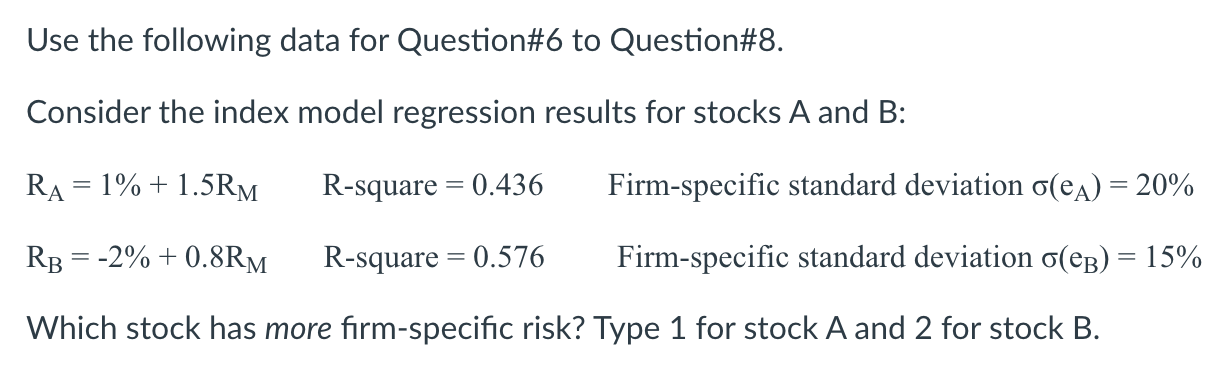

Question: Use the following data for Question#6 to Question#8. Consider the index model regression results for stocks A and B : RA=1%+1.5RMR-square =0.436 Firm-specific standard deviation

Use the following data for Question\#6 to Question\#8. Consider the index model regression results for stocks A and B : RA=1%+1.5RMR-square =0.436 Firm-specific standard deviation (eA)=20% RB=2%+0.8RMR-square =0.576 Firm-specific standard deviation (eB)=15% Which stock has more firm-specific risk? Type 1 for stock A and 2 for stock B

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock