Question: Variance Drain Approximation Recall the formula from the Variance Drain notes (use same notation): 1 RA 5 R9 + 502. The issue raised in the

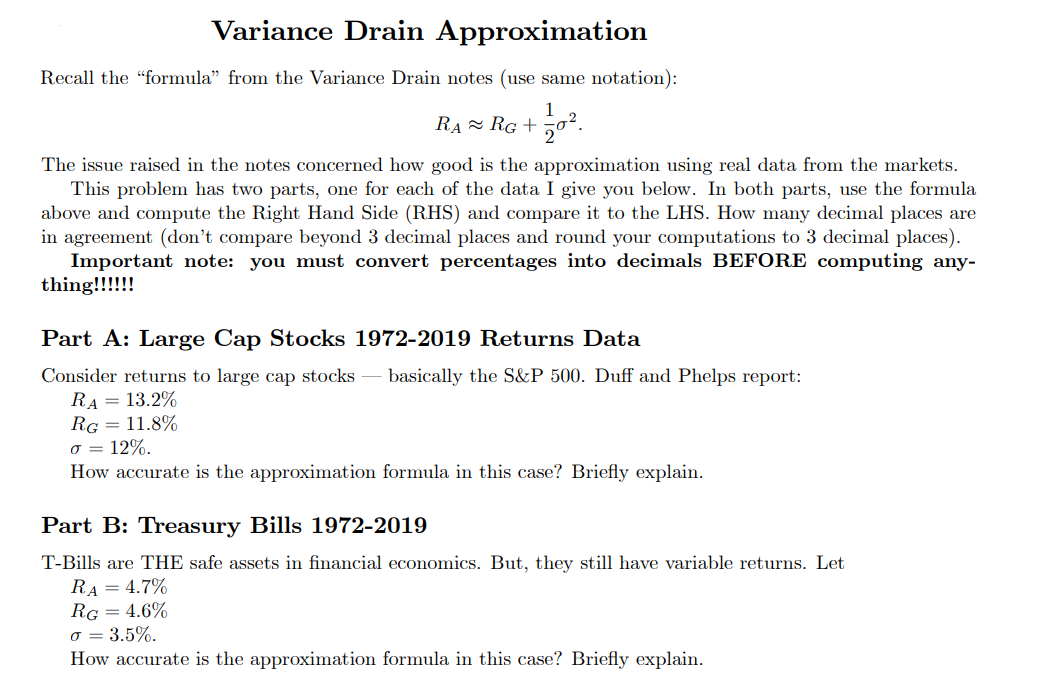

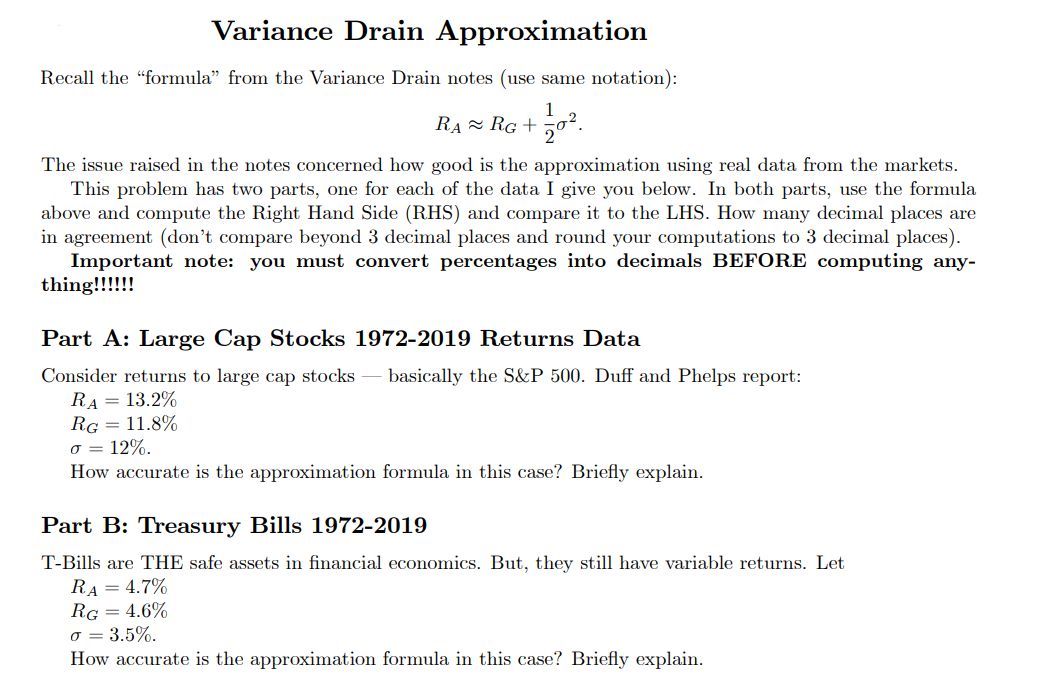

Variance Drain Approximation Recall the \"formula\" from the Variance Drain notes (use same notation): 1 RA 5 R9 + 502. The issue raised in the notes concerned how good is the approximation using real data from the markets. This problem has two parts, one for each of the data I give you below. In both parts, use the formula above and compute the Right Hand Side (RHS) and compare it to the LHS. How many decimal places are in agreement (don't compare beyond 3 decimal places and round your computations to 3 decimal places). Important note: you must convert percentages into decimals BEFORE computing any- thing!!!!!! Part A: Large Cap Stocks 1972-2019 Returns Data Consider returns to large cap stocks basically the SEEP 500. Duff and Phelps report: RA = 13.2% RG = 11.8% 0' = 12%. Ho'sr accurate is the approximation formula in this case? Briey explain. Part B: Treasury Bills 1972-2019 TBills are THE safe assets in nancial economics. But, they still have variable returns. Let R A = 4.7% RG = 4.6% 0' = 3.5%. Ho'sr accurate is the approximation formula in this case? Briey explain

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts