Question: We have solved for the minimum variance portfolio, the weights and its expected return and variance. The expected return was 25%. However, we need the

We have solved for the minimum variance portfolio, the weights and its expected return and variance. The expected return was 25%. However, we need the return to be 26. What should be the minimum variance and the weights on the three stocks using the below for data?

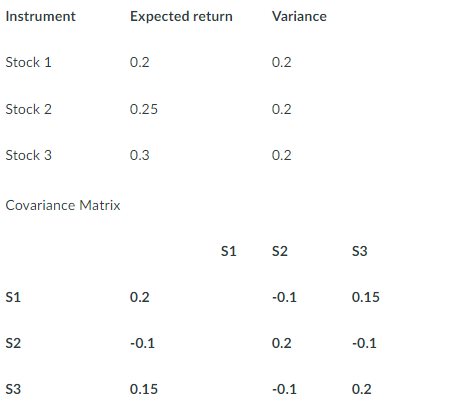

Instrument Expected return Variance Stock 1 0.2 0.2 Stock 2 0.25 0.2 Stock 3 0.3 0.2 Covariance Matrix S1 S2 53 S1 0.2 -0.1 0.15 S2 -0.1 0.2 -0.1 S3 0.15 -0.1 0.2 Instrument Expected return Variance Stock 1 0.2 0.2 Stock 2 0.25 0.2 Stock 3 0.3 0.2 Covariance Matrix S1 S2 53 S1 0.2 -0.1 0.15 S2 -0.1 0.2 -0.1 S3 0.15 -0.1 0.2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock