Question: What are the null and alternative hypothesis for both the ADF unit-root test and the KPSS unit-root test? Using your findings from both tests, what

What are the null and alternative hypothesis for both the ADF unit-root test and the KPSS unit-root test? Using your findings from both tests, what could be happening? I have attached the ADF results and KPSS results respectively.

These are all the results produced by eviews. What else is missing?

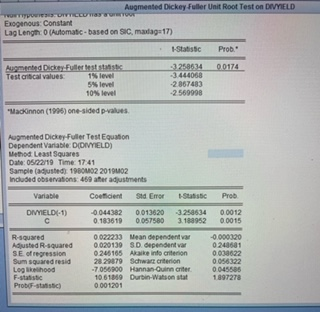

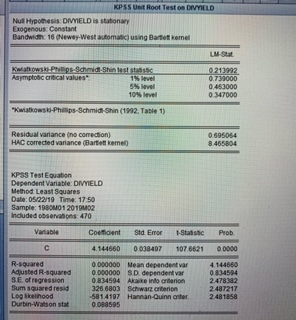

Augmented Dickey Fuller Unit Root Test on DVYIELD Exogenous: Constant Lag Length: 0 (Automatic-based on SIC, maxlag- 17) 3258534 00174 3.444068 2867483 2 569998 1% level Test criscal values 5%level 5% level 10% level Mackinnon (1996) one-sided p-values Augmented Dickey Fuller Test Equation Dependent Variable DiDNYIELD Method Least Squares Date:05/2219 Time: 1741 Sample (adjusted) 1980MM02 2019802 Included observations 469 ater adjustments Coeficient Std Emor Statstc Prob DIMYIELD-1) -0044382 0013620 3258534 00012 0.183619 0057580 3.188952 00015 R-squared Adjusted R-squared SE of regression Sum squared resid Log kkelihood F-statistic ProboF-statstic) 0 022233 0.020139 SDdependent var 0246165 Akaike info criterion 28 29879 Schwarz criterion 7.056900 Hannan-Quinn 10 61869 Durbin-Watson stat 0 001201 Mean 0.000320 0 248681 0 038622 0 056322 dependent var criter 0045585 1897278 KPSS Unit Root Test on DIVYIELD Nul Hypothesis: DMELD is stationay Exogenous: Censtant Bandwidi 16 (Neway-West automaic) using Bartet kenel LM-Stat 0213992 0.733000 Asymptobc critical values- % level 0 347000 Kwiatkowsi-Phps-Schmidi-Shin (1992, Table 1) Residual variance (no comection) HAC corrected variance (Bartet keme 0.695064 8.465804 KPSS Test Equation Dependent Variable: DIMMIELD Method Least Squares Date: 05/22/19 Time: 17 50 Sample 1980101 2019M02 Included observasons: 470 Variable Coe loent Std Emor -Statstc Peob 4.144660 0038497 107.6621 00000 R-squared 0 000000 Mean dependent var 4144660 0 834594 2478382 2487217 Adjusted R-squared0.000000 SD dependent var SE. ofregression Sum squared resid Log lkeihood Durbin-Watson staf 0834594 Akaite into crterion 326 6803 Schwarz arterion 5814197 Hannan-Quinn ater. 2481858 0.088595

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts