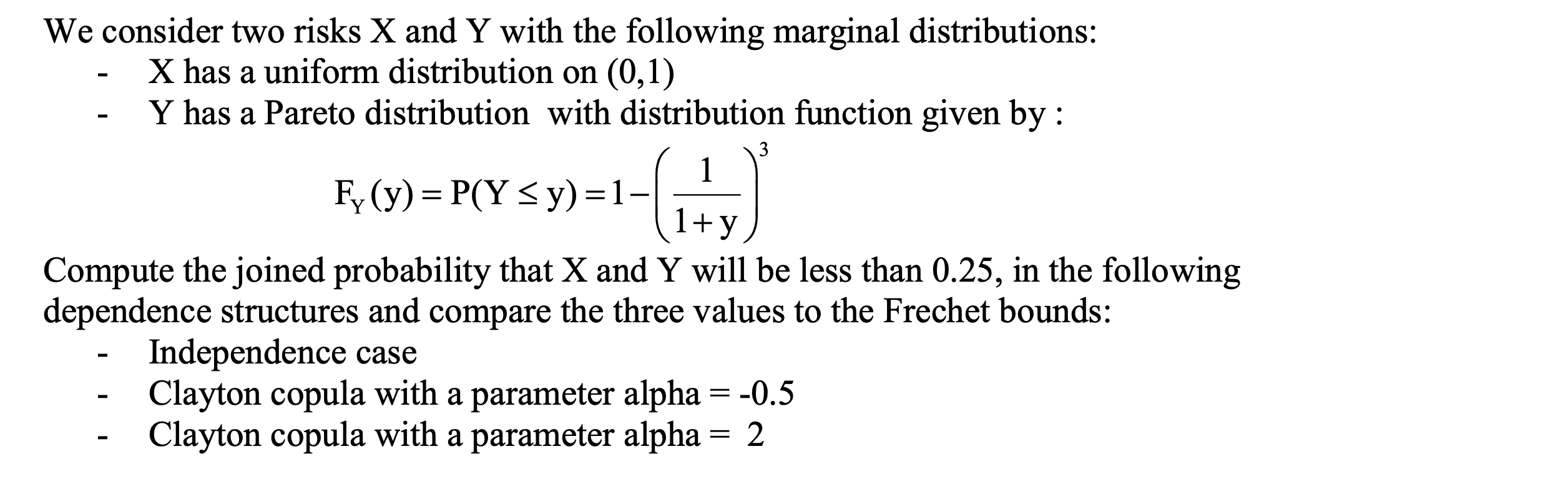

Question: We consider two risks X and Y with the following marginal distributions: - X has a uniform distribution on (0,1) - Y has a Pareto

We consider two risks X and Y with the following marginal distributions: - X has a uniform distribution on (0,1) - Y has a Pareto distribution with distribution function given by : FY(y)=P(Yy)=1(1+y1)3 Compute the joined probability that X and Y will be less than 0.25, in the following dependence structures and compare the three values to the Frechet bounds: - Independence case - Clayton copula with a parameter alpha =0.5 - Clayton copula with a parameter alpha =2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock