Question: When the restriction that the underlying does not pay income is removed, the modified Black- Scholes model is often referred to as the Garman-Kolhagen pricing

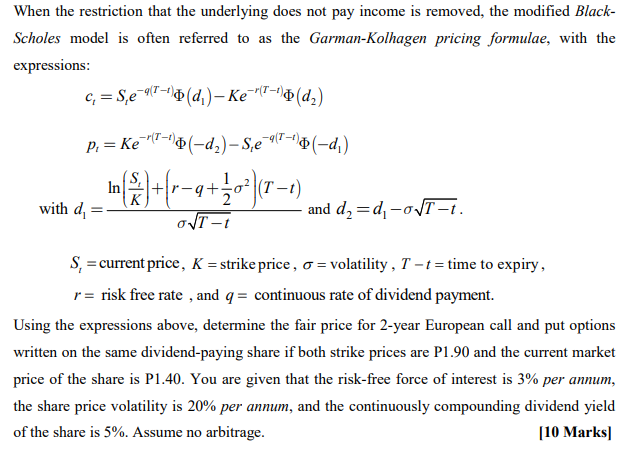

When the restriction that the underlying does not pay income is removed, the modified Black- Scholes model is often referred to as the Garman-Kolhagen pricing formulae, with the expressions: c, = Se=1/2=6* (d) - Ke="t=\(dz) P. = Ke "-"(-d2)-Se-917-1) (-d) In *)+(2-4+203)(1-1) with d and dy=d, -o/T-t. OVT-t S, = current price, K = strike price, o = volatility , T - t = time to expiry, r= risk free rate , and q = continuous rate of dividend payment. Using the expressions above, determine the fair price for 2-year European call and put options written on the same dividend-paying share if both strike prices are P1.90 and the current market price of the share is P1.40. You are given that the risk-free force of interest is 3% per annum, the share price volatility is 20% per annum, and the continuously compounding dividend yield of the share is 5%. Assume no arbitrage. [10 Marks When the restriction that the underlying does not pay income is removed, the modified Black- Scholes model is often referred to as the Garman-Kolhagen pricing formulae, with the expressions: c, = Se=1/2=6* (d) - Ke="t=\(dz) P. = Ke "-"(-d2)-Se-917-1) (-d) In *)+(2-4+203)(1-1) with d and dy=d, -o/T-t. OVT-t S, = current price, K = strike price, o = volatility , T - t = time to expiry, r= risk free rate , and q = continuous rate of dividend payment. Using the expressions above, determine the fair price for 2-year European call and put options written on the same dividend-paying share if both strike prices are P1.90 and the current market price of the share is P1.40. You are given that the risk-free force of interest is 3% per annum, the share price volatility is 20% per annum, and the continuously compounding dividend yield of the share is 5%. Assume no arbitrage. [10 Marks

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts