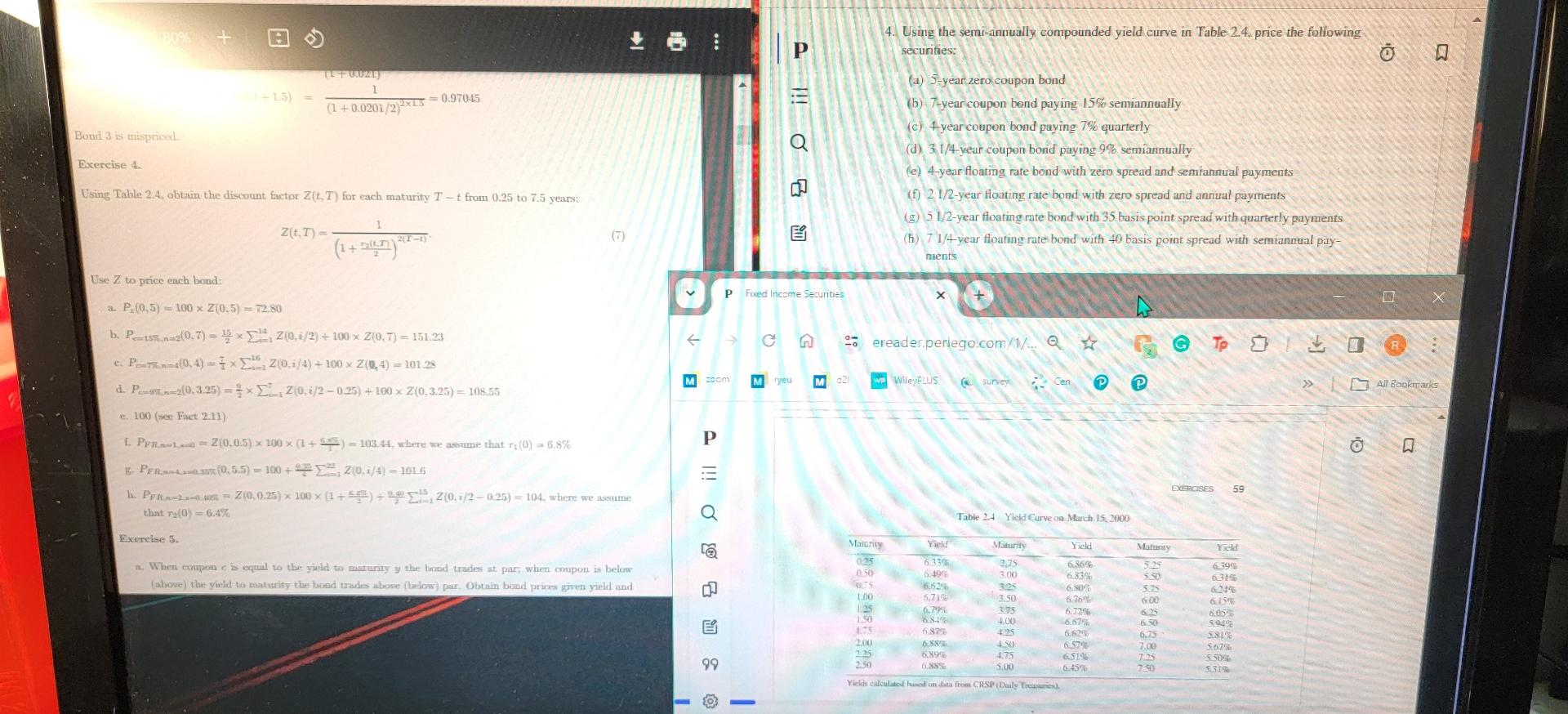

Question: Using the semi - innually compounded yield curve in Table 2 . 4 , price the following securities: ( a ) 5 - year zero

Using the semiinnually compounded yield curve in Table price the following securities:

ayear zero coupon bond

byear coupon bend paying semiannually

c year coupon bond paying quarterly

d year coupon bond paying semiannually

eyear floating rate bond with zero spread and semiannual payments

fyear floating rate bond with zero spread and annual payments

Using Table obtain the discount factor for each maturity from to years;

gyear floating rate bond with basis point spread with quarterly payments

hyear floating rate bond wath basis point spread with semiannual pay

Use to price each bond:

a

b

ctin

d

csec Fact that

Exereise

a When conpon of is equil to the yield to maturity the thod trades at par, when coupon is below

P

Q

mentslease provide detailed Solutions using Excel I have provided the table and the solution manual for reference

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock