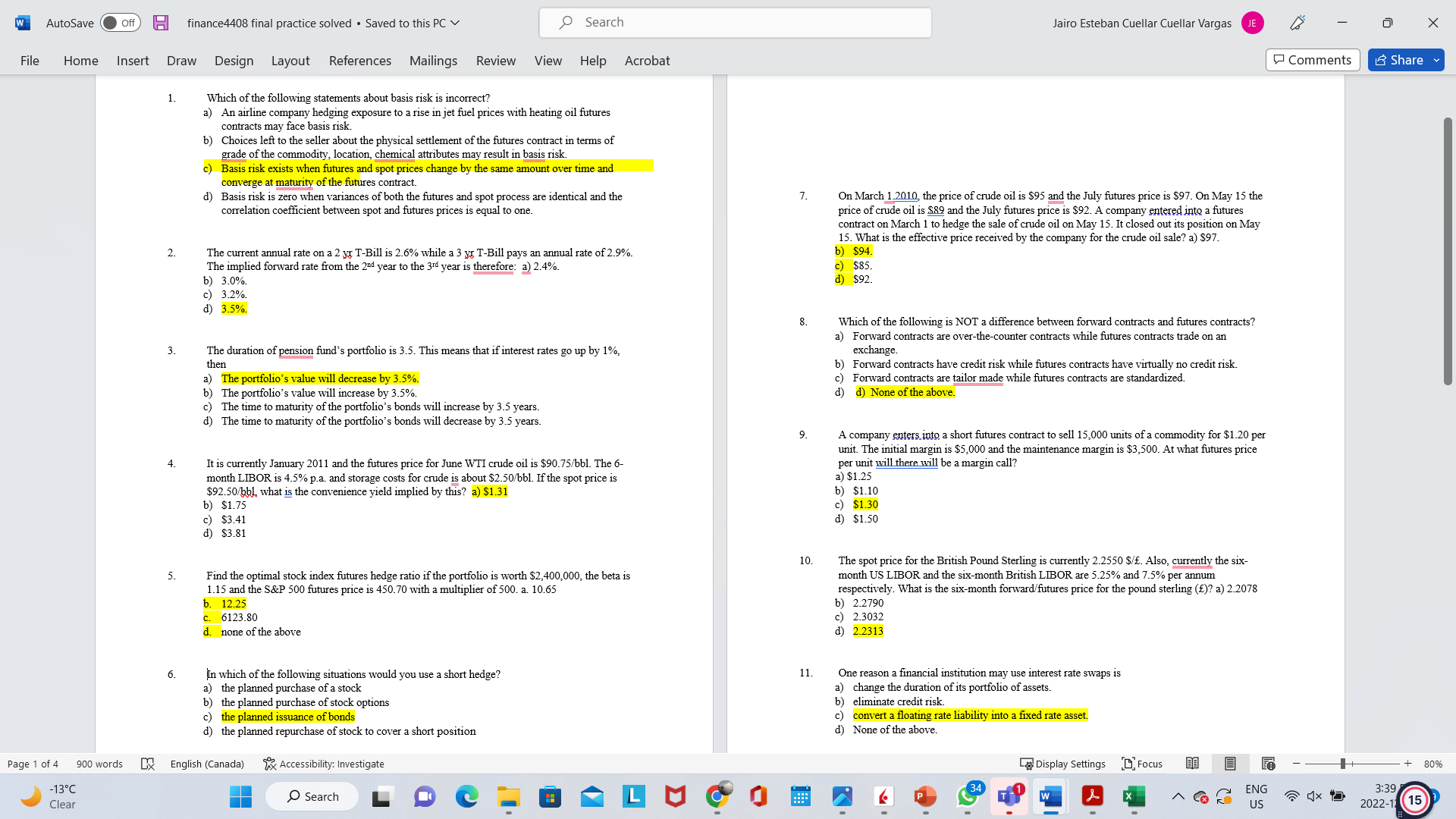

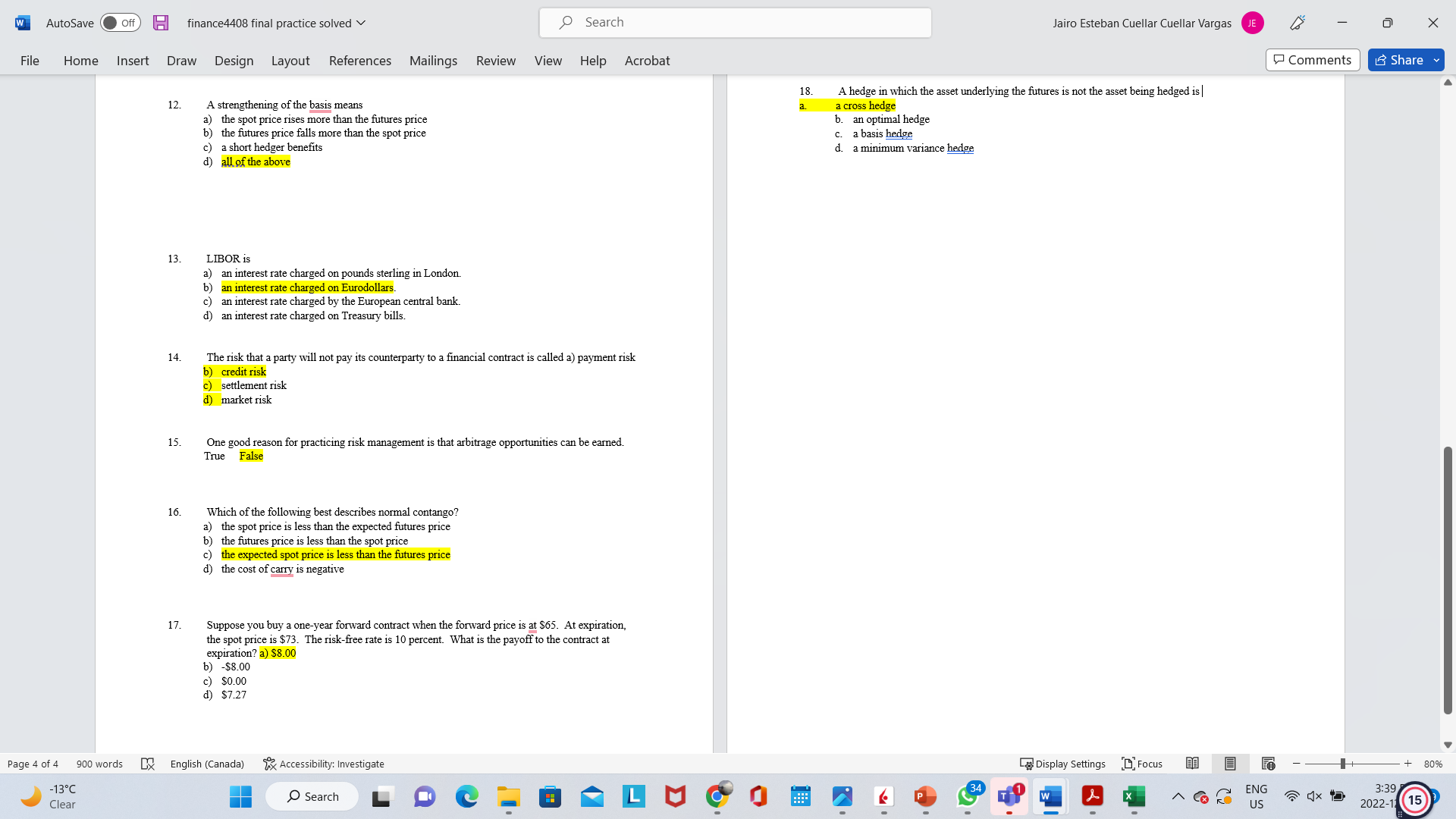

Question: W AutoSave Off finance4408 final practice solved . Saved to this PC v Search Jairo Esteban Cuellar Cuellar Vargas X File Home Insert Draw Design

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock