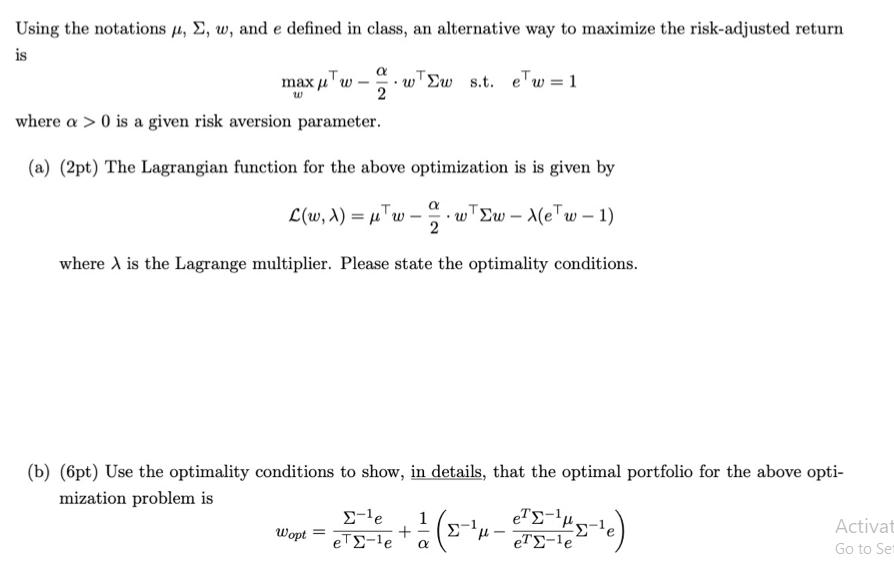

Question: Using the notations , , w, and e defined in class, an alternative way to maximize the risk-adjusted return is a max w- wEw

Using the notations , , w, and e defined in class, an alternative way to maximize the risk-adjusted return is a max w- wEw s.t. ew=1 W where a > 0 is a given risk aversion parameter. (a) (2pt) The Lagrangian function for the above optimization is is given by L(w, x) = w-27 ww - X(ew -1) where X is the Lagrange multiplier. Please state the optimality conditions. (b) (6pt) Use the optimality conditions to show, in details, that the optimal portfolio for the above opti- mization problem is -1 eTe Wopt -e 1 + eT-le eT-le Activat Go to Set

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock