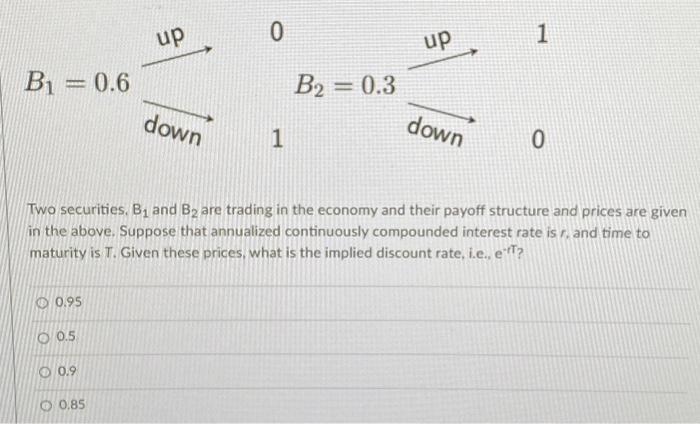

Question: up 0 1 up Bi = 0.6 B2 = 0.3 down down 1 0 Two securities, B1 and B2 are trading in the economy and

up 0 1 up Bi = 0.6 B2 = 0.3 down down 1 0 Two securities, B1 and B2 are trading in the economy and their payoff structure and prices are given in the above. Suppose that annualized continuously compounded interest rate is 1 and time to maturity is T. Given these prices, what is the implied discount rate, i.e., efT? O 0.95 O 0.5 O 0.9 0 0.85

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock