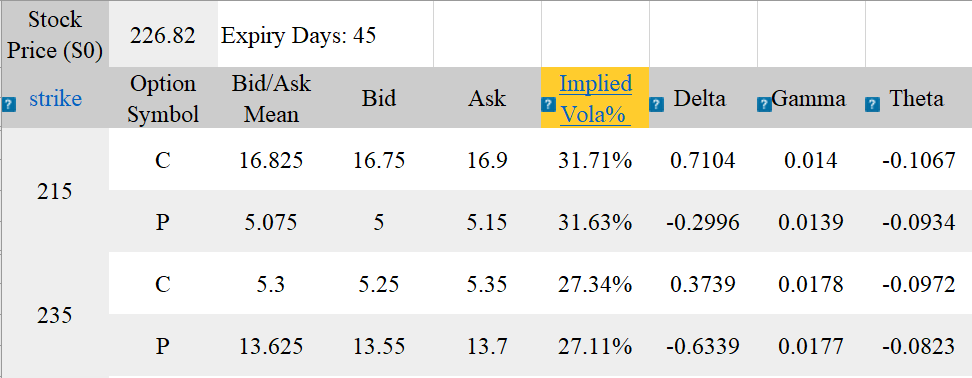

Question: Using the AAPL option chain, design a short strangle, where Xp = 215, and Xc = 235. If Stock price (S1)= 225 in two days,

Using the AAPL option chain, design a short strangle, where Xp = 215, and Xc = 235. If Stock price (S1)= 225 in two days, calculate the margin, 2-day profit (using delta, theta, and gamma), ROI for 2 days and annualized, maximum gain and maximum loss.

Stock Price (SO) 226.82 Expiry Days: 45 2 strike Option Symbol Bid/Ask Mean Bid Ask Implied Vola% Delta Gamma Theta 16.825 16.75 16.9 31.71% 0.7104 0.014 -0.1067 215 P 5.075 5 5.15 31.63% -0.2996 0.0139 -0.0934 5.3 5.25 5.35 27.34% 0.3739 0.0178 -0.0972 235 P 13.625 13.55 13.7 27.11% -0.6339 0.0177 -0.0823 Stock Price (SO) 226.82 Expiry Days: 45 2 strike Option Symbol Bid/Ask Mean Bid Ask Implied Vola% Delta Gamma Theta 16.825 16.75 16.9 31.71% 0.7104 0.014 -0.1067 215 P 5.075 5 5.15 31.63% -0.2996 0.0139 -0.0934 5.3 5.25 5.35 27.34% 0.3739 0.0178 -0.0972 235 P 13.625 13.55 13.7 27.11% -0.6339 0.0177 -0.0823

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts