Question: With reference to professional ethics, discuss the following: a) Two obligations imposed on employed professionals with regard to the principle of confidentiality. b) Five

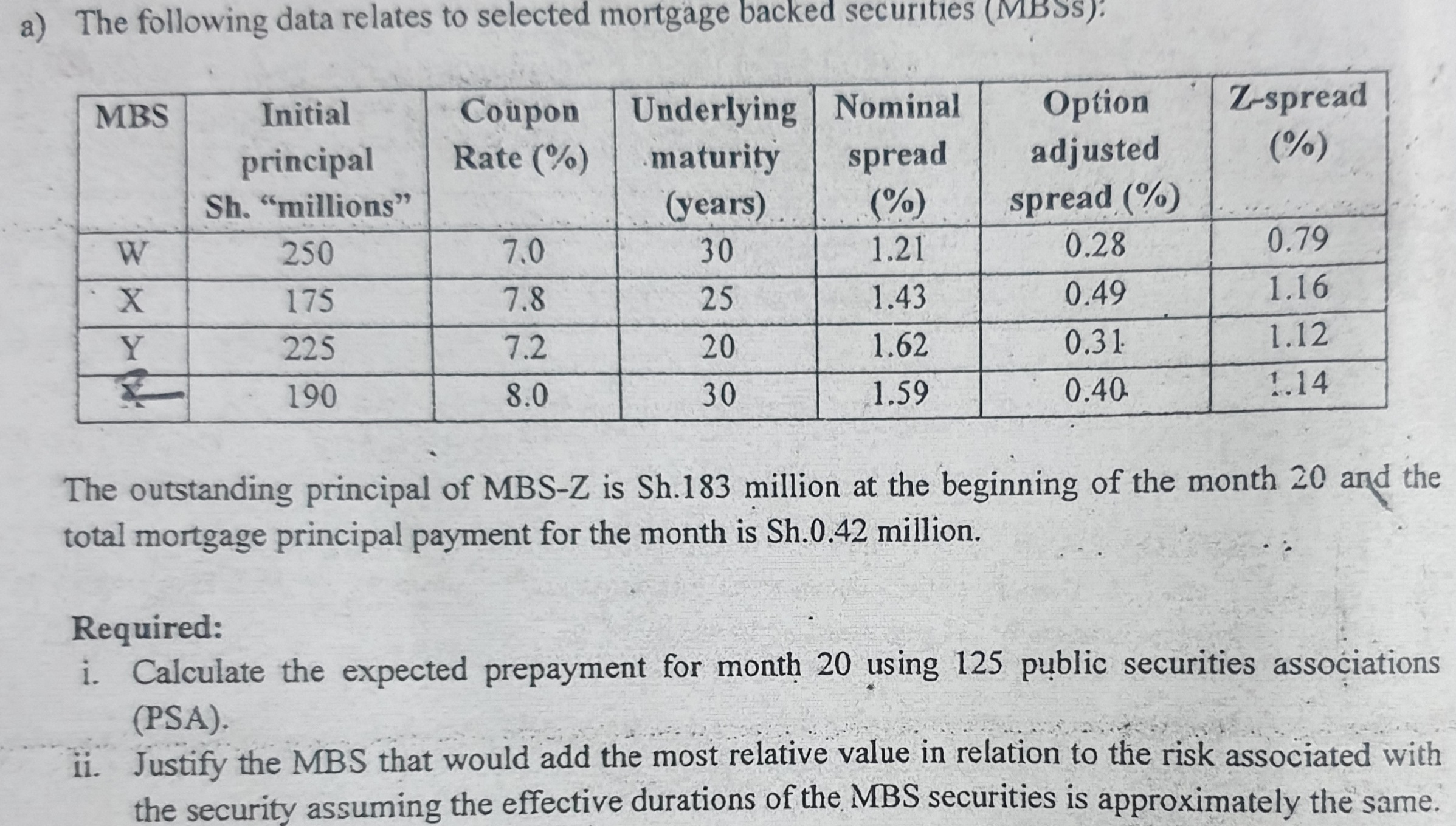

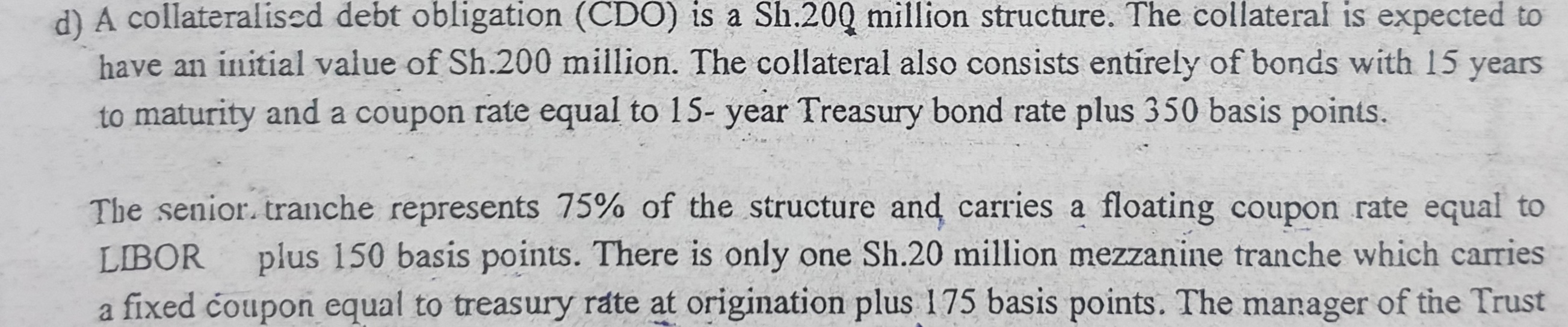

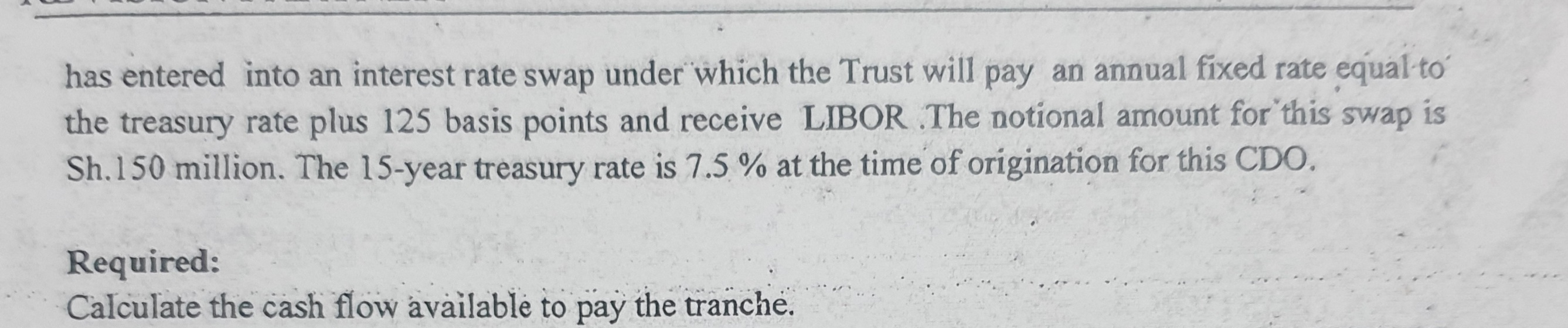

With reference to professional ethics, discuss the following: a) Two obligations imposed on employed professionals with regard to the principle of confidentiality. b) Five threats which might hinder compliance with fundamental principles prescribed by professional bodies. c) The meaning of "professional judgment" a) The following data relates to selected mortgage backed securities (MBSS)! MBS Initial principal Coupon Rate (%) Underlying Nominal Option Z-spread maturity spread adjusted (%) Sh. "millions" (years) (%) spread (%) W 250 7.0 30 1.21 0.28 0.79 X 175 7.8 25 1.43 0.49 1.16 Y 225 7.2 20 1.62 0.31 1.12 190 8.0 30 1.59 0.40 1.14 The outstanding principal of MBS-Z is Sh.183 million at the beginning of the month 20 and the total mortgage principal payment for the month is Sh.0.42 million. Required: i. Calculate the expected prepayment for month 20 using 125 public securities associations (PSA). ii. Justify the MBS that would add the most relative value in relation to the risk associated with the security assuming the effective durations of the MBS securities is approximately the same. d) A collateralised debt obligation (CDO) is a Sh.200 million structure. The collateral is expected to have an initial value of Sh.200 million. The collateral also consists entirely of bonds with 15 years to maturity and a coupon rate equal to 15- year Treasury bond rate plus 350 basis points. The senior. tranche represents 75% of the structure and carries a floating coupon rate equal to LIBOR plus 150 basis points. There is only one Sh.20 million mezzanine tranche which carries a fixed coupon equal to treasury rate at origination plus 175 basis points. The manager of the Trust has entered into an interest rate swap under which the Trust will pay an annual fixed rate equal to the treasury rate plus 125 basis points and receive LIBOR The notional amount for this swap is Sh.150 million. The 15-year treasury rate is 7.5 % at the time of origination for this CDO. Required: Calculate the cash flow available to pay the tranche. c) An investor purchases a 30-year Sh.500, 000 level payment fully a rate of 12 %. Required: The outstanding principal at the end of three months.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts