Question: what is the probability that a C-rated bond will have defaulted in two years? What is the probability that a B-rated bond defaults in the

what is the probability that a C-rated bond will have defaulted in two years? What is the probability that a B-rated bond defaults in the second year (but survives the first year)? If an investor has a portfolio of 1076 A-rated bonds and 50 C-rated bonds how many non-defaulted bonds would you expect to be in the portfolio after 2 years?

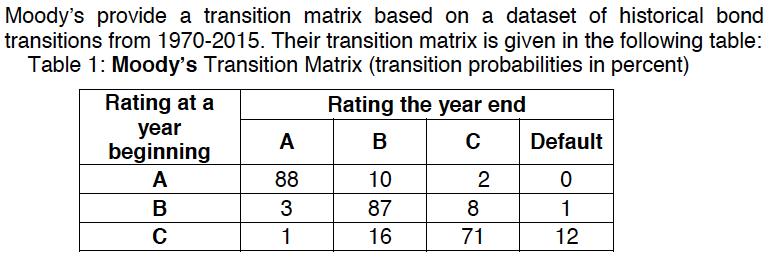

Moody's provide a transition matrix based on a dataset of historical bond transitions from 1970-2015. Their transition matrix is given in the following table Table 1: Moody's Transition Matrix (transition probabilities in percent) Rating the year end Rating at a year C Default beginning 0 2 10 87 43 12 71 16 Moody's provide a transition matrix based on a dataset of historical bond transitions from 1970-2015. Their transition matrix is given in the following table Table 1: Moody's Transition Matrix (transition probabilities in percent) Rating the year end Rating at a year C Default beginning 0 2 10 87 43 12 71 16

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts