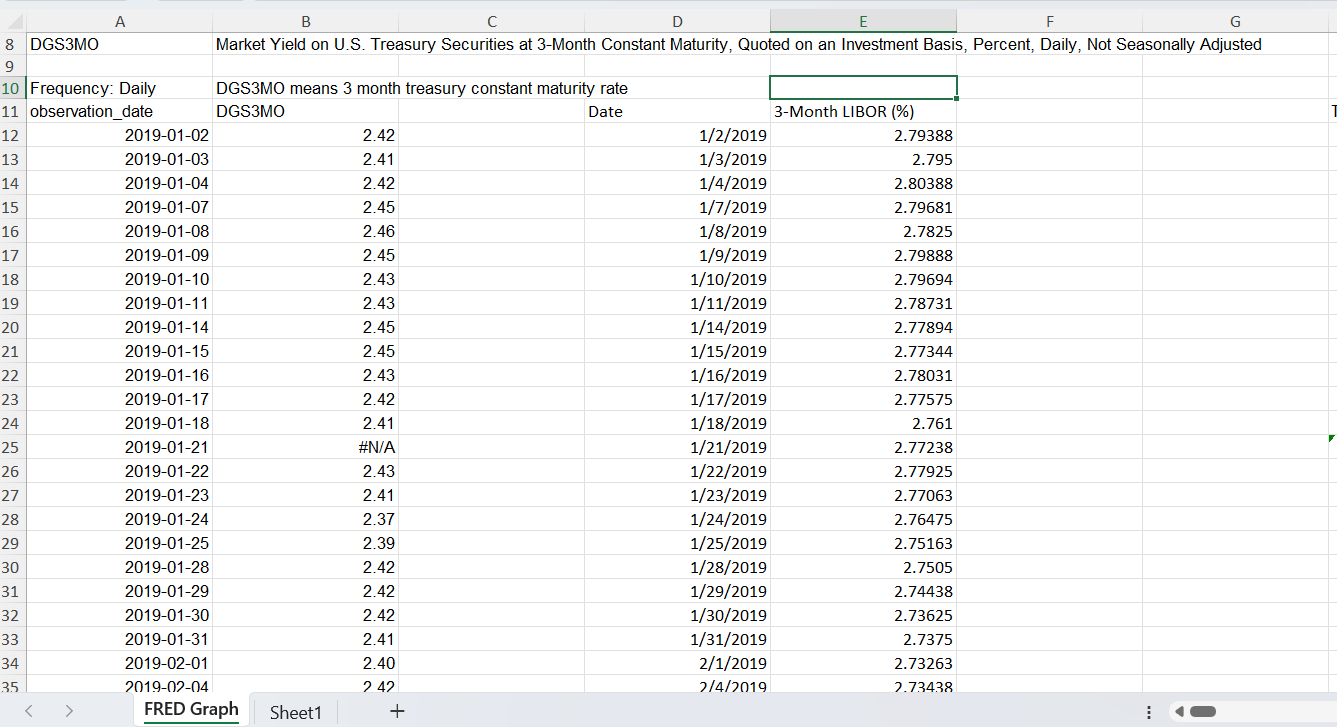

Use the 3-month LIBOR as attached: 3month_LIBOR.xlsx ( 3month_LIBOR.xlsx ). 2) Download daily 3-month Treasury Constant Maturity

No answer yet for this question.

Ask a Tutor

Question:

Use the 3-month LIBOR as attached: 3month_LIBOR.xlsx ( 3month_LIBOR.xlsx ).

2) Download daily "3-month Treasury Constant Maturity Rate" from Jan. 2, 2019, to Dec 29, 2023. (https://fred.stlouisfed.org/series/DGS3MO)

3) Compute the daily average rate of return and standard deviation with a 3-month T-bill rate over the sample period,

4) Plot the cumulative rate of return (X-axis: Date, Y-axis: Cumulative Return) from 3). Explain the plot thoroughly.

5) Calculate daily TED spreads over the sample period. (TED Spread = 3-month LIBOR - 3-month Treasury Constant Maturity Rate.)

6) Plot the TED spreads (X-axis: Date, Y-axis: TED Spread) over the sample period. Explain the plot by identifying periods of stress or relaxation in the financial markets.

Expert Answer:

Related Book For

Posted Date: