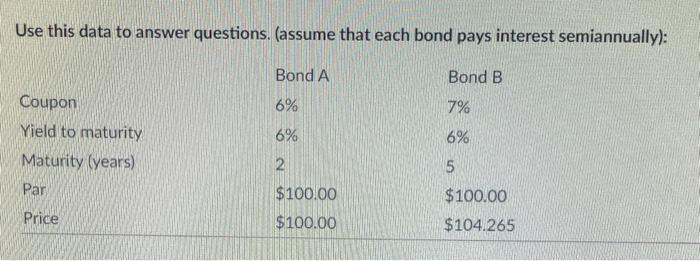

Question: Use this data to answer questions. (assume that each bond pays interest semiannually): Bond A Bond B 6% 7% 6% Coupon Yield to maturity Maturity

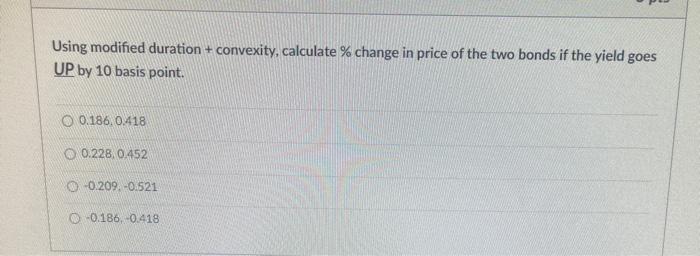

Use this data to answer questions. (assume that each bond pays interest semiannually): Bond A Bond B 6% 7% 6% Coupon Yield to maturity Maturity (years) Par 6% 2 $100.00 5 Price $100.00 $104.265 $100.00 Using modified duration + convexity, calculate % change in price of the two bonds if the yield goes UP by 10 basis point. O 0.186.0.418 O 0.228.0452 0 0.209.-0.521 -0.186,-0.418

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock