Question: Variable Production Cost Variance Analysis and Performance Evaluation. Deerfield Plastics, Inc., produces plastic snow shovels. Variable overhead is applied to products based on machine hours.

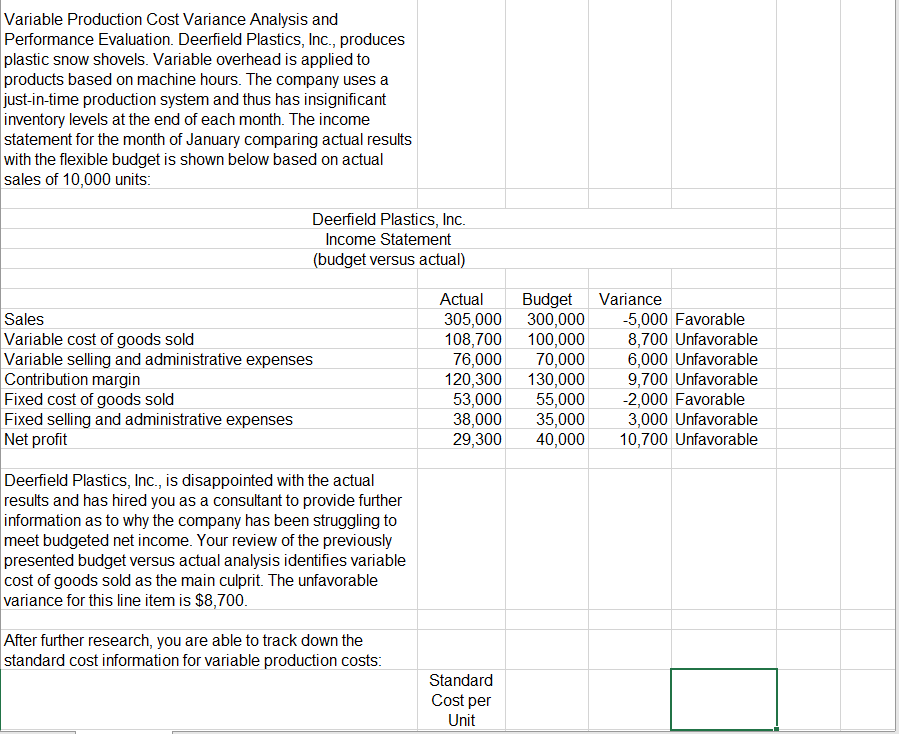

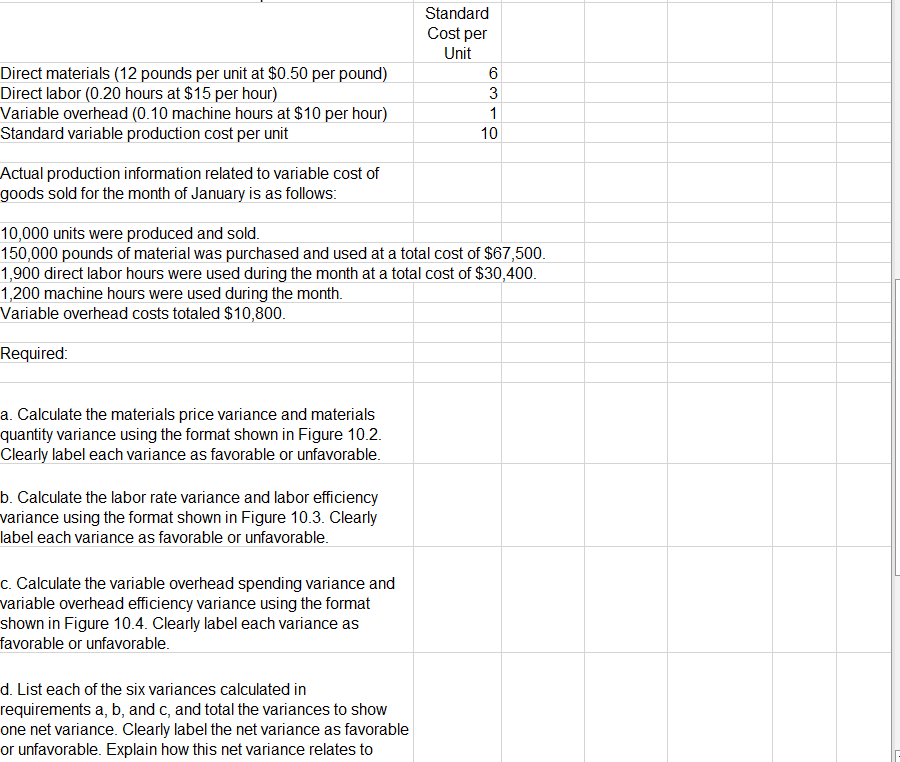

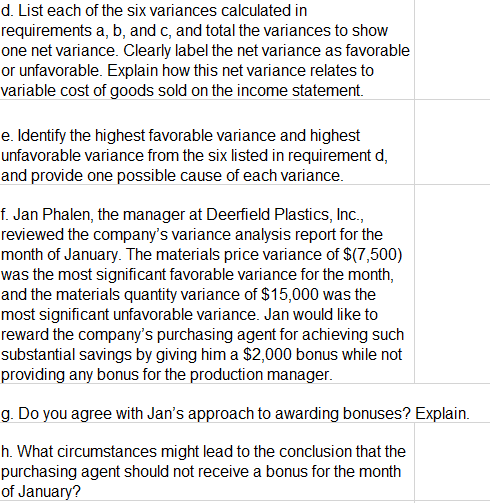

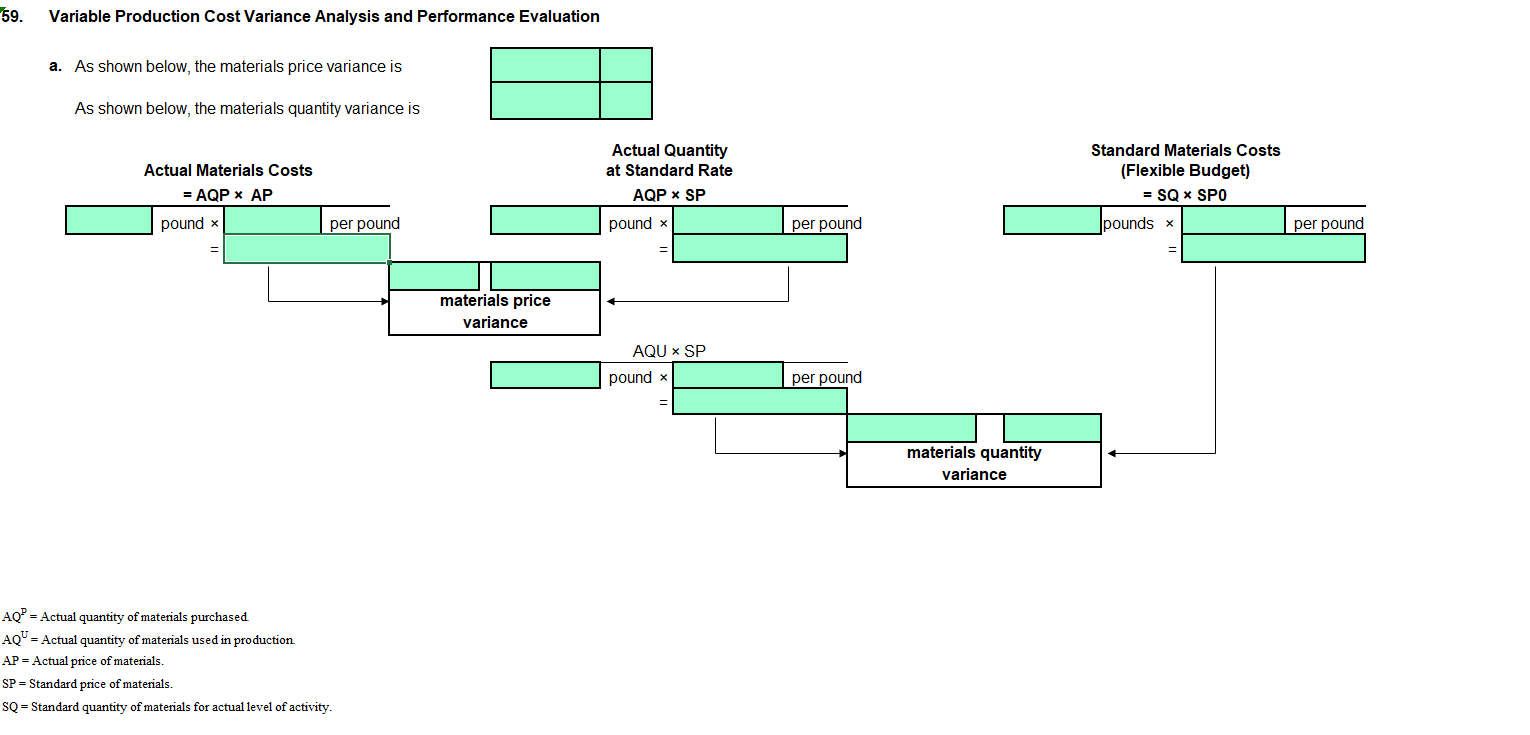

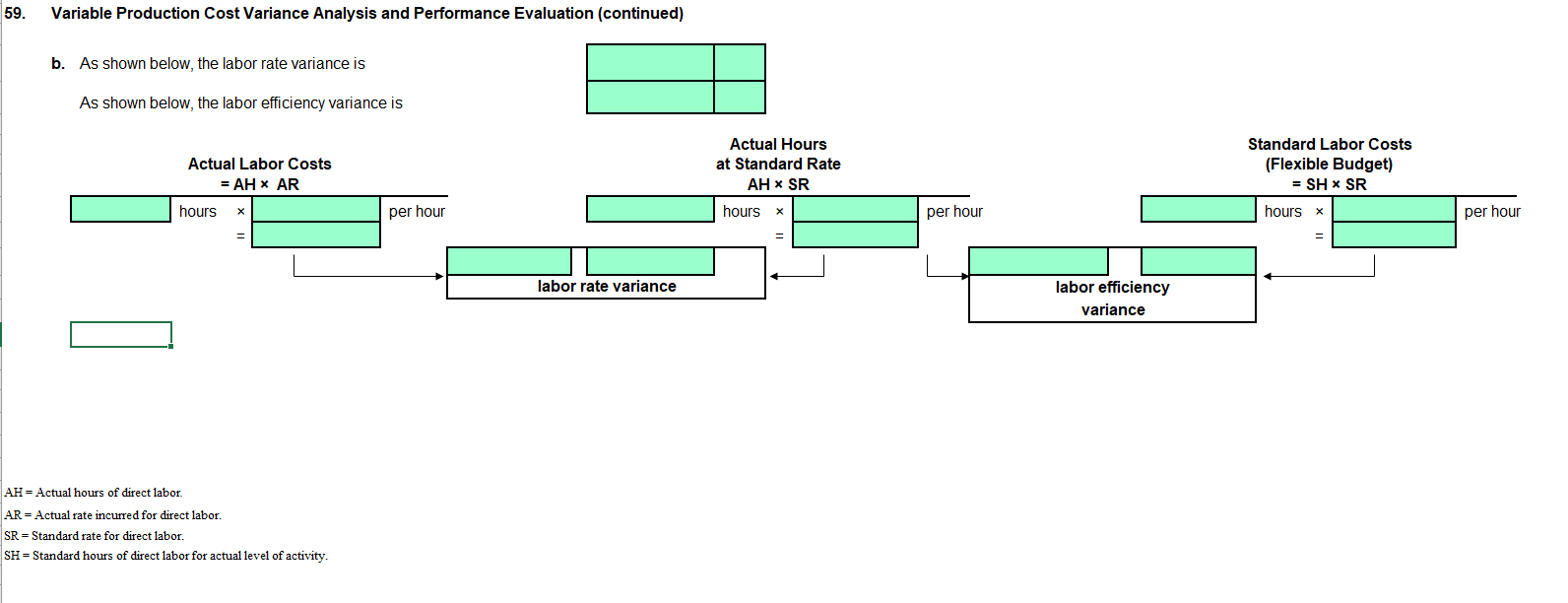

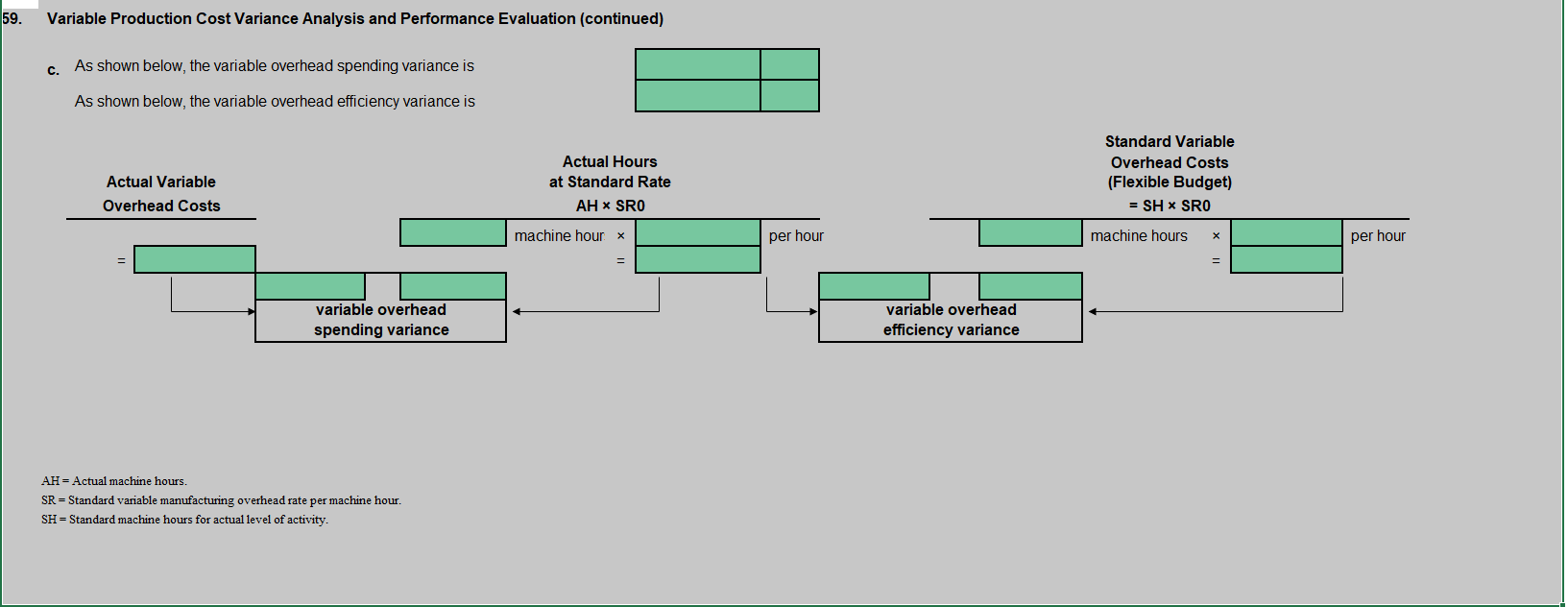

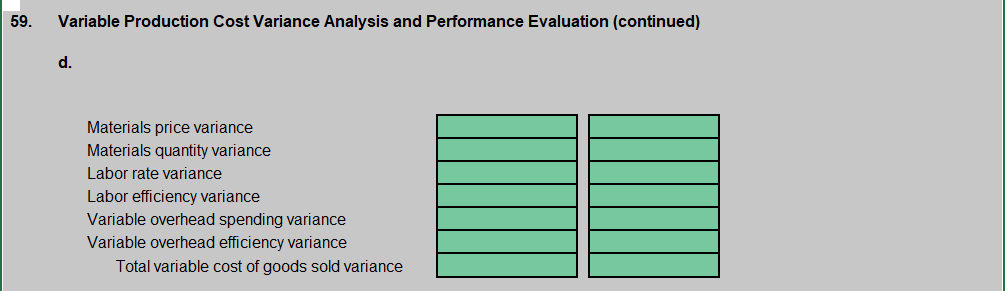

Variable Production Cost Variance Analysis and Performance Evaluation. Deerfield Plastics, Inc., produces plastic snow shovels. Variable overhead is applied to products based on machine hours. The company uses a just-in-time production system and thus has insignificant inventory levels at the end of each month. The income statement for the month of January comparing actual results with the flexible budget is shown below based on actual sales of 10,000 units: Deerfield Plastics, Inc. Income Statement {budget versus actual) Actual Budget VWariance Sales 305,000 300,000 -5,000 Favorable Variable cost of goods sold 108,700 100,000 8,700 Unfavorable Variable selling and administrative expenses 76,000 70,000 5,000 Unfavorable Contribution margin 120,300 130,000 9,700 Unfavorable Fixed cost of goods sold 53,000 55,000 -2,000 Favorable Fixed selling and administrative expenses 38,000 35,000 3,000 Unfavorable Net profit 29300 40,000 10,700 Unfavorable Deerfield Plastics, Inc_, is disappointed with the actual results and has hired you as a consultant to provide further information as to why the company has been struggling to meet budgeted net income. Your review of the previously presented budget versus actual analysis identifies variable cost of goods sold as the main culprit. The unfavorable variance for this line item is $8,700. After further research, you are able to track down the standard cost information for variable production costs: Standard Cost per Unit Standard Cost per Unit Direct materials (12 pounds per unit at $0.50 per pound) G Direct labor (0.20 hours at $15 per hour) 3 Variable overhead (0.10 machine hours at $10 per hour) 1 Standard variable production caost per unit 10 Actual production information related to variable cost of goods sold for the month of January is as follows: 10,000 units were produced and sold. 150,000 pounds of material was purchased and used at a total cost of $67,500. 1,900 direct labor hours were used during the month at a total cost of $30,400. 1,200 machine hours were used during the month. Variable overhead costs totaled $10,800. Required: a. Calculate the materials price variance and materials quantity variance using the format shown in Figure 10.2. Clearly label each variance as favorable or unfavorable. b. Calculate the labor rate variance and labor efficiency variance using the format shown in Figure 10.3. Clearly label each variance as favorable or unfavorable. c. Calculate the variable overhead spending variance and variable overhead efficiency variance using the format shown in Figure 10.4. Clearly label each variance as favorable or unfavorable. d. List each of the six variances calculated in requirements a, b, and c, and total the variances to show one net variance. Clearly label the net variance as favorable or unfavorable. Explain how this net variance relates to d. List each of the six variances calculated in requirements a, b, and c, and total the variances to show one net variance. Clearly label the net variance as favorable or unfavorable. Explain how this net variance relates to variable cost of goods sold on the income statement. e. Identify the highest favorable variance and highest unfavorable variance from the six listed in requirement d, and provide one possible cause of each variance. f. Jan Phalen, the manager at Deerfield Plastics, Inc., reviewed the company's variance analysis report for the month of January. The materials price variance of $(7,500) was the most significant favorable variance for the month, and the materials quantity variance of $15,000 was the most significant unfavorable variance. Jan would like to reward the company's purchasing agent for achieving such substantial savings by giving him a $2,000 bonus while not providing any bonus for the production manager. g. Do you agree with Jan's approach to awarding bonuses? Explain. h. What circumstances might lead to the conclusion that the purchasing agent should not receive a bonus for the month of January? '59. Variable Production Cost Variance Analysis and Performance Evaluation a. As shown below, the materials price variance is As shown below, the materials quantity variance is Actual Quantity Standard Materials Costs Actual Materials Costs at Standard Rate (Flexible Budget) =AQP x AP AQP x SP =8Q x SP0 pound x per pound pound x per pound pounds x per pound materials price variance materials quantity variance AQP = Actual quantity of materials purchased. AQY = Actual quantity of materials used in production. AP = Actual price of materials. SP = Standard price of materials 8Q = Standard quantity of materials for actual level of activity. 59. Variable Production Cost Variance Analysis and Performance Evaluation (continued) b. As shown below, the labor rate variance is As shown below, the labor efficiency variance is Actual Hours Standard Labor Costs Actual Labor Costs at Standard Rate (Flexible Budget) = AH x AR AH x SR = SH * SR hours X per hour hours X per hour hours * per hour labor rate variance labor efficiency variance AH = Actual hours of direct labor. AR = Actual rate incurred for direct labor. SR = Standard rate for direct labor. SH = Standard hours of direct labor for actual level of activity.59. Variable Production Cost Variance Analysis and Performance Evaluation (continued) c. As shown below, the variable overhead spending variance is As shown below, the variable overhead efficiency variance is Standard Variable Actual Hours Overhead Costs Actual Variable at Standard Rate (Flexible Budget) Overhead Costs AH * SRO = SH * SRO machine hour x per hour machine hours X per hour variable overhead variable overhead spending variance efficiency variance AH = Actual machine hours. SR = Standard variable manufacturing overhead rate per machine hour. SH = Standard machine hours for actual level of activity.59. Variable Production Cost Variance Analysis and Performance Evaluation (continued) d. Materials price variance Materials quantity variance Labor rate variance Labor efficiency variance Variable overhead spending variance Variable overhead efficiency variance Total variable cost of goods sold variance

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts