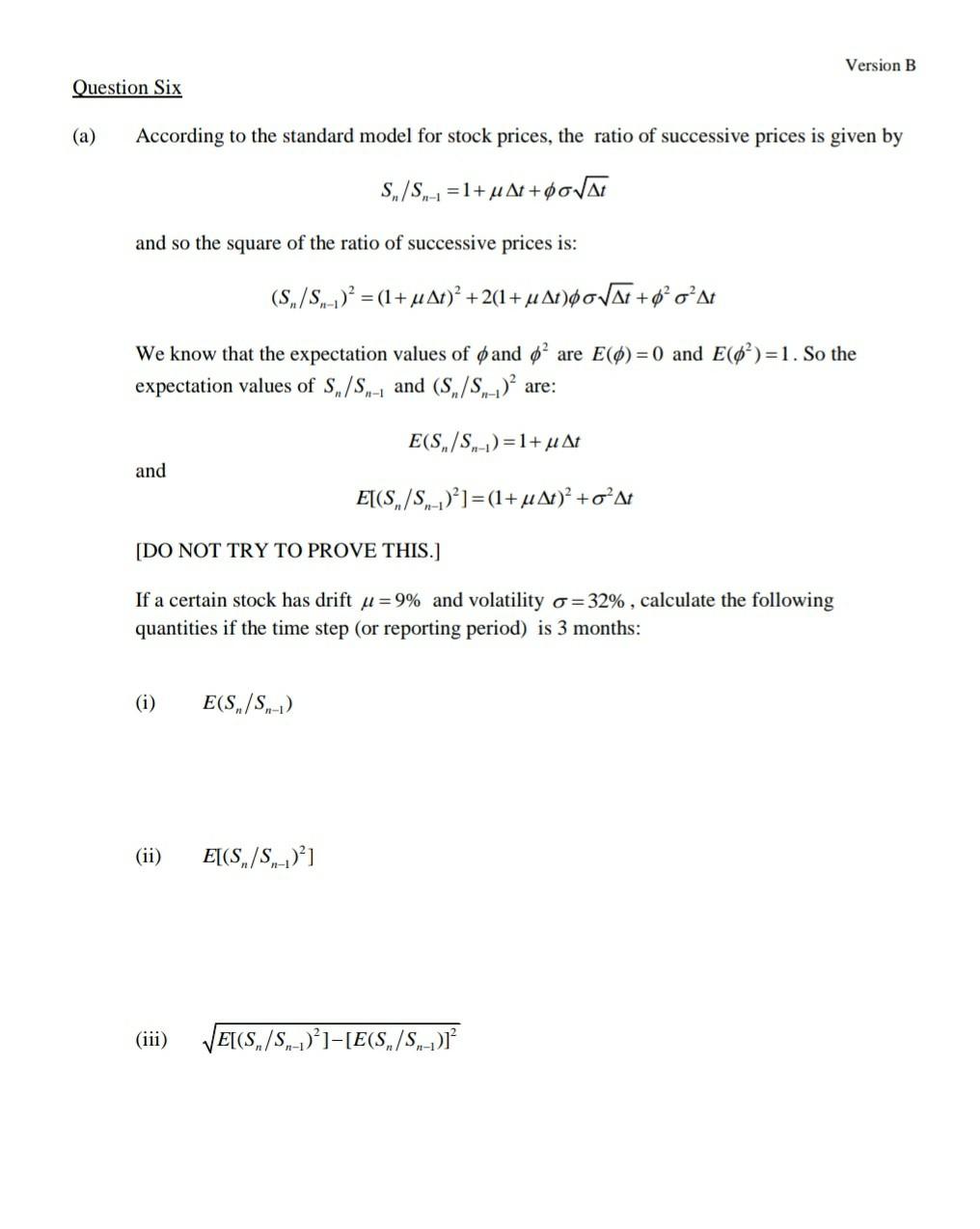

Question: Version B Question Six (a) According to the standard model for stock prices, the ratio of successive prices is given by S/S - = 1+

Version B Question Six (a) According to the standard model for stock prices, the ratio of successive prices is given by S/S - = 1+ u At+ OVA n-1 and so the square of the ratio of successive prices is: (S,/S -.)? = (1+ u At)? + 2(1+ u Atho/At + oAt = We know that the expectation values of and 6 are E(0)=0) and E(0)=1. So the expectation values of S/S.,- and (S/S) are: E(S/S)-1)=1+u At and E[(S/S -.)?] =(1+ Af)? + oAt [DO NOT TRY TO PROVE THIS.] If a certain stock has drift u = 9% and volatility o =32%, calculate the following quantities if the time step (or reporting period) is 3 months: (i) E(S/S,-) (ii) E[(S,/S,-)?1 (iii) VE[(S./S.-)1-[E(S,/S,-)1 Version B (b) a If is a random variable taken from the standard normal distribution, and n is a positive integer, the expectation value of " is given by the integral E(6") = 1 21 metro "e *1 d (i) Use the Product Rule to calculate the derivative d d el (ii) Use the result of part (i) to show that E($n+l) = nE(0-1) e/2 = 0 and lim */2 e =0 for any [Hint: You may assume that lim- positive integer k.] (iii) Use the result of part (ii) and the fact that E(6)=0) and E(0)=1 to calculate the following expectation values: E($) = E(04)= E($)= E(0)= (iv) Calculate Ecz?) if z = 320++40. Version B Question Six (a) According to the standard model for stock prices, the ratio of successive prices is given by S/S - = 1+ u At+ OVA n-1 and so the square of the ratio of successive prices is: (S,/S -.)? = (1+ u At)? + 2(1+ u Atho/At + oAt = We know that the expectation values of and 6 are E(0)=0) and E(0)=1. So the expectation values of S/S.,- and (S/S) are: E(S/S)-1)=1+u At and E[(S/S -.)?] =(1+ Af)? + oAt [DO NOT TRY TO PROVE THIS.] If a certain stock has drift u = 9% and volatility o =32%, calculate the following quantities if the time step (or reporting period) is 3 months: (i) E(S/S,-) (ii) E[(S,/S,-)?1 (iii) VE[(S./S.-)1-[E(S,/S,-)1 Version B (b) a If is a random variable taken from the standard normal distribution, and n is a positive integer, the expectation value of " is given by the integral E(6") = 1 21 metro "e *1 d (i) Use the Product Rule to calculate the derivative d d el (ii) Use the result of part (i) to show that E($n+l) = nE(0-1) e/2 = 0 and lim */2 e =0 for any [Hint: You may assume that lim- positive integer k.] (iii) Use the result of part (ii) and the fact that E(6)=0) and E(0)=1 to calculate the following expectation values: E($) = E(04)= E($)= E(0)= (iv) Calculate Ecz?) if z = 320++40

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts