Question: Using part A, how would I complete part B? 9. Suppose you download the adjusted daily prices for ABC and estimate the annual variance to

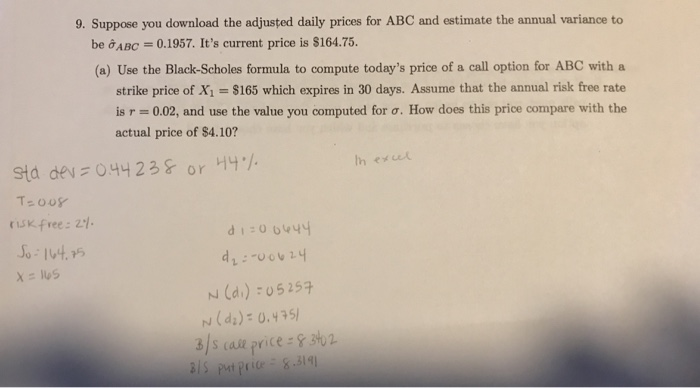

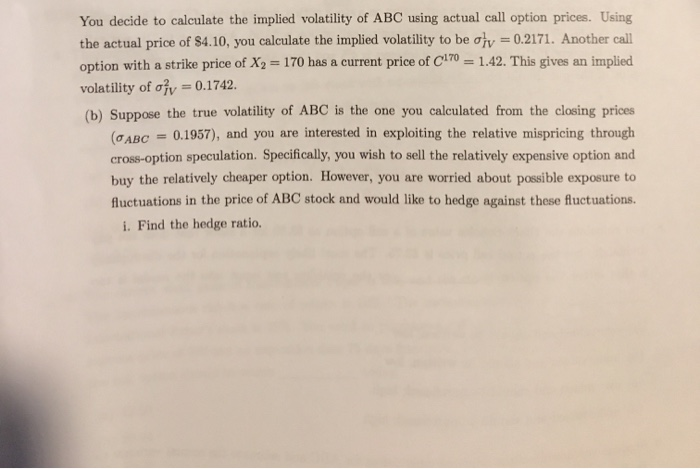

9. Suppose you download the adjusted daily prices for ABC and estimate the annual variance to be &ABC 0.1957. It's current price is $164.75. (a) Use the Black-Scholes formula to compute today's price of a call option for ABC with a strike price of X1 = $165 which expires in 30 days. Assume that the annual risk free rate is r 0.02, and use the value you computed for a. How does this price compare with the actual price of $4.10? Sta dev- 044 238 or T-0o SKfree: 21 So-104, 15 d N (di)- 05257 N(di)= 0.435 3/S (ase price -st2 3IS put Pric& 319 You decide to calculate the implied volatility of ABC using actual call option prices. Using the actual price of $4.10, you calculate the implied volatility to be aty 0.2171. Another call option with a strike price of X2 170 has a current price of C170 1.42. This gives an implied volatility of oy= 0.1742 (b) Suppose the true volatility of ABC is the one you calculated from the closing prices = 0.1957), and you are interested in exploiting the relative mispricing through (0ABC cross-option speculation. Specifically, you wish to sell the relatively expensive option and buy the relatively cheaper option. However, you are worried about possible exposure to fluctuations in the price of ABC stock and would like to hedge against these fluctuations. i. Find the hedge ratio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts