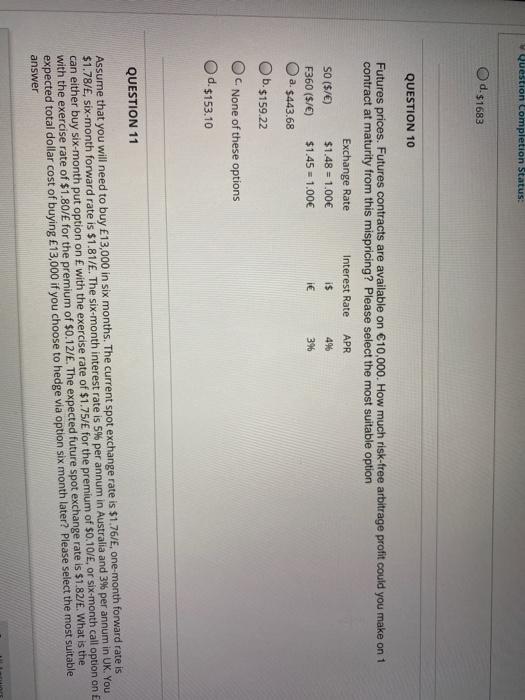

Question: w Question Completion Status: O d. 51683 QUESTION 10 Futures prices. Futures contracts are available on 10,000. How much risk-free arbitrage profit could you make

w Question Completion Status: O d. 51683 QUESTION 10 Futures prices. Futures contracts are available on 10,000. How much risk-free arbitrage profit could you make on 1 contract at maturity from this mispricing? Please select the most suitable option Exchange Rate Interest Rate APR SO ($/) $1.48 = 1.00 i$ 4% F360 ($/) $1.45 = 1.00 ie 396 a. $443.68 b. $159.22 None of these options d.$153.10 QUESTION 11 Assume that you will need to buy 13,000 in six months. The current spot exchange rate is $1.76/E, one-month forward rate is $1.78/, six-month forward rate is $1.81/. The six-month interest rate is 5% per annum in Australia and 3% per annum in UK. You can either buy six-month put option on with the exercise rate of $1.75/ for the premium of $0.10/, or six-month call option on E with the exercise rate of $1.80/ for the premium of $0.12/. The expected future spot exchange rate is $1.82/E. What is the expected total dollar cost of buying 13,000 if you choose to hedge via option six month later? Please select the most suitable

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts