Question: Using the options data from the spreadsheet FNCE4408_Assignment-02.xlsx, form a COVERED CALL strategy with the stock and the Jan 110 CALL option. At maturity, determine:

- Using the options data from the spreadsheet FNCE4408_Assignment-02.xlsx, form a COVERED CALL strategy with the stock and the Jan 110 CALL option. At maturity, determine:

(Answers should be to two decimal places, NO dollar sign. You may Answer with INFINITY if appropriate)

i) The maximum Profit is?

ii) The maximum Loss is?

iii) The break-even stock price is?

2. The OCC margin requirements for uncovered short calls and puts is: 100% of the market value of the premium plus: 20% of the market value of the underlying stock minus: the amount the option is out-of-the-money. However, the margin must be at least the option market value plus either 10% of the value of the stock for a call option or 10% of the exercise price for a put option.

Stock ABY is currently trading at $50 per share. What is the margin requirement for a short position in a put option which has a strike price of $45 and a premium of $4.00?

a)1400

b)900

c)850

d)500

e)none of the above

3. Using the options data from the spreadsheet FNCE4408_Assignment-02.xlsx, what is the intrinsic value of the December 115 put?

a)1.75

b)0.00

c)3.90

d)3.00

4. Suppose you use put-call parity to compute a European call price from the European put price, the stock price, and the risk-free rate. You find the market price of the call to be less than the price given by put-call parity. Ignoring transaction costs, what trades should you do?

a)buy the put and the stock and sell the risk-free bonds and the call

b)buy the call and the risk-free bonds and sell the put and the stock

c)none of the above

5. Using the options data from the spreadsheet FNCE4408_Assignment-02.xlsx, what is the European lower bound of the December 105 call?

a) 0.00

b) 15.58

c) 8.25

d) 9.26

e) none of the above

6. Using the options data from the spreadsheet FNCE4408_Assignment-02.xlsx, what is the intrinsic value of the January 110 call?

a) 0.00

b) 8.30

c) 3.75

d)5.00

e)none of the above

7. A stock is currently $45 and the risk free rate is 5.75% per annum. A six-month European call option on this stock with a strike price of $42.50 has a price of $6.00. What is the price of a European put option on this stock with the same exercise price and maturity? (Hint: use the put call parity)

a) 2.33

b) 3.50

c) none of the above

8. Question 8 options:

Use either "up" or "down" "neither"(without the quotes for your answers) If the risk-free rate increases, then the price of a call option will go ____ and if volatility increases, the price of a put option will go ____.

9. Using the options data from the spreadsheet FNCE4408_Assignment-02.xlsx, what is the time value of the December 105 call?

a) 1.05

b) 2.80

c) 1.75

d) 0.00

e) none fo the above

10. Using the options data from the spreadsheet FNCE4408_Assignment-02.xlsx, what is the time premium of the November 110 put?

a) 3.25

b) 2.35

c) 1.50

d) 0.90

e) none fo the above

11. Using the options data from the spreadsheet FNCE4408_Assignment-02.xlsx, do the Nov 105 CALL and PUT options represent an arbitrage opportunity? ____ (Answer YES or NO. Hint use the put-call parity)

If so, the arbitrage strategy would be to :

i) ____ the call option (answer BUY or SELL)

ii) (Answer INVEST or BORROW) ____ the PV(X), which amounts to ____ (Answer should be to 2 decimal places and no dollar sign)

iii) (Answer BUY or SELL) ____ the PUT option, and ____ the STOCK (Answer BUY or SHORT).

FNCE4408_Assignment-02 Spreadsheet:

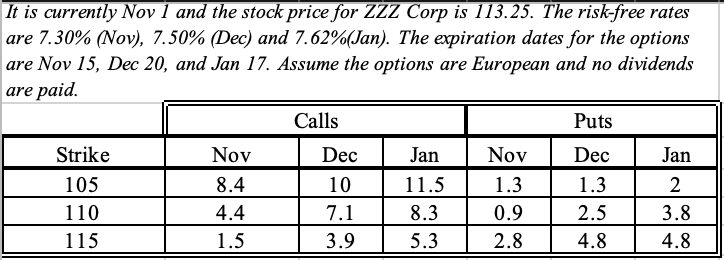

It is currently Nov 1 and the stock price for ZZZ Corp is 113.25. The risk-free rates are 7.30% (Nov), 7.50% (Dec) and 7.62%(Jan). The expiration dates for the options are Nov 15, Dec 20, and Jan 17. Assume the options are European and no dividends are paid

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts