Question: Using the weekly closing stock price (S;) data in the table below, find the stock price volatility per annum in decimal format (not in %).

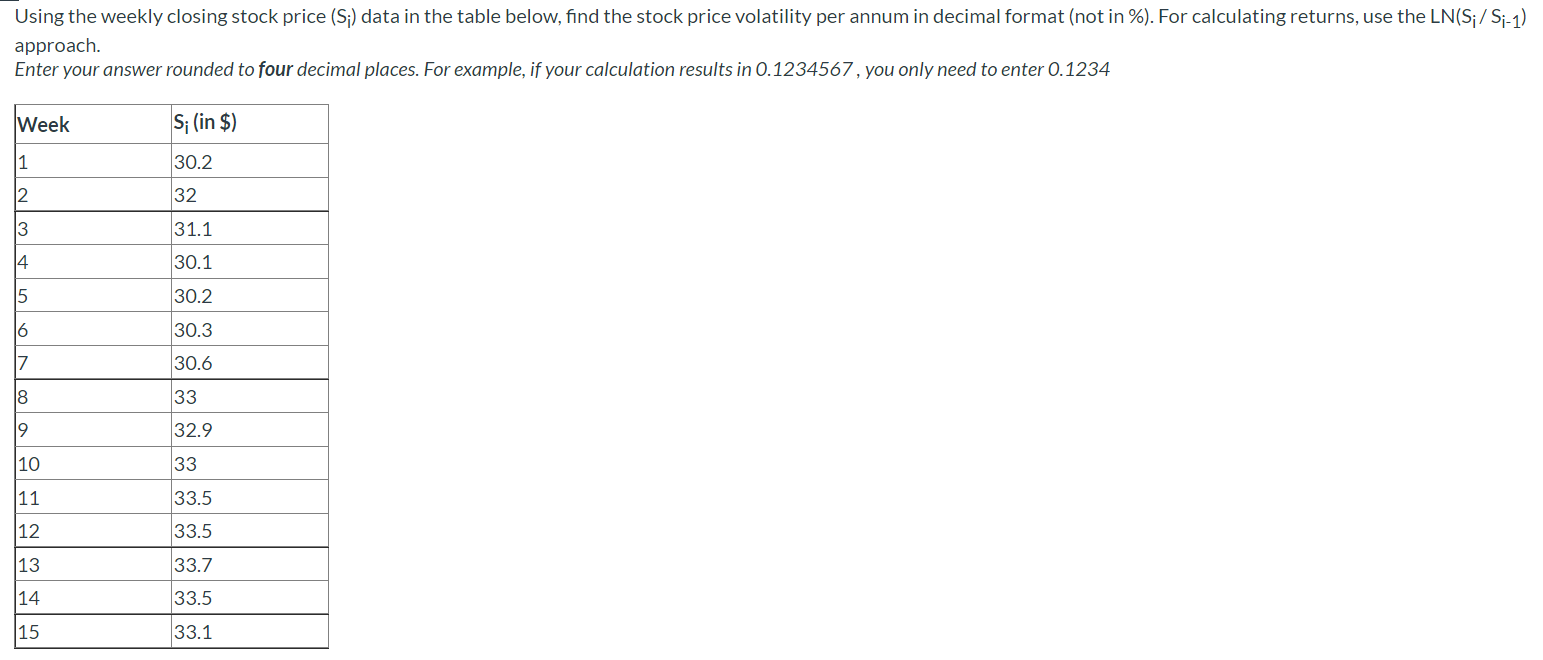

Using the weekly closing stock price (S;) data in the table below, find the stock price volatility per annum in decimal format (not in %). For calculating returns, use the LN(S;/ Si-1) approach. Enter your answer rounded to four decimal places. For example, if your calculation results in 0.1234567 , you only need to enter 0.1234 Week S; (in $) 1 30.2 2 32 3 31.1 4 30.1 5 30.2 30.3 30.6 33 32.9 10 33 ON 00 a FEB 2 11 33.5 12 33.5 33.7 14 33.5 33.1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock