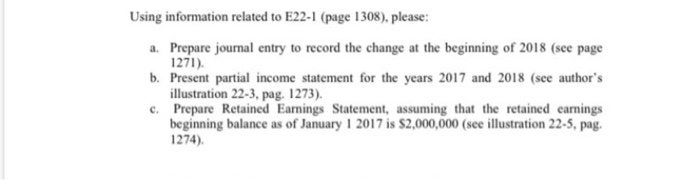

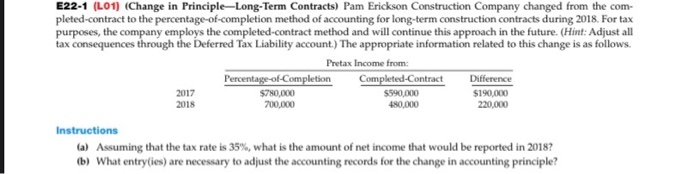

Question: Using information related to E22-1 (page 1308), please: a. Prepare journal entry to record the change at the beginning of 2018 (see page 1271). b.

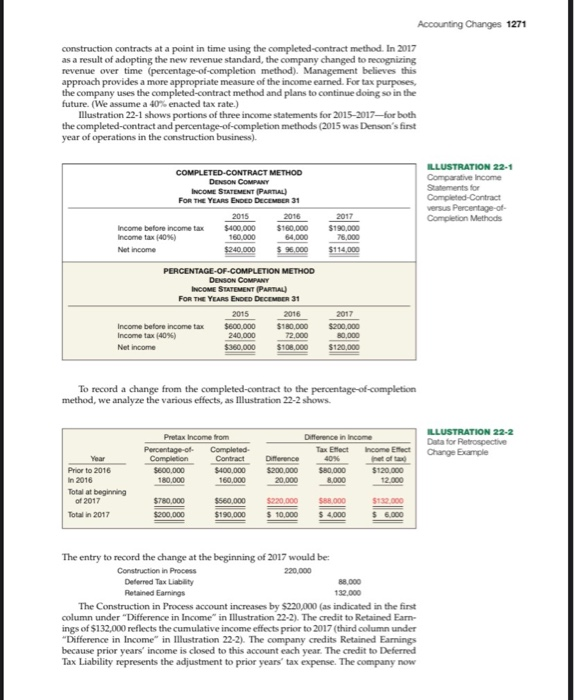

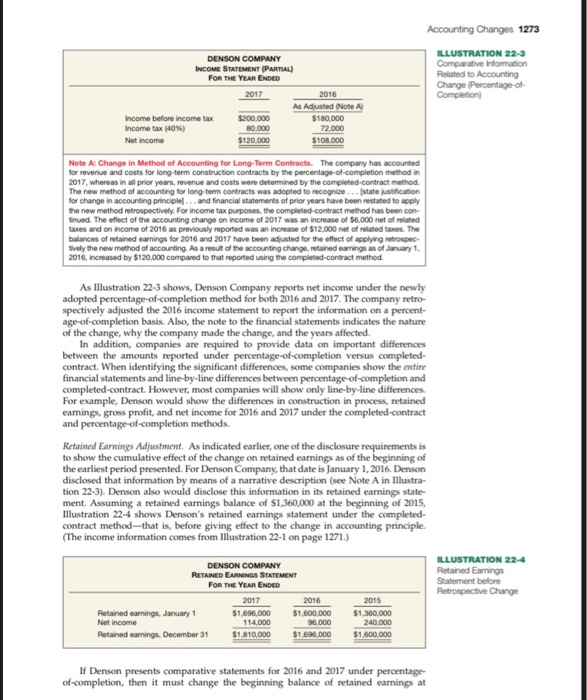

Using information related to E22-1 (page 1308), please: a. Prepare journal entry to record the change at the beginning of 2018 (see page 1271). b. Present partial income statement for the years 2017 and 2018 (see author's illustration 22-3, pag. 1273). c. Prepare Retained Earnings Statement, assuming that the retained earnings beginning balance as of January 1 2017 is $2,000,000 (see illustration 22-5. pag. 1274) E22-1 (L01) (Change in Principle-Long-Term Contracts) Pam Erickson Construction Company changed from the com- pleted-contract to the percentage-of-completion method of accounting for long-term construction contracts during 2018. For tax purposes, the company employs the completed-contract method and will continue this approach in the future. (Hint: Adjust all tax consequences through the Deferred Tax Liability account.) The appropriate information related to this change is as follows. Pretax Income from: Percentage-of-Completion Completed-Contract Difference 2017 $780,000 $590,000 $190,000 2018 700,000 480,000 220,000 Instructions (a) Assuming that the tax rate is 35%, what is the amount of net income that would be reported in 2018? (b) What entry (ies) are necessary to adjust the accounting records for the change in accounting principle? Accounting Changes 1271 construction contracts at a point in time using the completed-contract method. In 2017 as a result of adopting the new revenue standard, the company changed to recognizing revenue over time (percentage-of-completion method). Management believes this approach provides a more appropriate measure of the income earned. For tax purposes, the company uses the completed-contract method and plans to continue doing so in the future. (We assume a 40% enacted tax rate.) Illustration 22-1 shows portions of three income statements for 2015-2017-for both the completed-contract and percentage-of-completion methods (2015 was Denson's first year of operations in the construction business) COMPLETED-CONTRACT METHOD DENSON COMPANY INCOME STATEMENT PARTIAL) FOR THE YEARS ENDED DECEMBER 31 ILLUSTRATION 22-1 Comparative Income Satments for Completed-Contract versus Percentage-of- Completion Methods Income before income tax Income tax (40%) Net Income 2015 $400.000 160.000 $240.000 2016 $160,000 64.000 $ 96.000 2017 $190.000 28.000 $114,000 PERCENTAGE-OF-COMPLETION METHOD DENSON COMPANY INCOME STATEMENT PARTIAL FOR THE YEARS ENDED DECEMBER 31 2017 Income before income tax Income tax (40%) Net income 2015 $600.000 240.000 $360,000 2016 $180 000 72.000 $108,000 $200.000 80,000 $120.000 To record a change from the completed-contract to the percentage of completion method, we analyze the various effects, as Illustration 22-2 shows. Difference in income ILLUSTRATION 22-2 Data for Retrospective Change Example Pretax income from Percentage-of- Completed Completion Contract S600.000 $400.000 180.000 160.000 Tax Elect 40% Difference $200.000 Income Elect het ofta $120.000 0 000 Prior to 2016 In 2016 Total at beginning of 2017 Total in 2017 $780,000 $200.000 $560.000 $190.000 $ 10,000 The entry to record the change at the beginning of 2017 would be: Construction in Process 220.000 Deferred Tax Liability BRDO Retained Earnings 132.000 The Construction in Process account increases by $220,000 (as indicated in the first column under "Difference in Income" in Illustration 22-2). The credit to Retained Earn- ings of $132,000 reflects the cumulative income effects prior to 2017 (third column under "Difference in Income" in Illustration 22-2). The company credits Retained Earnings because prior years' income is closed to this account each year. The credit to Deferred Tax Liability represents the adjustment to prior years' tax expense. The company now Accounting Changes 1273 DENSON COMPANY INCOME STATEMENT PARTA) FOR THE YEAR ENDE ILLUSTRATION 22-3 Como veomation Related to Accounting Change Percentage of Completion 2017 2016 As Adjusted Not A $180.000 $200 000 income before income tax income tax 40%) Nutcome $120.000 Not A Change Method of Accounting for Long Term Contracts. The company has accounted for revenue and costs for long term construction contracts by the percentage of completion method in 2017, whereas in prior years, vence and costs were determined by the completed contact method The new method of accounting for long contracts was adopted to conce...stat i cation for change in accounting princ . and financial statements of prior years have been stated to apply the new method retrospectively. For income tax purposes, the completed contract method has been con sued. The effect of the accounting charge on income of 2017 was an increase of $6.000 net ofred and on Income of 2016 as previously reported was an increase of $12.000 net of related taxes. The balance of and earnings for 2016 and 2017 have been adjusted for the effect of applying to Wely the new method of accounting. As a result of the accounting changes and carings as of January 1 2016, increased by $120.000 compared to that reported using the completed contract method As Illustration 22-3 shows, Denson Company reports net income under the newly adopted percentage-of-completion method for both 2016 and 2017. The company retro spectively adjusted the 2016 income statement to report the information on a percent age-of-completion basis. Also, the note to the financial statements indicates the nature of the change, why the company made the change, and the years affected. In addition, companies are required to provide data on important differences between the amounts reported under percentage-of-completion versus completed contract. When identifying the significant differences, some companies show the entire financial statements and line-by-line differences between percentage-of-completion and completed-contract. However, most companies will show only line-by-line differences For example, Denson would show the differences in construction in process, retained eaming gross profit, and net income for 2016 and 2017 under the completed-contract and percentage-of-completion methods. Retained Earnings Adjustment. As indicated earlier, one of the disclosure requirements is to show the cumulative effect of the change on retained earnings as of the beginning of the earliest period presented. For Denson Company, that date is January 1, 2016. Denson disclosed that information by means of a narrative description (see Note A in Illustra- tion 22-3). Denson also would disclose this information in its retained earnings state ment. Assuming a retained earnings balance of $1,360,000 at the beginning of 2015, Illustration 22-4 shows Denson's retained earnings statement under the completed- contract method that is, before giving effect to the change in accounting principle (The income information comes from Illustration 22-1 on page 1271.) DENSON COMPANY RETAINED EARNINGS STATEMENT FOR THE YEAR ENDED S ILLUSTRATION 22-4 Retained Ewings ent before Retrospective Change 2017 $1.600.000 2016 $1500.000 Retained camings, January 1 Not income Retained caming, December 31 2015 $1.350.000 240.000 $1.600000 $1.810,000 If Denson presents comparative statements for 2016 and 2017 under percentage of-completion, then it must change the beginning balance of retained earnings at 1274 Chapter 22 Accounting Changes and Error Analysis January 1, 2016. The difference between the retained earnings balances under completed-contract and percentage of completion is computed as follows Retained earning January 1 2016 percentage of completion Retained earnings January 1, 2016 compte-contract Cumulative-effect herence $1.720 000 1.500 000 $120.000 The $120,000 difference is the cumulative effect. Illustration 22-5 shows a comparative retained earnings statement for 2016 and 2017, giving effect to the change in accounting principle to percentage-of-completion ILLUSTRATION 22-5 Pened Earnings Statement after Retrospective Application 2016 $1.500.000 DENSON COMPANY RETUNED EARNINGS SUTEMENT FOR THE YEAR ENDED 2017 Retained earnings January 1, as reported Add: Austment for the cumle ton prior years of the new method of accounting for construction contracts Retained caming. January 1, as adjusted $1.828.000 Net income 120.000 Retained earnings. December 31 $1. M8.000 120.000 1.720,000 108,000 $128.000 Denson adjusted the beginning balance of retained earnings on January 1, 2016, for the excess of percentage-of-completion net income over completed-contract net income in 2015. This comparative presentation indicates the type of adjustment that a company needs to make. It follows that this adjustment could be much larger if a number of prior periods were involved. Retrospective Accounting Change: Inventory Methods. As a second illustration of the retrospective approach, assume that Lancer Company has accounted for its inventory using the LIFO method. In 2017, the company changes to the FIFO method because management believes this approach provides a more appropriate reporting of its inventory costs. Illustration 22-6 provides additional information related to Lancer Company ILLUSTRATION 22-6 Lancer Company Information 1 Lancer Company started its operations on January 1, 2015. At that time stockholders invested $100.000 in the business in exchange for common stock 2. All sales, purchases, and operating expenses for the period 2015-2017 Cahansactions. Lancer's cash flows over this period are as follows $300.000 Purchase Operating expenses Cash flow Somerations 100 000 $110.000 000 110 000 100.000 $ 90.000 $300 000 125.000 100 000 $ 75.000 Dance Lancer has used the UFO method for financial reporting since its inception Inventory a nd under UFO and FIFO ore period 2015-2017 is as follows UFO Med FIFO Method January 1, 2015 December 31, 2015 12.000 December 31, 2016 25.000 December 31, 2017 39.000 Using information related to E22-1 (page 1308), please: a. Prepare journal entry to record the change at the beginning of 2018 (see page 1271). b. Present partial income statement for the years 2017 and 2018 (see author's illustration 22-3, pag. 1273). c. Prepare Retained Earnings Statement, assuming that the retained earnings beginning balance as of January 1 2017 is $2,000,000 (see illustration 22-5. pag. 1274) E22-1 (L01) (Change in Principle-Long-Term Contracts) Pam Erickson Construction Company changed from the com- pleted-contract to the percentage-of-completion method of accounting for long-term construction contracts during 2018. For tax purposes, the company employs the completed-contract method and will continue this approach in the future. (Hint: Adjust all tax consequences through the Deferred Tax Liability account.) The appropriate information related to this change is as follows. Pretax Income from: Percentage-of-Completion Completed-Contract Difference 2017 $780,000 $590,000 $190,000 2018 700,000 480,000 220,000 Instructions (a) Assuming that the tax rate is 35%, what is the amount of net income that would be reported in 2018? (b) What entry (ies) are necessary to adjust the accounting records for the change in accounting principle? Accounting Changes 1271 construction contracts at a point in time using the completed-contract method. In 2017 as a result of adopting the new revenue standard, the company changed to recognizing revenue over time (percentage-of-completion method). Management believes this approach provides a more appropriate measure of the income earned. For tax purposes, the company uses the completed-contract method and plans to continue doing so in the future. (We assume a 40% enacted tax rate.) Illustration 22-1 shows portions of three income statements for 2015-2017-for both the completed-contract and percentage-of-completion methods (2015 was Denson's first year of operations in the construction business) COMPLETED-CONTRACT METHOD DENSON COMPANY INCOME STATEMENT PARTIAL) FOR THE YEARS ENDED DECEMBER 31 ILLUSTRATION 22-1 Comparative Income Satments for Completed-Contract versus Percentage-of- Completion Methods Income before income tax Income tax (40%) Net Income 2015 $400.000 160.000 $240.000 2016 $160,000 64.000 $ 96.000 2017 $190.000 28.000 $114,000 PERCENTAGE-OF-COMPLETION METHOD DENSON COMPANY INCOME STATEMENT PARTIAL FOR THE YEARS ENDED DECEMBER 31 2017 Income before income tax Income tax (40%) Net income 2015 $600.000 240.000 $360,000 2016 $180 000 72.000 $108,000 $200.000 80,000 $120.000 To record a change from the completed-contract to the percentage of completion method, we analyze the various effects, as Illustration 22-2 shows. Difference in income ILLUSTRATION 22-2 Data for Retrospective Change Example Pretax income from Percentage-of- Completed Completion Contract S600.000 $400.000 180.000 160.000 Tax Elect 40% Difference $200.000 Income Elect het ofta $120.000 0 000 Prior to 2016 In 2016 Total at beginning of 2017 Total in 2017 $780,000 $200.000 $560.000 $190.000 $ 10,000 The entry to record the change at the beginning of 2017 would be: Construction in Process 220.000 Deferred Tax Liability BRDO Retained Earnings 132.000 The Construction in Process account increases by $220,000 (as indicated in the first column under "Difference in Income" in Illustration 22-2). The credit to Retained Earn- ings of $132,000 reflects the cumulative income effects prior to 2017 (third column under "Difference in Income" in Illustration 22-2). The company credits Retained Earnings because prior years' income is closed to this account each year. The credit to Deferred Tax Liability represents the adjustment to prior years' tax expense. The company now Accounting Changes 1273 DENSON COMPANY INCOME STATEMENT PARTA) FOR THE YEAR ENDE ILLUSTRATION 22-3 Como veomation Related to Accounting Change Percentage of Completion 2017 2016 As Adjusted Not A $180.000 $200 000 income before income tax income tax 40%) Nutcome $120.000 Not A Change Method of Accounting for Long Term Contracts. The company has accounted for revenue and costs for long term construction contracts by the percentage of completion method in 2017, whereas in prior years, vence and costs were determined by the completed contact method The new method of accounting for long contracts was adopted to conce...stat i cation for change in accounting princ . and financial statements of prior years have been stated to apply the new method retrospectively. For income tax purposes, the completed contract method has been con sued. The effect of the accounting charge on income of 2017 was an increase of $6.000 net ofred and on Income of 2016 as previously reported was an increase of $12.000 net of related taxes. The balance of and earnings for 2016 and 2017 have been adjusted for the effect of applying to Wely the new method of accounting. As a result of the accounting changes and carings as of January 1 2016, increased by $120.000 compared to that reported using the completed contract method As Illustration 22-3 shows, Denson Company reports net income under the newly adopted percentage-of-completion method for both 2016 and 2017. The company retro spectively adjusted the 2016 income statement to report the information on a percent age-of-completion basis. Also, the note to the financial statements indicates the nature of the change, why the company made the change, and the years affected. In addition, companies are required to provide data on important differences between the amounts reported under percentage-of-completion versus completed contract. When identifying the significant differences, some companies show the entire financial statements and line-by-line differences between percentage-of-completion and completed-contract. However, most companies will show only line-by-line differences For example, Denson would show the differences in construction in process, retained eaming gross profit, and net income for 2016 and 2017 under the completed-contract and percentage-of-completion methods. Retained Earnings Adjustment. As indicated earlier, one of the disclosure requirements is to show the cumulative effect of the change on retained earnings as of the beginning of the earliest period presented. For Denson Company, that date is January 1, 2016. Denson disclosed that information by means of a narrative description (see Note A in Illustra- tion 22-3). Denson also would disclose this information in its retained earnings state ment. Assuming a retained earnings balance of $1,360,000 at the beginning of 2015, Illustration 22-4 shows Denson's retained earnings statement under the completed- contract method that is, before giving effect to the change in accounting principle (The income information comes from Illustration 22-1 on page 1271.) DENSON COMPANY RETAINED EARNINGS STATEMENT FOR THE YEAR ENDED S ILLUSTRATION 22-4 Retained Ewings ent before Retrospective Change 2017 $1.600.000 2016 $1500.000 Retained camings, January 1 Not income Retained caming, December 31 2015 $1.350.000 240.000 $1.600000 $1.810,000 If Denson presents comparative statements for 2016 and 2017 under percentage of-completion, then it must change the beginning balance of retained earnings at 1274 Chapter 22 Accounting Changes and Error Analysis January 1, 2016. The difference between the retained earnings balances under completed-contract and percentage of completion is computed as follows Retained earning January 1 2016 percentage of completion Retained earnings January 1, 2016 compte-contract Cumulative-effect herence $1.720 000 1.500 000 $120.000 The $120,000 difference is the cumulative effect. Illustration 22-5 shows a comparative retained earnings statement for 2016 and 2017, giving effect to the change in accounting principle to percentage-of-completion ILLUSTRATION 22-5 Pened Earnings Statement after Retrospective Application 2016 $1.500.000 DENSON COMPANY RETUNED EARNINGS SUTEMENT FOR THE YEAR ENDED 2017 Retained earnings January 1, as reported Add: Austment for the cumle ton prior years of the new method of accounting for construction contracts Retained caming. January 1, as adjusted $1.828.000 Net income 120.000 Retained earnings. December 31 $1. M8.000 120.000 1.720,000 108,000 $128.000 Denson adjusted the beginning balance of retained earnings on January 1, 2016, for the excess of percentage-of-completion net income over completed-contract net income in 2015. This comparative presentation indicates the type of adjustment that a company needs to make. It follows that this adjustment could be much larger if a number of prior periods were involved. Retrospective Accounting Change: Inventory Methods. As a second illustration of the retrospective approach, assume that Lancer Company has accounted for its inventory using the LIFO method. In 2017, the company changes to the FIFO method because management believes this approach provides a more appropriate reporting of its inventory costs. Illustration 22-6 provides additional information related to Lancer Company ILLUSTRATION 22-6 Lancer Company Information 1 Lancer Company started its operations on January 1, 2015. At that time stockholders invested $100.000 in the business in exchange for common stock 2. All sales, purchases, and operating expenses for the period 2015-2017 Cahansactions. Lancer's cash flows over this period are as follows $300.000 Purchase Operating expenses Cash flow Somerations 100 000 $110.000 000 110 000 100.000 $ 90.000 $300 000 125.000 100 000 $ 75.000 Dance Lancer has used the UFO method for financial reporting since its inception Inventory a nd under UFO and FIFO ore period 2015-2017 is as follows UFO Med FIFO Method January 1, 2015 December 31, 2015 12.000 December 31, 2016 25.000 December 31, 2017 39.000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts