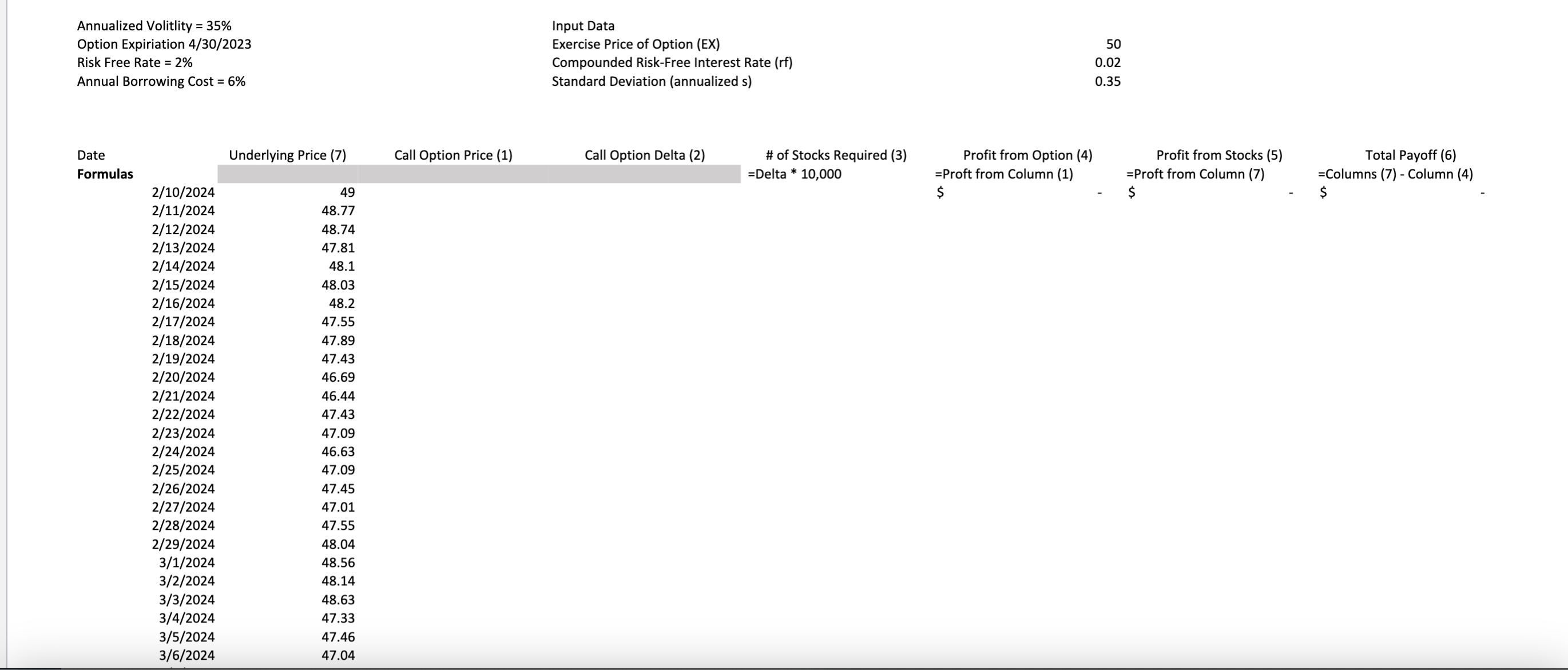

Question: Using the spreadsheet provided, simulate a portfolio with delta hedging. Assume you have sold 1 0 0 European call options ( each of which is

Using the spreadsheet provided, simulate a portfolio with delta hedging. Assume you have sold European call options each of which is worth shares, for a total of shares exposure short on the stock of Lumberjack Farms. Information about option is given below. Annualized Volitlity

Option Expiriation

Risk Free Rate

Annual Borrowing Cost

Strike Price

Number of Shares

Your ability to compute delta.

Your ability to compute the total number of shares purchasedsold each day.

Your graph showing the profit and loss from the option portfolio, and the stock portfolio.

The calculation of the total payoff.No transaction costs and days in a year for interest and purposes

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock