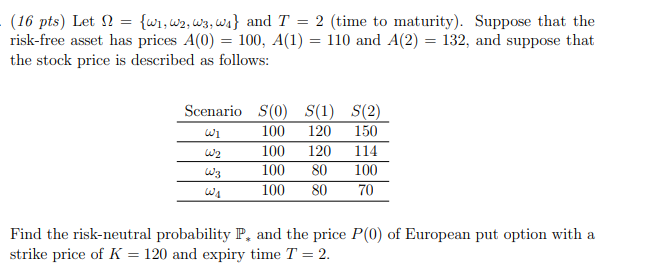

(16 pts) Let 2 = {wi, W2, W3, wa} and T = 2 (time to maturity). Suppose that the risk-free asset has prices A(0) = 100, A(1) = 110 and A(2) = 132, and suppose that the stock price is described as follows: Scenario S(0) S(1) Wi 100 120 W2 100 120 100 80 100 80 S(2) 150 114 100 70 Find the risk-neutral probability P, and the price PO of European put option with a strike price of K = 120 and expiry time T = 2. (16 pts) Let 2 = {wi, W2, W3, wa} and T = 2 (time to maturity). Suppose that the risk-free asset has prices A(0) = 100, A(1) = 110 and A(2) = 132, and suppose that the stock price is described as follows: Scenario S(0) S(1) Wi 100 120 W2 100 120 100 80 100 80 S(2) 150 114 100 70 Find the risk-neutral probability P, and the price PO of European put option with a strike price of K = 120 and expiry time T = 2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts