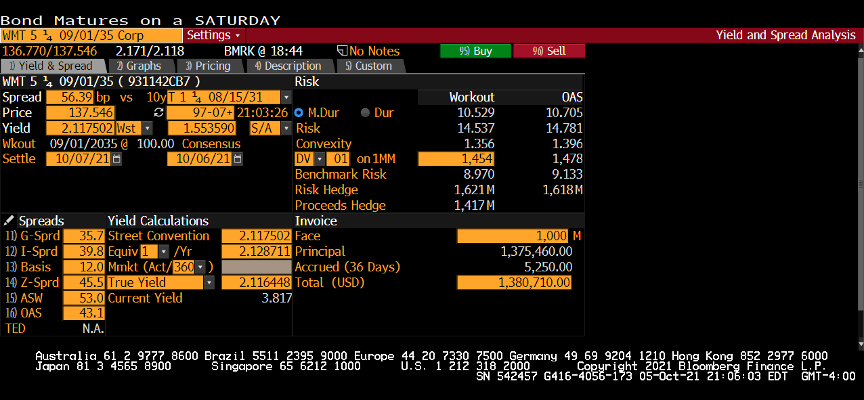

Question: Using the Bloomberg YAS screen below, answer the following questions. (1) Compute the Macaulay duration using the modified duration. (2) What is the DV01 of

Using the Bloomberg YAS screen below, answer the following questions.

(1) Compute the Macaulay duration using the modified duration.

(2) What is the DV01 of the bond for $1,000 par value?

(3) What is the approximate dollar price change for a 50-basis-point decrease in yields for $1,000 par value? You can use the modified duration only.

(4) What is the approximate percentage change in price for a 50-basis-point increase in yields for $1,000 par value? You can use the modified duration only.

Yield and Spread Analysis Yield and Spread Analysis

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock