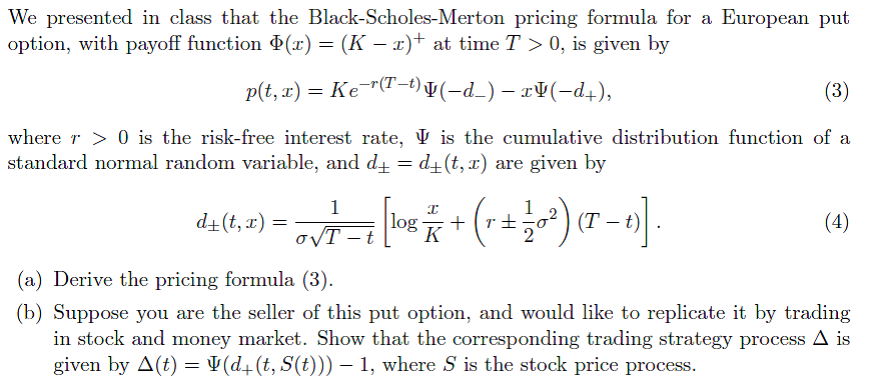

Question: We presented in class that the Black-Scholes-Merton pricing formula for a European put option, with payoff function d(x) (K-z)+ at time T > 0, is

We presented in class that the Black-Scholes-Merton pricing formula for a European put option, with payoff function d(x) (K-z)+ at time T > 0, is given by r(T-t) where r > 0 is the risk-free interest rate, is the cumulative distribution function of a standard normal random variable, and dd+(t, x) are given by a) Derive the pricing formula and would like to replicate it by trading in stock and money market. Show that the corresponding trading strategy process is uppose you are the seller of this put option, given by (t)-$(d+(t,S(t)))-1, where s is the stock price process. We presented in class that the Black-Scholes-Merton pricing formula for a European put option, with payoff function d(x) (K-z)+ at time T > 0, is given by r(T-t) where r > 0 is the risk-free interest rate, is the cumulative distribution function of a standard normal random variable, and dd+(t, x) are given by a) Derive the pricing formula and would like to replicate it by trading in stock and money market. Show that the corresponding trading strategy process is uppose you are the seller of this put option, given by (t)-$(d+(t,S(t)))-1, where s is the stock price process

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts