Question: What is the answer to line 1? Comprehensive Problem 8-85 (LO 8-1, LO 8-2, LO 8-3, LO 8-4, LO 8-5) (Static) [The following information applies

What is the answer to line 1?

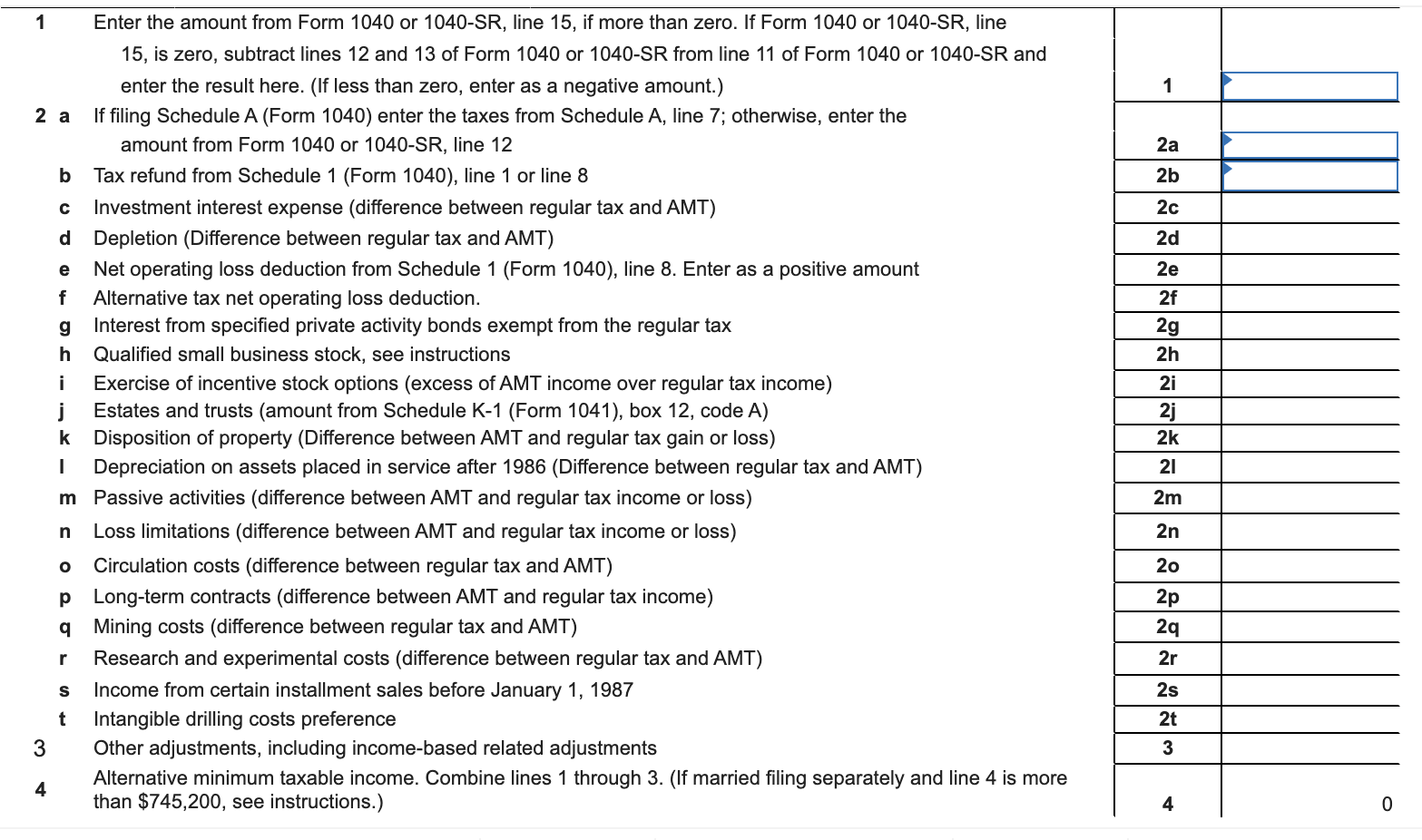

Comprehensive Problem 8-85 (LO 8-1, LO 8-2, LO 8-3, LO 8-4, LO 8-5) (Static) [The following information applies to the questions displayed below.] John and Sandy Ferguson got married eight years ago and have a seven-year-old daughter, Samantha. In 2021, John worked as a computer technician at a local university earning a salary of $152,000, and Sandy worked part time as a receptionist for a law firm earning a salary of $29,000. John also does some Web design work on the side and reported revenues of $4,000 and associated expenses of $750. The Fergusons received $800 in qualified dividends and a $200 refund of their state income taxes. The Fergusons always itemize their deductions, and their itemized deductions were well over the standard deduction amount last year. Assume the Fergusons did not receive an advance payment for the 2021 individual recovery credit because they are not eligible for the credit. Use Exhibit 8-10, Tax Rate Schedule, Dividends and Capital Gains Tax Rates, 2021 AMT exemption for reference. The Fergusons reported making the following payments during the year: - State income taxes of $4,400. Federal tax withholding of $21,000. - Alimony payments to John's former wife of $10,000 (divorced 12/31/2014). - Child support payments for John's child with his former wife of $4,100. - $12,200 of real property taxes. - Sandy was reimbursed $600 for employee business expenses she incurred. She was required to provide documentation for her expenses to her employer. - \$3,600 to Kid Care day care center for Samantha's care while John and Sandy worked. - $14,000 interest on their home mortgage ( $400,000 acquisition debt). - $3,000 interest on a $40,000 home-equity loan. They used the loan to pay for a family vacation and new car. - $15,000 cash charitable contributions to qualified charities. - Donation of used furniture to Goodwill. The furniture had a fair market value of $400 and cost $2,000. 1 Enter the amount from Form 1040 or 1040SR, line 15 , if more than zero. If Form 1040 or 1040SR, line 15 , is zero, subtract lines 12 and 13 of Form 1040 or 1040-SR from line 11 of Form 1040 or 1040SR and enter the result here. (If less than zero, enter as a negative amount.) 2 a If filing Schedule A (Form 1040) enter the taxes from Schedule A, line 7; otherwise, enter the amount from Form 1040 or 1040SR, line 12 b Tax refund from Schedule 1 (Form 1040), line 1 or line 8 c Investment interest expense (difference between regular tax and AMT) d Depletion (Difference between regular tax and AMT) e Net operating loss deduction from Schedule 1 (Form 1040), line 8. Enter as a positive amount f Alternative tax net operating loss deduction. g Interest from specified private activity bonds exempt from the regular tax h Qualified small business stock, see instructions i Exercise of incentive stock options (excess of AMT income over regular tax income) j Estates and trusts (amount from Schedule K-1 (Form 1041), box 12, code A) k Disposition of property (Difference between AMT and regular tax gain or loss) I Depreciation on assets placed in service after 1986 (Difference between regular tax and AMT) m Passive activities (difference between AMT and regular tax income or loss) n Loss limitations (difference between AMT and regular tax income or loss) - Circulation costs (difference between regular tax and AMT) p Long-term contracts (difference between AMT and regular tax income) q Mining costs (difference between regular tax and AMT) r Research and experimental costs (difference between regular tax and AMT) s Income from certain installment sales before January 1, 1987 t Intangible drilling costs preference 3 Other adjustments, including income-based related adjustments Alternative minimum taxable income. Combine lines 1 through 3. (If married filing separately and line 4 is more than $745,200, see instructions.) Comprehensive Problem 8-85 (LO 8-1, LO 8-2, LO 8-3, LO 8-4, LO 8-5) (Static) [The following information applies to the questions displayed below.] John and Sandy Ferguson got married eight years ago and have a seven-year-old daughter, Samantha. In 2021, John worked as a computer technician at a local university earning a salary of $152,000, and Sandy worked part time as a receptionist for a law firm earning a salary of $29,000. John also does some Web design work on the side and reported revenues of $4,000 and associated expenses of $750. The Fergusons received $800 in qualified dividends and a $200 refund of their state income taxes. The Fergusons always itemize their deductions, and their itemized deductions were well over the standard deduction amount last year. Assume the Fergusons did not receive an advance payment for the 2021 individual recovery credit because they are not eligible for the credit. Use Exhibit 8-10, Tax Rate Schedule, Dividends and Capital Gains Tax Rates, 2021 AMT exemption for reference. The Fergusons reported making the following payments during the year: - State income taxes of $4,400. Federal tax withholding of $21,000. - Alimony payments to John's former wife of $10,000 (divorced 12/31/2014). - Child support payments for John's child with his former wife of $4,100. - $12,200 of real property taxes. - Sandy was reimbursed $600 for employee business expenses she incurred. She was required to provide documentation for her expenses to her employer. - \$3,600 to Kid Care day care center for Samantha's care while John and Sandy worked. - $14,000 interest on their home mortgage ( $400,000 acquisition debt). - $3,000 interest on a $40,000 home-equity loan. They used the loan to pay for a family vacation and new car. - $15,000 cash charitable contributions to qualified charities. - Donation of used furniture to Goodwill. The furniture had a fair market value of $400 and cost $2,000. 1 Enter the amount from Form 1040 or 1040SR, line 15 , if more than zero. If Form 1040 or 1040SR, line 15 , is zero, subtract lines 12 and 13 of Form 1040 or 1040-SR from line 11 of Form 1040 or 1040SR and enter the result here. (If less than zero, enter as a negative amount.) 2 a If filing Schedule A (Form 1040) enter the taxes from Schedule A, line 7; otherwise, enter the amount from Form 1040 or 1040SR, line 12 b Tax refund from Schedule 1 (Form 1040), line 1 or line 8 c Investment interest expense (difference between regular tax and AMT) d Depletion (Difference between regular tax and AMT) e Net operating loss deduction from Schedule 1 (Form 1040), line 8. Enter as a positive amount f Alternative tax net operating loss deduction. g Interest from specified private activity bonds exempt from the regular tax h Qualified small business stock, see instructions i Exercise of incentive stock options (excess of AMT income over regular tax income) j Estates and trusts (amount from Schedule K-1 (Form 1041), box 12, code A) k Disposition of property (Difference between AMT and regular tax gain or loss) I Depreciation on assets placed in service after 1986 (Difference between regular tax and AMT) m Passive activities (difference between AMT and regular tax income or loss) n Loss limitations (difference between AMT and regular tax income or loss) - Circulation costs (difference between regular tax and AMT) p Long-term contracts (difference between AMT and regular tax income) q Mining costs (difference between regular tax and AMT) r Research and experimental costs (difference between regular tax and AMT) s Income from certain installment sales before January 1, 1987 t Intangible drilling costs preference 3 Other adjustments, including income-based related adjustments Alternative minimum taxable income. Combine lines 1 through 3. (If married filing separately and line 4 is more than $745,200, see instructions.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts