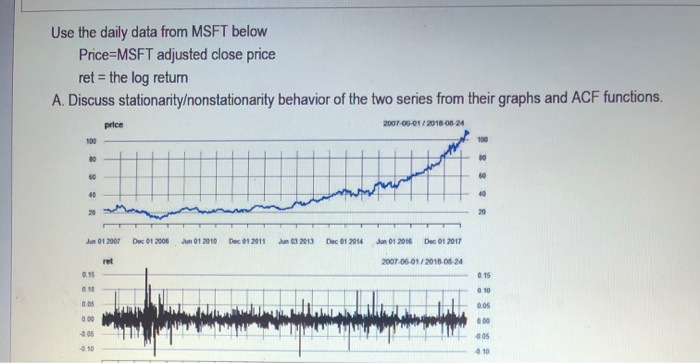

Question: Use the daily data from MSFT below Price=MSFT adjusted close price ret = the log return A. Discuss stationarityonstationarity behavior of the two series from

Use the daily data from MSFT below Price=MSFT adjusted close price ret = the log return A. Discuss stationarityonstationarity behavior of the two series from their graphs and ACF functions. price 2007-05-01 / 2018-01-24 100 100 60 4D 20 Jun 01 2007 Dec 01 2000 Jun 01 2010 Dec 01 2011 Jun 2013 Dec 01 2014 Jun 01 2016 Dec 01 2017 ret 2007-06-01/2018-01-24 0.15 0.15 0.10 0.10 0.08 0.05 0.00 0.05 6.10

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock