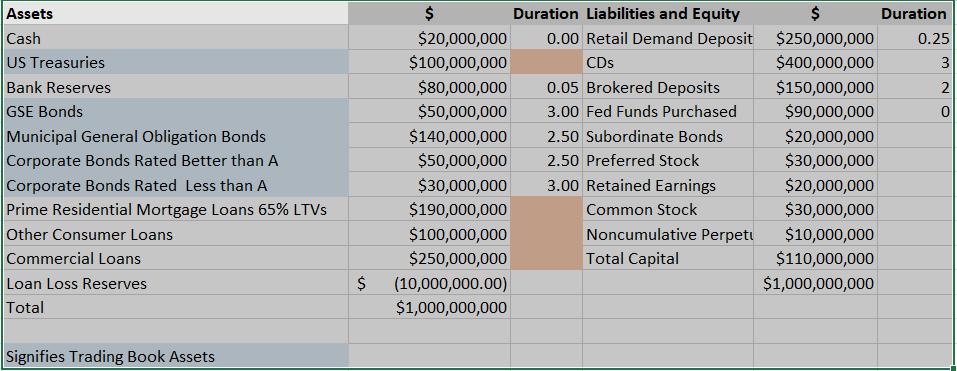

What is the bank's expected default frequency on its portfolio before any new product is added? What

Fantastic news! We've Found the answer you've been seeking!

Question:

What is the bank's loss given default (loss severity) before any new product is added?

What is the bank's expected and unexpected loss and economic capital before any new product is added?

What are the ROA, ROE and RaRoC for each new product before hedging?

What is the bank's expected default frequency for each new product?

What is the bank's loss given default (loss severity) for each new product?

What is the bank's expected and unexpected loss and economic capital for each new product?

Applying the Moody's Analytics approach, what is the portfolio's volatility prior to adding new products?

Using the Moody's Analytics approach what is the bank portfolio's volatility after adding each new product (you answer should produce 4 portfolio volatilities, each associated with a new product)

Expert Answer:

Bank Portfolio Analysis Before Adding New Products Expected Default Frequency EDF Calculate the weighted average EDF for each asset class based on its ... View the full answer

Related Book For

Complete Business Statistics

ISBN: 9780077239695

7th Edition

Authors: Amir Aczel, Jayavel Sounderpandian

Posted Date: