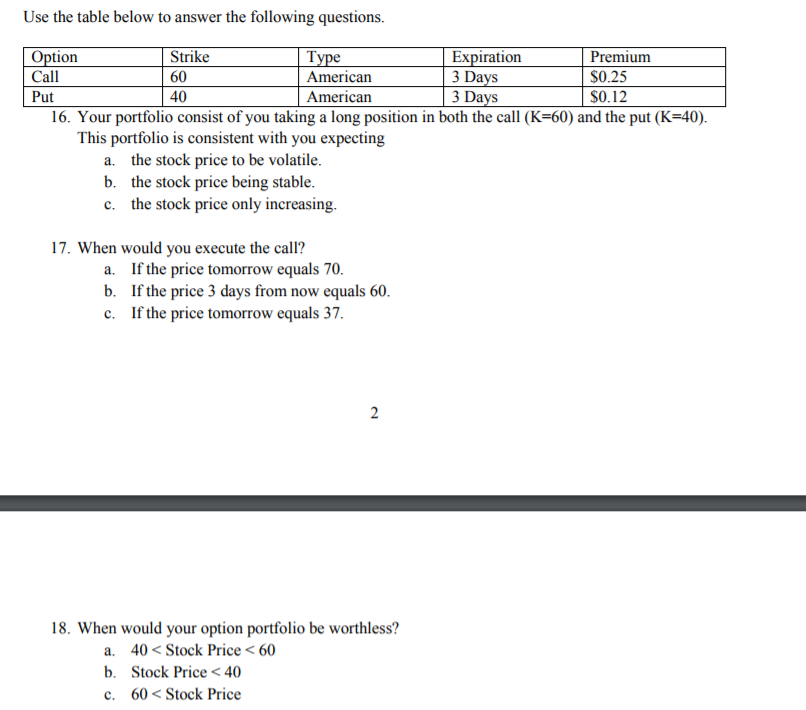

Question: Use the table below to answer the following questions. Option Call Put Strike 60 40 American American Expiration 3 Da 3 Da Premium S0.25 S0.12

Use the table below to answer the following questions. Option Call Put Strike 60 40 American American Expiration 3 Da 3 Da Premium S0.25 S0.12 16. Your portfolio consist of you taking a long position in both the call (K-60) and the put (K=40) This portfolio is consistent with you expecting a. b. c. the stock price to be volatile the stock price being stable the stock price only increasing 17. When would you execute the call? a. b. c. If the price tomorrow equals 70 If the price 3 days from now equals 60 If the price tomorrow equals 37. 18. When would your option portfolio be worthless? a. 40

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock