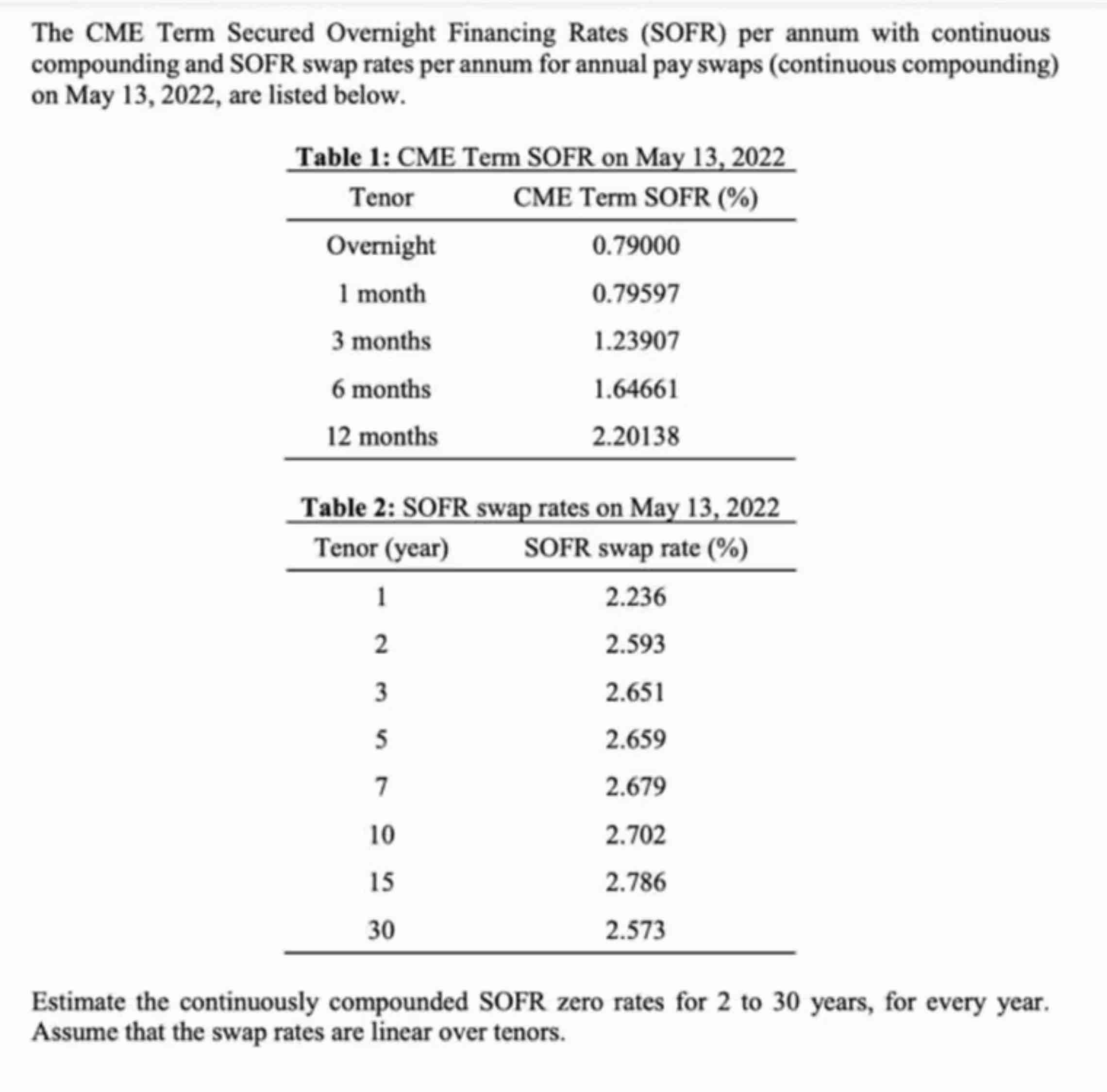

Question: Use excel to find answer The CME Term Secured Overnight Financing Rates ( SOFR ) per annum with continuous compounding and SOFR swap rates per

Use excel to find answer The CME Term Secured Overnight Financing Rates SOFR per annum with continuous compounding and SOFR swap rates per annum for annual pay swaps continuous compounding on May are listed below.

Estimate the continuously compounded SOFR zero rates for to years, for every year. Assume that the swap rates are linear over tenors.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock