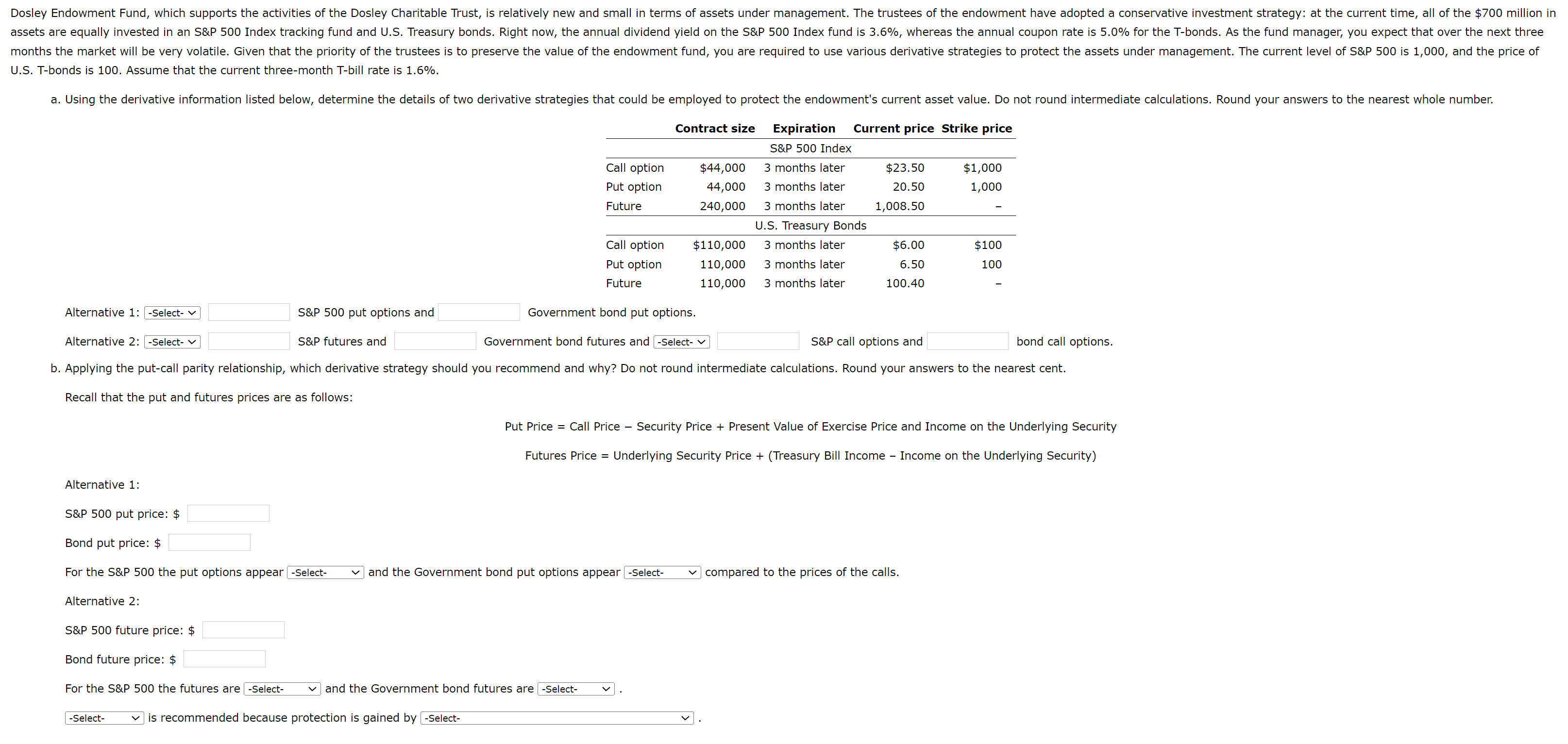

Question: U . S . T - bonds is 1 0 0 . Assume that the current three - month T - bill rate is 1

US Tbonds is Assume that the current threemonth Tbill rate is

Alternative : Select S&P put options and

Government bond put options.

Alternative : Select

S&P futures ar

Jovernment bond futures and Select

S&P call options and

bond call options.

b Applying the putcall parity relationship, which derivative strategy should you recommend and why? Do not round intermediate calculations. Round your answers to the nearest cent.

Recall that the put and futures prices are as follows:

Put Price Call Price Security Price Present Value of Exercise Price and Income on the Underlying Security

Futures Price Underlying Security Price Treasury Bill Income Income on the Underlying Security

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock