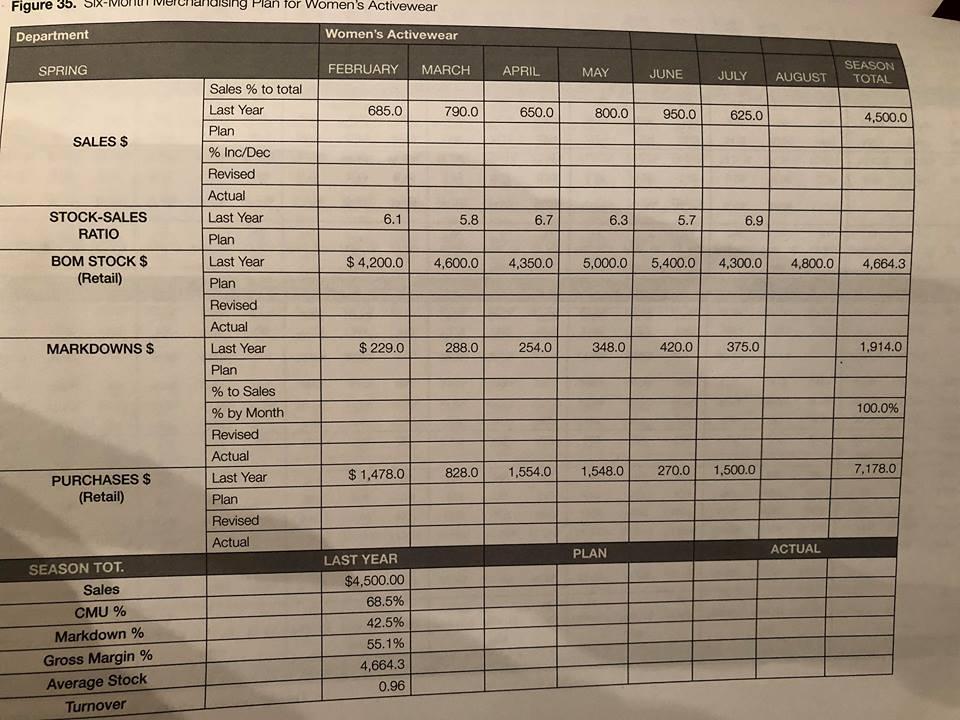

Question: When the buyer for the activewear department started to develop the merchandise plan for the spring season, she reviewed the six-month plan in Figure 35.

When the buyer for the activewear department started to develop the merchandise plan for the spring season, she reviewed the six-month plan in Figure 35. The numbers that were achieved represent the department’s performance last year for a fast- selling and up-trending department. The buyer was given the following information to plan the upcoming spring season:

Planned sales + 4.0%

Planned markdown % 45.1%

Planned turnover 0.98

Cumulative markup % 68.7%

For next spring, the buyer has to take into account a shift in Easter selling. Last year,

Easter occurred on the first Sunday in April; therefore, pre-Easter sales happened the

last two weeks in March. This year, Easter falls in the third week of April.

Based on the sales success this department has experienced over the last two years,

the buyer is concerned about keeping that trend going.

Acting as the buyer for the activewear department, formulate the six-month plan:

1. Calculate each monthâs percentage of sales for last year.

2. Calculate the total season sales planned. What will the planned sales be by

month taking into account the Easter shift?

3. Calculate the planned markdown dollars and percentage by month.

4. Calculate the BOM stock needed by month.

5. Calculate the receipt dollars needed to achieve the BOM stock.

6. Does this plan achieve the desired turnover necessary?

7. How will a buyer achieve the increased cumulative markup percentage?

What is the potential effect on gross margin given the higher markdown

percentage?

8.How should the buyer address her concern regarding sales potentially slowing down?

Figure 35. Department SPRING SALES $ STOCK-SALES RATIO BOM STOCK $ (Retail) MARKDOWNS $ PURCHASES $ (Retail) SEASON TOT. Sales CMU % Markdown % Gross Margin % Average Stock Turnover sing Plan for Women's Activewear Sales % to total Last Year Plan % Inc/Dec Revised Actual Last Year Plan Last Year Plan Revised Actual Last Year Plan % to Sales % by Month Revised Actual Last Year Plan Revised Actual Women's Activewear FEBRUARY 685.0 6.1 $ 229.0 $1,478.0 MARCH $4,200.0 4,600.0 LAST YEAR $4,500.00 68.5% 42.5% 55.1% 4,664.3 0.96 790.0 5.8 288.0 828.0 APRIL 650.0 6.7 MAY 254.0 800.0 6.3 348.0 1,554.0 1,548.0 PLAN JUNE 950.0 5.7 4,350.0 5,000.0 5,400.0 4,300.0 JULY AUGUST 420.0 625.0 6.9 375.0 270.0 1,500.0 4,800.0 ACTUAL SEASON TOTAL 4,500.0 4,664.3 1,914.0 100.0% 7,178.0

Step by Step Solution

3.51 Rating (154 Votes )

There are 3 Steps involved in it

1 To calculate each months percentage of sales for last year divide each months sales by the total season sales February 6850 45000 152 March 7900 45000 176 April 6500 45000 144 May 8000 45000 178 Jun... View full answer

Get step-by-step solutions from verified subject matter experts