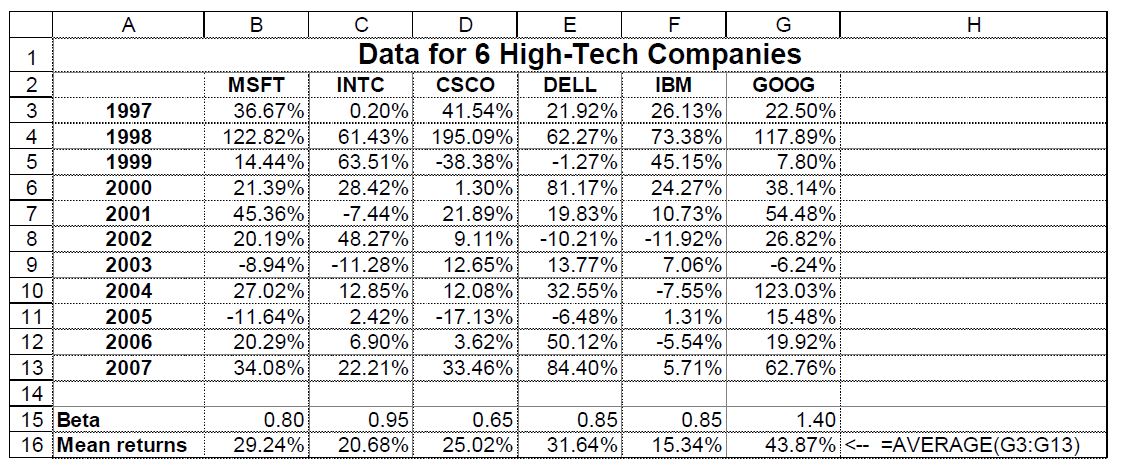

Question: Use the data below, calculate the variance - covariance matrix with the single-index model. You may assume that the variance of the S&P 500 index

Use the data below, calculate the variance - covariance matrix

with the single-index model. You may assume that the variance of the S&P 500

index (market portfolio) is 18%. In other words, the variances of each stock

remain the same as in question 21, but the covariances (outside the main diagonal)

are adjusted (multiplied) by the market index variance (a sort of a shrinkage

factor).

\f

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock